Pressure Mounts on Asian Pegs...

- Marc Bentin

- May 12, 2025

- 6 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

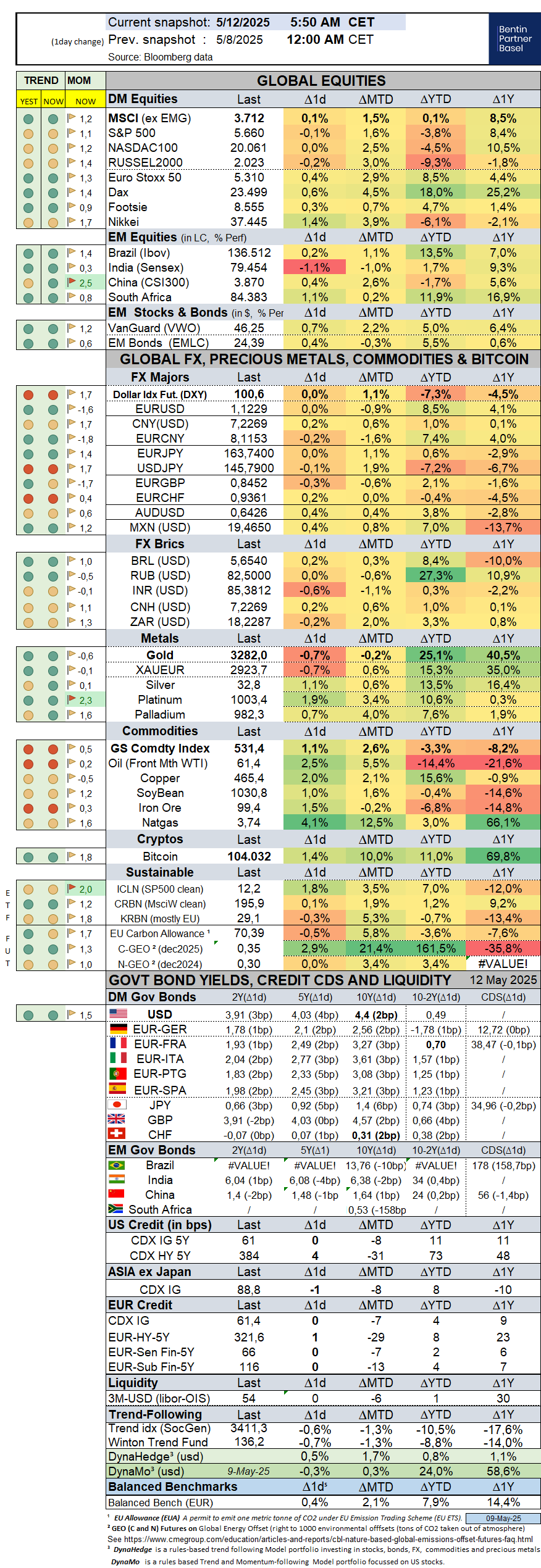

US stocks marked a pause last week, dropping slightly and underperforming international markets. The week started with President Trump making another surprise tariff announcement, this time contemplating a 100% tariff on foreign made movies and with sentiment dampened by W. Buffet announcing that he would be passing the baton of Berkshire Hathaway at the end of the year.

Some optimism returned on Tuesday after Treasury Secretary Scott Bessent said he would travel place (without Trump adviser Peter Navarro) to Switzerland for the week end in order to meet with Chinese trade officials.

Stocks remained volatile on Wednesday following the expected Federal Reserve decision to leave interest rates unchanged (in a range between 4.25% to 4.5%), but with Fed Chair Powell warning that the risks for an economic slowdown and higher prices may increase if large tariffs that were announced remain in place, essentially threatening both sides of the Federal Reserve’s dual mandate. Fed Chair Powell knocked down any notion of taking preemptive rate cut decision which gave a positive spin to the USD for the rest of the week despite endless talks of further dollar devaluation concerns (and urges for tactical FX hedges).

That said, in an emergency press briefing late Monday, Taiwan’s central bank sought to quell speculation about the currency’s surge, saying that the wild, two-day appreciation was partially attributable to market chatter and urged against irresponsible speculation… More diversification, with a keen focus on Asia remains a popular strategy with most of the European stock market outperformance so far this year sourced not from improving economic prospects but from huge concerted borrowing plans for war preparation (it was reported last week that the ECB Council was also briefed with Russia’s (bad) military intentions in Europe as a preamble to its policy discussions and decision).

The cheerleading surrounding the first major trade deal to lower tariffs between the US and the UK (which still left the UK with 10% tariffs on most of UK imports) and further talks of some big planes purchases caused an initial burst higher on Thursday before those gains were faded as D. Trump could not refrain from calling J. Powell names after the Fed Chairman did not bow under the pressure…to immediately cut interest rates.

