DeepSeeking What is Next...

- Marc Bentin

- Feb 3, 2025

- 7 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Caught between the Chinese artificial intelligence start-up Deep Seek revelation, the Fed meeting which did not signal rate cuts and D. Trump’s tariffs salvos shot at the end of the week, stocks had a volatile week, closing only with mild losses.

The DeepSeek app drew both awe and consternation as an ultra-competitive AI bot functioning at a fraction of the cost of its US competitors. The sudden interest in DeepSeek sent shivers down the spine of investors in preferred AI plays, including Nvidia or Broadcom (which both dropped 17% on Monday) but also the entire chip and energy sector as it dawned on investors that perhaps, China’s Deep Seek holds the potential to be a major disruptor in the AI space, requiring much less powerful chips and therefore much less energy. As a result, DeepSeek’s AI assistant rose to the No. 1 spot on Apple App Store on Jan. 26, holding this position globally since then, according to Appfigures data that exclude downloads from China.

Could this herald the beginning of a new era, or more prosaically the beginning of the end of the AI mania? I am not sufficiently expert in the field to express an affirmative opinion but others who are …did and the price action was ominous enough for everyone to notice, especially starting from an already faded momentum for most AI plays (besides energy which was caught completely flat footed).

Whether Deepseek meant a Sputnik moment or not, the rest of the week did not deliver much in terms of “positive” news susceptible to erase the “back eye” from Monday and the technical wound was deep enough for our trend and momentum model to reduce significantly its exposure to both, IT, utilities and energy, in favor of more defensive sectors such as health care, industrials or consumer discretionary. At the moment, we are also “fundamentally” more comfortable holding US sectors in “anything but” the underperforming sectors from last week which remain priced to (near) perfection. Human bias enabled the rebound…

Of course, the response to DeepSeek will be, at least initially, to downplay the risk, then even possibly to discard and litigate it, given that the innovation came from China.

In any case, if only half of Chinese AI achievements are genuine, legitimate and lasting, this will signal that the US AI spending binge will likely face a hangover and that sanctions against China to deprive the country from high end chips only forced it to be more creative and at an advantage to unleash potential creative destruction.

History is replete with examples of tech innovators that lost their shine after being disrupted by competitors delivering and outpacing the initial innovator at a fraction of the cost. History is also replete of bubbles of all sorts that were pricked by a seminal event that was initially ignored. And if sentiment is any guide, investors’ confidence is probably still too high and possibly in denial of the risk of a deeper correction.

While earnings results were generally favorable last week, with some exceptions, macro (inflation and confidence) concerns coupled to Trump’s tariffs moves were barely supportive.

US jobless claims increased slightly to 223k (from 220k), the US S&P Global composite PMI index for January came at 52.4 (from 55.4 previously) although the US Manufacturing PMI was better than expected (at 50.1 (from 49.4 last month). The University of Michigan Sentiment Survey declined to 71.1 (from 73.2 in December). The volatile durable goods orders report unexpectedly dropped by -2.2% (from -1.2% the previous month). Real estate data, however (existing and new home sales) improved last month. The Fed’s preferred inflation gauge rose 0.3% MoM, from 0.1% in December, demonstrating the lack of improvement on the inflation front.

Bonds rallied last week with 10Y yields dropping -8bps 8with similar moves in Europe), reassured that the Fed did not signal imminent rate cuts at the same time as inflation pressures remained unabated and as “risk off” sentiment prevailed for most of last week (especially on Monday). As regards Trump’s declared intention of forcing the hand of the Fed to cut rates, my intuition is that it will will materialize as it did the last time, by forcing an equity market shock that will force the Fed to go in full easing mode.

On the FX side, the dollar was broadly stronger, with the dollar index gaining 1.1%, posting its best week since November with EUR resuming its bear trend (towards parity?) as the ECB rate cutting cycle continued while the Fed remained at a standstill and following more immediate prospects of US trade tariffs. The Canadian dollar dropped sharply by -1.4% while volatility on the Mexican peso remained discouraging for the carry trade as well.

Gold (XAUUSD) further climbed last week and briefly pierced a fresh all time high, in a move that was fueled by a surge in deliveries to the US on speculation of potential tariffs. Whatever is justifying this surge (tariffs front running or genuine runaway demand), this has forced the LBMA to ask for central banks storing their gold in London to lend itself more of their gold. According to the FT, “Governor Andrew Bailey played down the significance of the increased waiting times to remove gold from its vaults. “London remains the major gold market in the world. If you are involved in that market and want to trade or use your gold, you really need to have it in London,” he said in response to questions from parliament’s Treasury Committee on Wednesday.”” I would say at this stage that “a bird in the hand is worth two in the bush”.

