Weekly Trend Status Update

- Marc Bentin

- May 25, 2019

- 5 min read

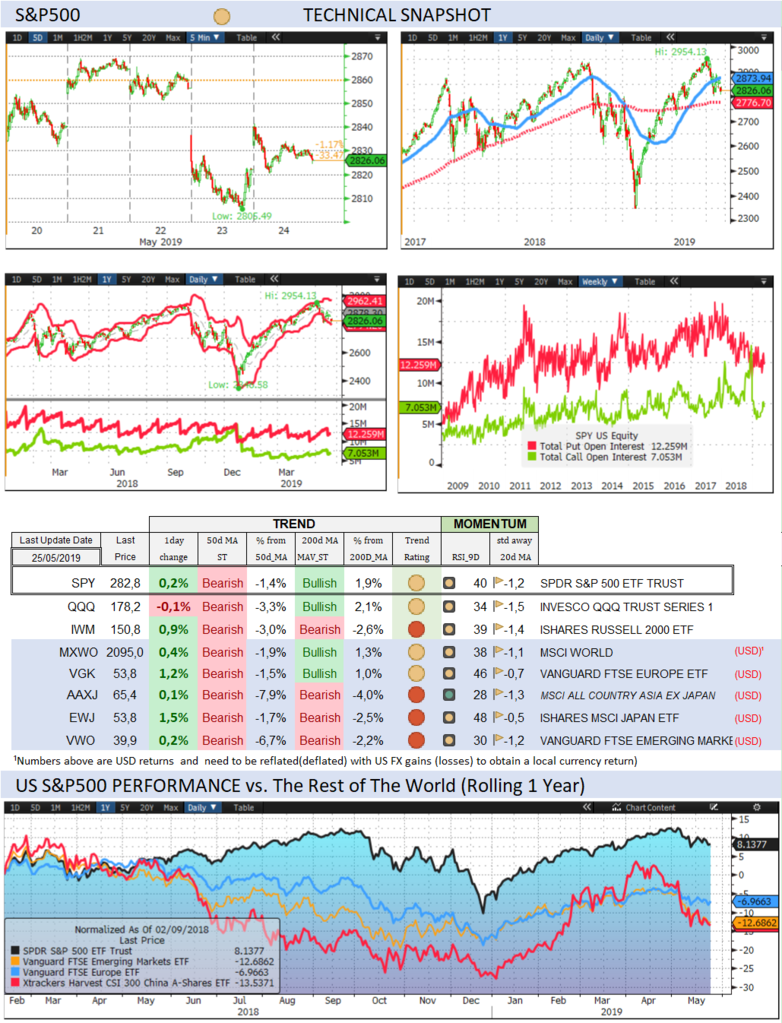

Last week was marked by a distinct “risk off tone”. The S&P500 dropped -1,1% (13,1% YTD) while the Nasdaq100 shed -2,7% (15,5% YTD). The US small cap index dropped -1,3% (12,6% YTD). Despite a whiplash on Thursday, the CBOE Volatility Index closed the week unchanged at 15,85. Popular tech names and Fangs underperformed. AAPL sold off by -5,3% (13,5%) on reduced Chinese prospects. FB dropped -2,3% (38,1%). The worst sector for the week was energy (XLE) which shed -3,3% (7,4%, Z-score -2,1). Health Care did best (XLV) gaining 1,3% (3,5%). The Eurostoxx50 was not spared, dropping -1,9% (13,1%), underperforming the S&P500 by-0,8%, dragged down by Europe’s STOXX 600 Bank index falling -3.0% and a harder 6% fall for Italian banks. Diversified EM equities (VWO) proved resilient last week despite a bout of risk aversion, only dropping by -0,5% (4,6%), supported by fresh traction from Indian shares (EPI) which rallied 5,6% (5,3%) in response to Modi’s reelection. CSI300 Chinese equity index (ASHR) dropped -1,1% (17,4%) whilst Russian shares (RSX) rallied 2,3% (15,3%) on continued RUB strength (USDRUB dropped -0,3% on the week (-7,0% YTD)) despite a selloff in oil prices on Thursday and Friday. The Dollar DXY Index (UUP), measuring the USD performance vs. other G7 currencies, dropped -0,4% (3,1%) after suffering a false breakout on Thursday and falling on Friday. In a mirror like fashion, EURUSD gained 0,4% on the week (-2,3%). The MSCI EM currency index (measuring the performance of EM currencies vs. the USD) held steady, even gaining a little 0,3% over the past week to return green for the year (+0,1% YTD). For the most part, the Fed asserted last week that it was not about to lower the targeted Fed funds rate with US Federal Reserve officials, according to the minutes of the central bank’s April 30-May 1 meeting, agreeing that their current patient approach to setting monetary policy could remain in place ‘for some time’. Recent weak inflation data were also viewed by many participants ‘as likely to be transitory’, while risks to financial markets and the global economy had appeared to ease. However, this judgment was rendered before the Trump administration imposed higher tariffs on Chinese goods which fuelled a tough Chinese rebuke along with the all-in assault of the Trump administration against China’s “Apple”, Huawei. Bond markets have begged to disagree, signalling that the Fed will cut and do so soon. The market probability for a rate cut by the December 11th FOMC meeting, jumped to 80% last week, up from 75% for the previous week and 59% the week before. 10Y US Treasuries rallied -7bps (-36bps) to 2,32%. 10Y Bunds dropped -1bps (-36bps) to -0,12%. 