While the dollar proved fairly resilient last week, credit spreads also continued to ease but US 10Y Treasury yields rose 7bps with jobless claims remaining resilient and inflation pressure not really abating at the same time as issuance of non-financial commercial paper swelled by $100 billion last month, above the monthly average of $27 billion seen from 2019 to 2024, according to Bloomberg.

Last week closed with a mild correction as investors awaited the outcome of US/China trade discussions. President Trump suggested an 80% tariff cut for China but did not commit to a final plan while Mag7 pressure remained after GOOG lost an antitrust trial expected to force the company to share more of its revenues. Federal Reserve Governor Michael Barr also echoed J. Powell’s message that recent tariff hikes could drive inflation and slow economic growth.

Small caps outperformed last week with credit spreads and volatility (VIX) improving further while the dollar gained slightly (despite the strong gains of some Asian currencies).

Precious metals closed slightly higher but remained under some profit taking with higher US yields, a resilient dollar, peace talks prospects and a powerful comeback of cryptos serving as catalysts. Silver which remains extremely cheap, outperformed, a trend which we expect will continue, irrespective of ups and downs of the metals complex.

“Chinese President Xi Jinping told Russia's Vladimir Putin… their two countries should be ‘friends of steel’, as they pledged to raise cooperation to a new level and ‘decisively’ counter the influence of the United States. At talks in the Kremlin, the two leaders cast themselves as defenders of a new world order no longer dominated by the U.S. In a lengthy joint statement, they said they would deepen relations in all areas, including military ties, and ‘strengthen coordination in order to decisively counter Washington's course of ‘dual containment' of Russia and China’.”, Reuters reported.

Outside of the geopolitical progress achieved over the week end, the fact that US buybacks have been running (in April) at the fastest pace in 41 years and that institutional investors remain cautiously positioned (with only private investors seemingly buying the dip) remain of good omen to start the week.

Overnight in Asia…

Over the past week, the S&P500 dropped -0,4% (-3,7% YTD) while the Nasdaq100 dropped -0,2% (-4,5% YTD). The US small cap index gained 0,2% (-9,1% YTD). AAPL sold off by -3,3% (-20,7%).

The Equally Weighed SP500 gained 0,4% (-1,5% YTD), outperforming the S&P500 by 0,8%. The median SP500 YTD return closed the week at -0,8%.

Cboe Volatility Index sold off by -3,4% (26,2% YTD) to 21,9.

The Eurostoxx50 gained 1,0% (9,9%), outperforming the S&P500 by 1,4%.

Diversified EM equities (VWO) dropped -0,4% (5,0%), matching the S&P500.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 0,5% (-6,0%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,4% (4,7%).

10Y US Treasuries underperformed with yields rising 7bps (-19bps) to 4,38%. 10Y Bunds climbed 3bps (20bps) to 2,56%. 10Y Italian BTPs dropped -3bps (9bps) to 3,61%, outperforming Bunds by -6bps.

US High Yield (HY) Average Spread over Treasuries dropped -9bps (56bps) to 3,43%. US Investment Grade Average OAS dropped -4bps (19bps) to 1,06%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps (2bp) to 0,66%.

Gold rallied 2,6% (26,7%) while Silver rallied 2,2% (13,2%). Major Gold Mines (GDX) rallied 7,0% (48,5%).

Goldman Sachs Commodity Index gained 1,7% (-1,2%). WTI Crude rallied 4,7% (-14,9%).

Overnight in Asia…

S&P future +79 points; Hong Kong +1.1%; Nikkei +0.1%; China +0.8%

US futures and Asian markets rallied strongly overnight after Treasury Secretary Scott Bessent said U.S.-China trade talks had made "substantial progress," following D. Trump’s comments that negotiations led to a "total reset" in the two sides' trade relationship, negotiated in a friendly, but constructive, manner" (with more details to follow today).

Some optimism followed news that V. Putin is set to meet V. Zelenskiy in Istanbul on May 15 for “direct negotiations”, following a weekend of intense diplomacy. “HAVE THE MEETING, NOW!!!” Trump said in a post on Truth Social. The US also announced progress in trade negotiations with China, nuclear talks with Iran, the war in Gaza and helped to ease tensions between India and Pakistan. We’ll see what comes…(outside of E. Macron’s X account). E. Macron promised more sanctions (that need to be voted at the unanimity to go through) if Russia refuses the cease fire. Cease fire is not synonymous with peace, unfortunately and preparing for war remains a key priority on the economic agenda of Europe, more than trying to fix dangerously derailing public finances.

To learn more about why and how to invest in the trend-following investment factor, check our dedicated web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments