The Daily Close

- Marc Bentin

- Jan 4, 2018

- 3 min read

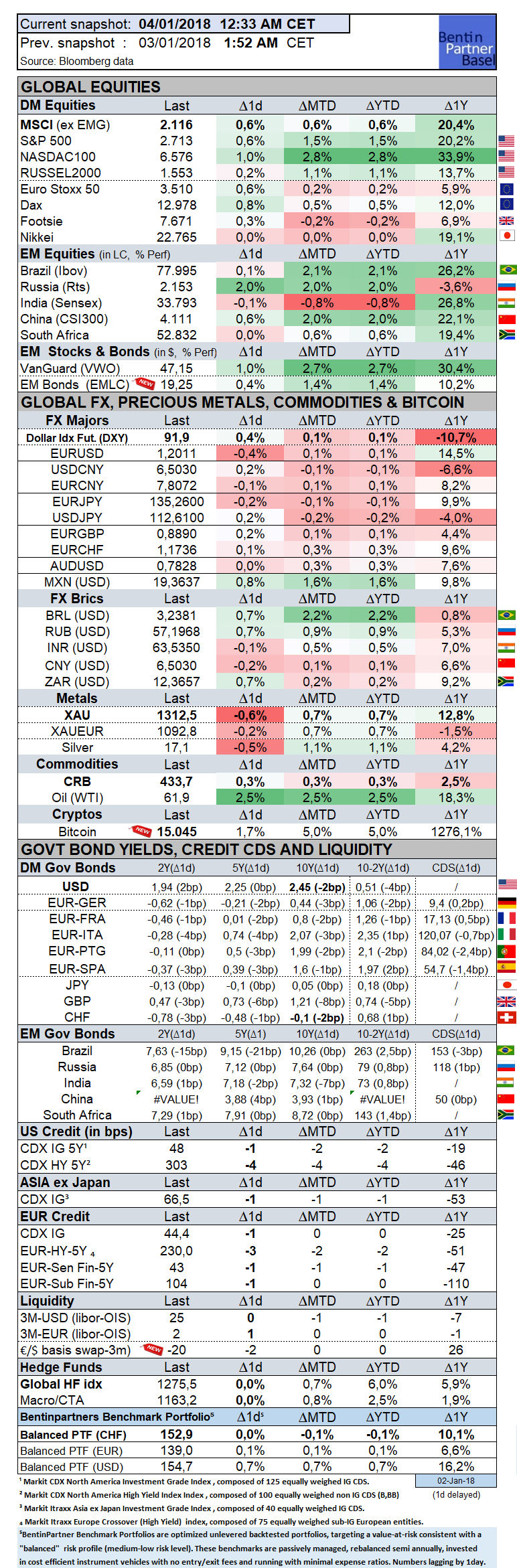

* US data were strong yesterday with December car sales pointing at more wealth effects from the run away equity markets gains. ISM Manufacturing data suggested a strengthening economic backdrop as well, likely supported by dollar weakness. December Fed minutes were a snooze. No mention was made of the crypto mania raging in December despite bitcoin gaining some 50% that month, as the Fed omitted to comment on an important element of financial (in)stability. * US stocks are losing no time this year and the S&P added +0.6%, supported by strong US data and positive momentum showing no sign of abating. Nasdaq gained +1%. While we would not necessarily fight this move (now), we are mindful that the first week of the year can be treachorous and the second equally as vicious in the other direction, at times. * European stocks recovered slightly, starting to follow up on US stock market gains, helped at the margin by Chancellor Angela Merkel saying chances of a successful conclusion to exploratory talks to build a coalition have improved. * While the dollar regained some footing against EUR (+0.4%), it weakened further against most EM with MXN adding 0.8% yesterday in line with gains of RUB, ZAR and BRL. EM stocks and bonds are leading the pack so far this year. * EUR was otherwise strong, gaining slightly vs. CHF and GBP. * Bloomberg reported that” UK PM Theresa May believes Michel Barnier is bluffing when he says there will be no special deal for financial services.” We are not so sure... GBP volatility is on the rise in this context as there is little reason to believe in a standstill for the finance industry in a post Brexit world. * Gold (and silver) dropped -0.5%, leaving XAUEUR mostly unchanged. * Oil climbed +2.5% as political tension in Iran and geopolitical unease mount (despite financial markets showing little concern, having in some ways stopped functioning as a price discovery mechanism), perhaps helped by the recent “rhethoric” of D. Trump. * The Turkish lira dropped -0.5% “after a Turkish banker was convicted of helping Iran evade U.S. financial sanctions in a verdict likely to further strain relations between Turkey and the U.S.”, Bloomberg reported. ”Foreign banks and bankers have a choice,” acting U.S. Attorney J. H. Kim in Manhattan said following the verdict. “You can choose wilfully to help Iran and other sanctioned nations evade U.S. law, or you can choose to be part of the international banking community transacting in U.S. dollars. But you can’t do both.” We may agree or disagree. But at least the message is clear... BentinPartner Advisers, Basel There is more to our research than the Daily Close. To receive a comprehensive wrap up every day and our tactical FX and global models positioning or if you wish to be notified 24/7 with updates on key macro economic releases and/or technical breaches on our comprehensive investment universe covering world equity indices, bonds, FX, precious metals and commodities, take a free trial to the Bentin Daily, our premium research service. You may join our free trial by clicking here.

Important Disclaimer © Copyright by BentinPartner llc. This blog is not intended as a recommendation, an offer or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon and particular needs. This blog does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation or particular needs of any person who receives this report. Accordingly, the opinions discussed in this blog may not be suitable for all investors. You should not consider any of the content in this report as legal, tax or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner llc, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner llc. The content and views expressed in this report represents the opinions of Marc Bentin and should not be construed as guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner llc believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness or reliability of such information. This blog is also not intended to be a complete statement or summary of the industries, markets or developments referred to in the blog.

Comments