10Y Italian BTPs rallied -11bps (-19bps) to 2,55%, out-performing Bunds by -9bps. While US High Yield (HY) Average Spread over Treasuries managed to close the week unchanged (-133bps YTD) at 3,93%, US High Yield of worse quality suffered a +33bps widening on the Caa Average Spread which climbed 33bps (-216bps) to 7,73%. US Investment Grade Average OAS also climbed 5bps (-35bps) to 1,37%. Emerging market debt in local currency EMLC (VANECK VECTORS J.P. MORGAN) gained 0,9% (-0,6%). In European credit markets, EUR 5Y Senior Financial Spread climbed 6bps (-23bps) to 0,87% in response to a further decline in European bank shares. Gold added 0,6% (+0,2% YTD) while Silver outperformed with a gain of 1,1% (-6,0%). Speculative short positioning against Silver, along with fresh highs for the gold/silver ratio and a false break of the dollar last week (which closed lower amidst rising trade tensions and possible side effects for foreign appetite to refinance ever larger US deficits) could be encouraging or at least offer some relief to the bulls, if history is any guide. Major Gold Mines (GDX) dropped -0,9% on the week (-2,5% YTD). Sea shells XXXcoins continued to defy the sceptics (yours truly included), rallying +14,2% (+120,8% YTD). Major Gold Mines (GDX) dropped -0,9% (-2,5%). The commodity complex was a real victim last week with the Goldman Sachs Commodity Index selling off -3,6% (+12,2%) and the entire sector falling in bear trend, judging from the sample we follow. For the week, WTI Crude also shed -6,6% (29,1%, Z-score -2,3). Copper declined 1.7%, approaching January lows whilst some stabilisation was seen in agricultural commodities with DBA recouping 2,2% (-4,0% YTD). Although fairly minor (for developed markets) so far, last week’s selloff pointed to rising risks that now include collapsed trade talks, rising US/China tensions, more signs that global growth is waning (the Markit indices in Europe and the US last week were a real negative surprise), rapidly deteriorating geopolitical concerns and finally, a breakdown in talks between the D. Trump and the US Congress on the idea of a bipartisan infrastructure project. The outlook seems to us sufficiently dimmed and mudded to warrant some caution. The (long Memorial) week end will bring some relief while the results of European elections tomorrow likely hold the key to the euro (with new lows or bottoming out both in sight) over the near term.

Important Disclaimer © Copyright by BentinPartner llc. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation or particular needs of any person who receives this report. Accordingly, the opinions discussed in this Report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner llc, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner llc. The content and views expressed in this report represents the opinions of Marc Bentin and should not be construed as guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner llc believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets or developments referred to in the Report. #fx #forex #investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants

Comments