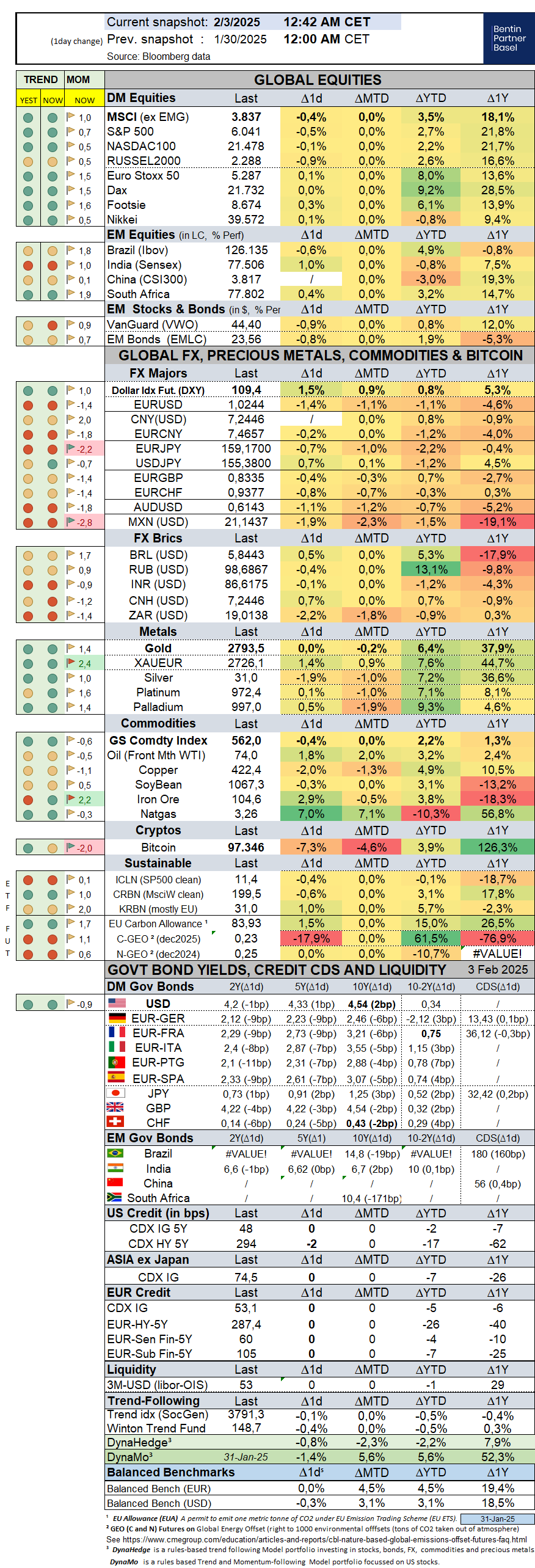

Over the past week, the S&P500 dropped -1,0% (2,7% YTD) while the Nasdaq100 dropped -1,4% (2,2% YTD). The US small cap index dropped -1,0% (2,5% YTD). AAPL rallied 5,9% (-5,8%).

The Equally Weighed SP500 dropped -0,5% (3,4% YTD), outperforming the S&P500 by 0,5%. The median SP500 YTD return closed the week at 3,0%.

Cboe Volatility Index rallied 10,6% (-5,3% YTD) to 16,43.

The Eurostoxx50 gained 1,2% (7,9%), outperforming the S&P500 by 2,2%.

Diversified EM equities (VWO) dropped -0,4% (0,8%), underperforming the S&P500 by0,6%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 1,1% (0,3%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,4% (0,8%).

10Y US Treasuries rallied -8bps (-3bps) to 4,54%. 10Y Bunds dropped -11bps (9bps) to 2,46%. 10Y Italian BTPs rallied -10bps (3bps) to 3,55%, underperforming Bunds by 1bps.

US High Yield (HY) Average Spread over Treasuries climbed 5bps (-26bps) to 2,61%. US Investment Grade Average OAS climbed 1bps (-1bps) to 0,86%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 0bps (-4bps) to 0,60%.

Gold gained 1,0% (6,6%) while Silver rallied 2,4% (8,3%). Major Gold Mines (GDX) rallied 2,7% (14,9%).

Overnight in Asia…

S&P future -97 points

On Saturday, D. Trump signed an order imposing 25% tariffs on all goods from Canada and Mexico starting on Tuesday, with the exception of Canadian energy products, which will be subject to a 10 percent duty. Both Mexico and Canada have both announced retaliatory tariffs against the US including a 25% top tariffs on $106.5bn of US goods. Trump has said that the tariffs against Mexico were due to the country's failure to stop fentanyl getting into the United States as well as what he describes as uncontrolled migration, Bloomberg reported.

On the other hand, “Why not implement tariffs as of now, or tomorrow, or Monday? Why Tuesday?” said Gabriel Casillas, chief Latin America economist at Barclays Plc. “It seems that US President Trump wants something in return before tariffs are effectively imposed.” So, expectations remain that we will see a lot of ups and down related to D. Trump’s erratic tariffs policy.

MXN is marked 2% lower (21.15) this morning and EURUSD 1 figure lower at 1.0250.

To learn more about why and how to invest in the trend-following investment factor, check our dedicated web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments