Weekly Trend Status Update

- Marc Bentin

- Oct 28, 2019

- 6 min read

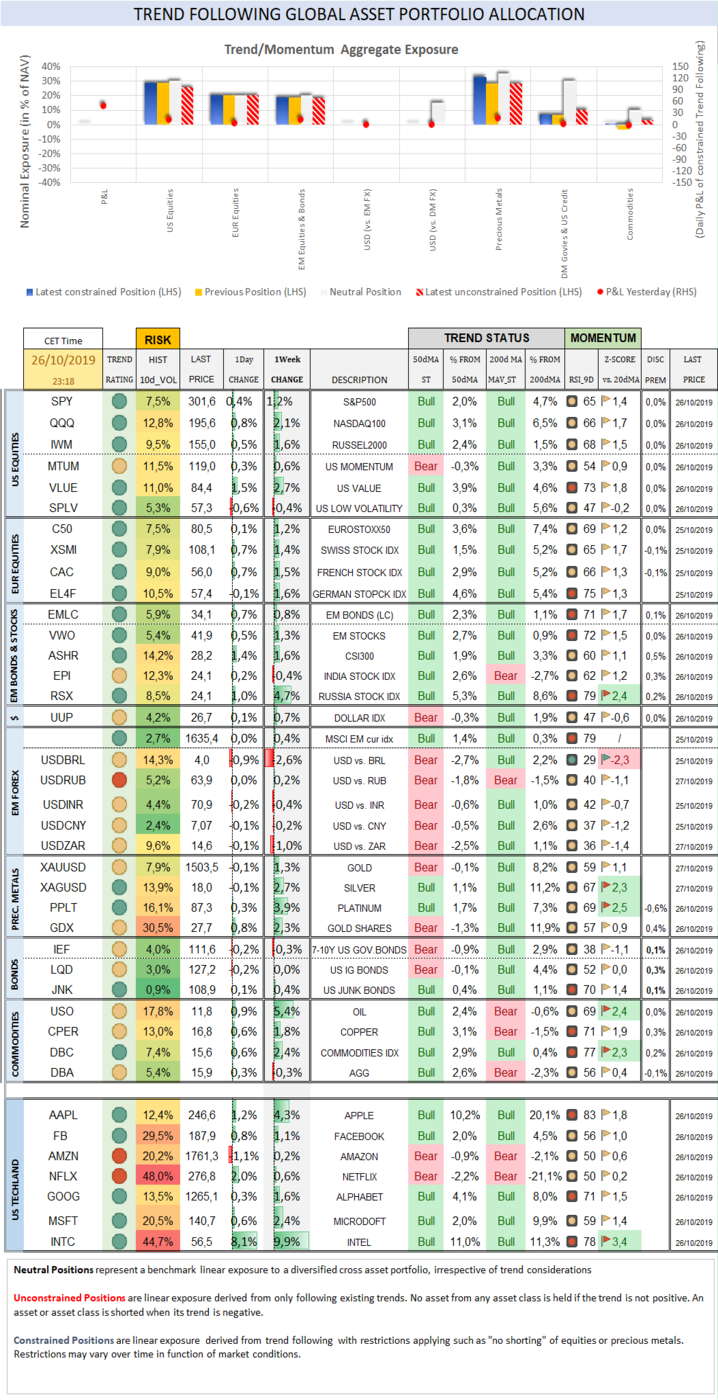

Equity and credit markets (and bonds and gold…) rallied for the most part last week, supported by the Fed (and the Bank of China) unleashing a larger than expected liquidity infusion on Thursday. More QE (or non-QE) liquidity infusion is all animal spirits need to be revived when sentiment and positioning remains overwhelmingly bearish and sceptical of the ongoing rally. Chances are this reluctant rally (probably one of the most hated ones in history) has more to go, fuelled occasionally as well by tailor made positive headlines on Sino/US negotiations. Cyclicals further outperformed last week and interestingly, commodities showed signs of bottoming out signals amidst an equally overwhelmingly bearish sentiment plaguing them (the speculative short positioning on copper is inter alia at an all-time highs). Larger than expected liquidity injections and solidifying expectations of upcoming Fed rate cuts when the S&P500 (which is to global equity markets what the sun is to solar system) tries to break on the upside is all that global stocks needed to do the same. The trading range on the S&P (and the 3000 barrier) had been in place for a while and baring an accident, now that it has been broken, it should rake in more gains over the near term, in our view. All of that being said, one has to also wonder what the tubing problems really are that are forcing the Fed to expand its balance sheet at an accelerating pace. Hopefully, it is not the data dependency of the S&P500 trading at all-time highs. Perhaps Marc Faber nailed it in his October newsletter (next to the point he made on conservative academic researchers being “called out”). According to him, liquidity troubles are likely caused by some large private equity firms struggling for financing. This ties in well with the ipo(calypse) market for Unicorns that is stone clogged and with the worst part of credit markets performing worst albeit in a contained fashion, at the present time. It is no coincidence that the money markets stress comes to light when “We Work” tries to restructure. VC’s that have valued and carried Unicorns at unreasonable (silly) prices are now left carrying their bag and needing financing for them. We are likely witnessing the end of the “growth at all costs” model that supersedes any other consideration about companies being capable (or not) to turn a dime of profit any time soon. This model is undergoing a ☢️ fusion in front of our eyes as public markets balk at being used as VC’s public toilets. This situation also ties well with the sense of near panic lingering despite the S&P500 now breaking all times high...courtesy of zero rates (Tina) and record buybacks (financed with negatively yielding debt in some cases). If the S&P climbs another 10% or 20% from here, maybe investors will accept to buy these unicorns again and unclog the system... That is the hope... Over the past week, the S&P500 gained 1,2% (20,7% YTD) while the Nasdaq100 rallied 2,1% (26,8% YTD). The US small cap index gained 1,6% (15,8% YTD). CBOE Volatility Index sold off by -11,2% (-50,2% YTD) to 12,65. Despite a week of decent results, analysts reduced estimates for the combined S&P500 earnings in 2020 by nearly USD1 to USD178.4. The Eurostoxx50 gained 1,2% (23,3%) as well. Diversified EM equities (VWO) gained 1,3% (10,1%), outperforming the S&P500 by 0,1%. CSI300 Chinese equity index (ASHR) gained 1,6% (28,5%). Indian shares (EPI) dropped -0,4% (-2,9%). Russian shares (RSX) rallied 4,7% (28,6%, Z-score 2,4). The Dollar DXY Index (UUP) recouped 0,7% (5,0%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,4% (1,3%). While the dollar rose last week vs. its G7 counterparts, it continued the move initiated earlier, underperforming EM currencies for the most part. USDBRL sold off by -2,6% (3,2%, Z-score -2,3). USDRUB gained 0,2% (-7,9%). USDMXN dropped -0,4% (-3,1%). USDINR dropped -0,4% (1,6%). USDCNY dropped -0,2% (2,7%). USDZAR dropped -1,0% (1,9%). Japan’s factory activity shrank at the fastest pace in three years in October, exposing broadening economic cracks from slowing global demand. At the same time, Japan’s exports contracted for the 10th straight month , adding to speculation that the central bank could ease monetary policy as soon as this week. 10Y US Treasuries dropped 4bps (-89bps) to 1,79%. The US government ended fiscal year 2019 with the largest budget deficit in 7 years at USD984bn or 4.6% of GDP (from 3.8% last year). JPMorgan said in a note that the stress in money markets that started last month will likely get much worse despite the injections. On the issue of bonds, the IMF also warned that bond funds worth USD1.7trn could face difficulties paying back investors promptly if volatility increases. It is raising concerns at the time when 15trn worth of government bonds are still yielding negatively with bond holdings constituting core holdings of international institutional investors. On Thursday morning the New York Fed raised its overnight repo operation from USD75bn to USD120bn and increased the next two term repos from USD35bn to USD45bn. 10Y Bunds added 2bps (-60bps) to -0,36%. 10Y Italian BTPs climbed 3bps (-179bps) to 0,95%, underperforming Bunds by 1bps. US High Yield (HY) Average Spread over Treasuries rallied -23bps last week (-166bps) to 3,60%. US Investment Grade Average OAS dropped -4bps (-53bps) to 1,19%. In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps (-52bps) to 0,58%. Gold rose 1,3% (17,2%) while Silver rallied 2,7% (16,4%, Z-score 2,3). Major Gold Mines (GDX) rallied 2,3% (31,5%). Bitcoin rallied 18,1% (163,8%, Z-score 5,2). Goldman Sachs Commodity Index rallied 3,0% (10,2%, Z-score 2,1). WTI Crude rallied 6,0% (24,5%, Z-score 2,0). Over the week end Asian share are 0.2% higher overnight. LVMH was reported over the week trying to buy Tiffany for USD14,5bn. The European Union is proposing to extend the deadline for Brexit by three months to Jan. 31, according to a draft declaration. That is one hurdle less for B. Johnson desire for snap elections on which British politicians will vote. Johnson remains short of the necessary two-thirds majority in the House of Commons, with Jeremy Corbyn reiterating on Sunday that he won’t back the (snap election) plan unless the threat of a no-deal Brexit is completely off the table while Johnson has made the ratification of his Brexit deal with Brussels contingent on MPs backing an early election…

———- To receive our daily updates and market reviews, consider our premium research: https://www.bentinpartners.ch/research And join our free trial. https://www.bentinpartners.ch/subscribe Important Disclaimer © Copyright by BentinPartner llc. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation or particular needs of any person who receives this report. Accordingly, the opinions discussed in this Report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner llc, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner llc. The content and views expressed in this report represents the opinions of Marc Bentin and should not be construed as guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner llc believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets or developments referred to in the Report. #fx #forex #investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants

Comments