Is Hedging for Gardeners Again?

- Marc Bentin

- Apr 13

- 6 min read

Updated: Apr 18

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

US stocks fluctuated to the tune of D. Trump’s Truth Social frustrated rage where he oscillated between genociding comments “a whole civilization will die tonight, never to be brought back again” (a comment that would have better suited Adolf Hitler than a US President) before holding a more conciliatory tone, opining “I agree to suspend the bombing and attack of Iran for a period of two weeks…” after the US President received a 10 point proposal which he said constituted “workable basis on which to negotiate” but which if agreed ….would have translated into a “capitulation without condition” of the US to Iran, something that only the naïve would believe D. Trump capable of doing…

“It is an Honor to have this Longterm problem close to resolution.”, D. Trump said in another deceiving comment despite being able to agree on nothing, except a maneuver to win time, gather more assets and reconstitute fast depleting air defenses for Israel while thinking about how to grab Iranian oil without causing mass casualties among US soldiers.

On the economic side, the US service economy expanded in March at a slower pace as employment shrank by the most since 2023 and input prices accelerated sharply (the ISM gauge of prices paid for services and materials jumped to 70.7, the highest since October 2022).

US applications for unemployment benefits rose last week with the number of Americans applying for jobless aid for the week ending April 4 jumping by 16,000 to 219,000 from the previous week’s 203,000.

US stocks gyrated up and down, essentially squeezing higher for most of the week, supported by constant manipulative comments aimed at precisely that…

As a Goldman strategist opined, “the positioning setup is constructive but the level is bearish”. How can we indeed imagine to have US equities hanging just a couple of % points away from all-time highs with a monetary, economic and geopolitical context as deleterious as it is today… It does not make any sense. And that is probably the most bullish part of the current setup.

The VIX dropped in response to a “breakthrough” cease fire even as it was violated half an hour later with a vicious attack that killed hundreds and hurt thousands in central Beirut after Israel hit without warning on Wednesday.

Hedging was the rational course of action since February 28th, but those hedges bled throughout the week with financial markets squeezing into a week end of negotiations that led…to nowhere, as was to be expected, with the same causes (inappropriate negotiators on the US side) likely to lead to the same absence of results.

In theory, a no deal “back to the stone ages” scenario holds potential to unleash market chaos but with the extent of market manipulation going on, nothing could in the end be more dangerous (besides trying to cross the SoH without Iranian authorization) than shorting this market or hold excessive hedging positions.

I suppose that the Fed and Trump Put(s) have been revived by poor economic data and a rapidly deteriorating private credit and AI bubble situation. At some point, what cannot be sustained ultimately will stop being sustainable but we are not quite there yet, it seems….and “stocks are too big to fall”.

While hedging is “complicated”, building an effective antifragile portfolio in today’s context is not easy either because as is customary in stressful periods, cross asset correlation has become extremely high…and everything is the same trade at any given time of Trump’s utterances.

Hedging stocks with short Sp500 futures requires to be (very) nimble but owning gold or silver against the risk of Armageddon is a near term fail as well, despite being the ultimate long-term solution.

Last week, the energy sector was the worst performing sector and also forced recalibration of (possibly) excessively overweighed positions while tech stocks outperformed, explaining in part why the SP500 squeezed.

Bond yields dropped a couple of bps on the week. Credit markets also squeezed with HY spreads dropping -40bps from the height of the crisis.

That said, Carlyle Group’s flagship private-credit fund was the latest to be hit with a wave of share-redemption requests. The Carlyle Tactical Private Credit Fund received repurchase requests amounting to roughly 15.7% of shares outstanding, more than three times the 5% redemption limit, the WSJ reported.

The dollar traded mostly but moderately lower last week with the US Dollar Index dropping 1.5% (+ 0.3% y-t-d).

Gold rallied last week as well (following stocks higher…), also supported by China’s central bank buying the most gold in more than a year in March, demonstrating that a key pillar of support for the precious metal remains intact.

Commodities dropped -2.7% on the week, driven by -14% drop in oil prices from its recent highs. Copper rallied 5.4% however.

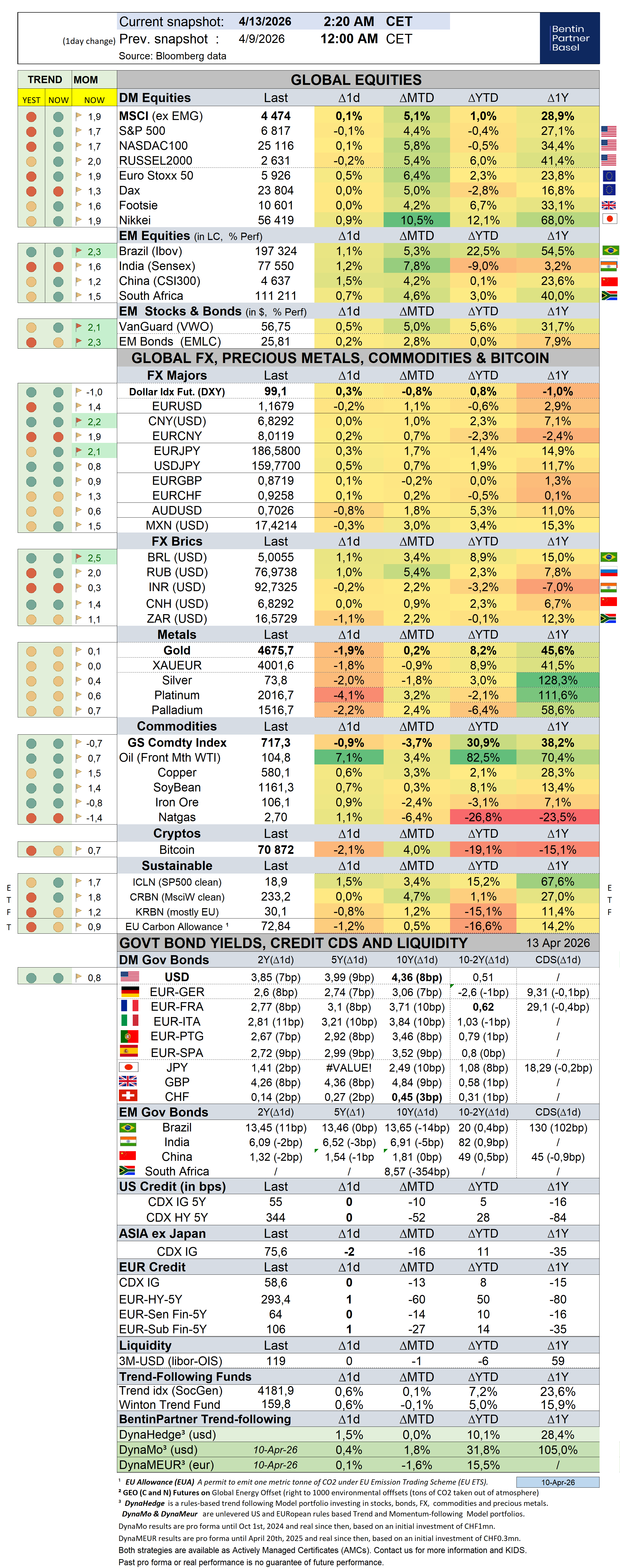

Over the past week, the S&P500 rallied 3,6% (-0,4% YTD) while the Nasdaq100 rallied 4,5% (-0,5% YTD). The US small cap index rallied 4,0% (6,2% YTD). AAPL gained 1,8% (-4,2%).

The Equally Weighed SP500 gained 1,8% (2,7% YTD), underperforming the S&P500 by-1,8%. The median SP500 YTD return closed the week at 1,4%.

Cboe Volatility Index sold off by -19,4% (28,6% YTD) to 19,23.

The Eurostoxx50 rallied 3,5% (2,6%), underperforming the S&P500 by -0,1%.

Diversified EM equities (VWO) rallied 5,4% (5,6%, Z-score 2,1), outperforming the S&P500 by 1,8%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -1,5% (1,5%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 1,1% (0,8%).

10Y US Treasuries dropped 3bps (19bps) to 4,36%. 10Y Bunds climbed 7bps (20bps) to 3,06%. 10Y Italian BTPs dropped -1bps (29bps) to 3,84%, outperforming Bunds by -8bps.

10Y French OAT’s dropped 3bps (14bps) to 3,71%, outperforming Bunds by -4bps.

US High Yield (HY) Average Spread over Treasuries dropped -21bps (12bps ) to 2,78%. US Investment Grade Average OAS dropped -2bps (2bps ) to 0,86%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -8bps (10bps) to 0,64%.

Gold gained 0,5% (8,2%) while Silver rose 1,3% (3,0%). Major Gold Mines (GDX) rallied 5,1% (15,9%).

Goldman Sachs Commodity Index sold off by -2,8% (27,5%). WTI Crude sold off by -7,1% (81,9%).

Overnight in Asia…

Ø S&P future -53 points; Hong Kong -0.9%; Nikkei -1.1%; China +0.2%

Ø US futures and Asian shares dropped on news of a failed week end of negotiations and as the US vowed to blockade Hormuz from 10 a.m. ET on Monday which also drove oil prices sharply higher (+8.5%) overnight.

Ø Iran’s Islamic Revolutionary Guard Corps responded to Trump’s call for a blockade by saying that any military vessels attempting to approach the strait “under any pretext” would be considered a violation of the ceasefire.

Ø A full blockade of the SoH will add further pressure to global oil markets, particularly China which is now also expected to enter the dance.

Ø D. Trump suffered another blow after Prime Minister Viktor Orban conceded defeat in Hungary’s Sunday’s election as D. Trump’s becomes the gravest threat to Europe’s right-wing parties…

Ø The zealous Christian that D. Trump claims to be said (among others) “I don’t want a Pope who criticizes the President of the United States because I’m doing exactly what I was elected, IN A LANDSLIDE, to do, setting Record Low Numbers in Crime, and creating the Greatest Stock Market in History.” Wouf wouf …Peace and Amen to that…

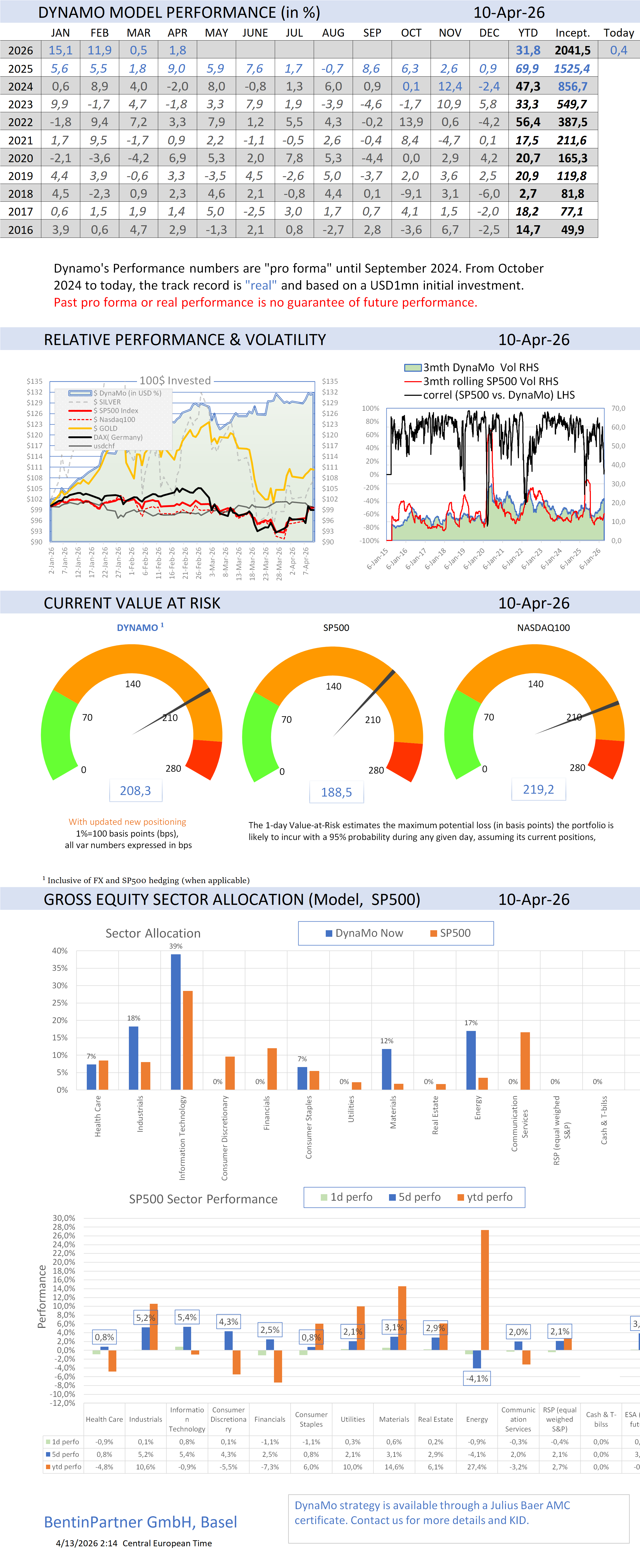

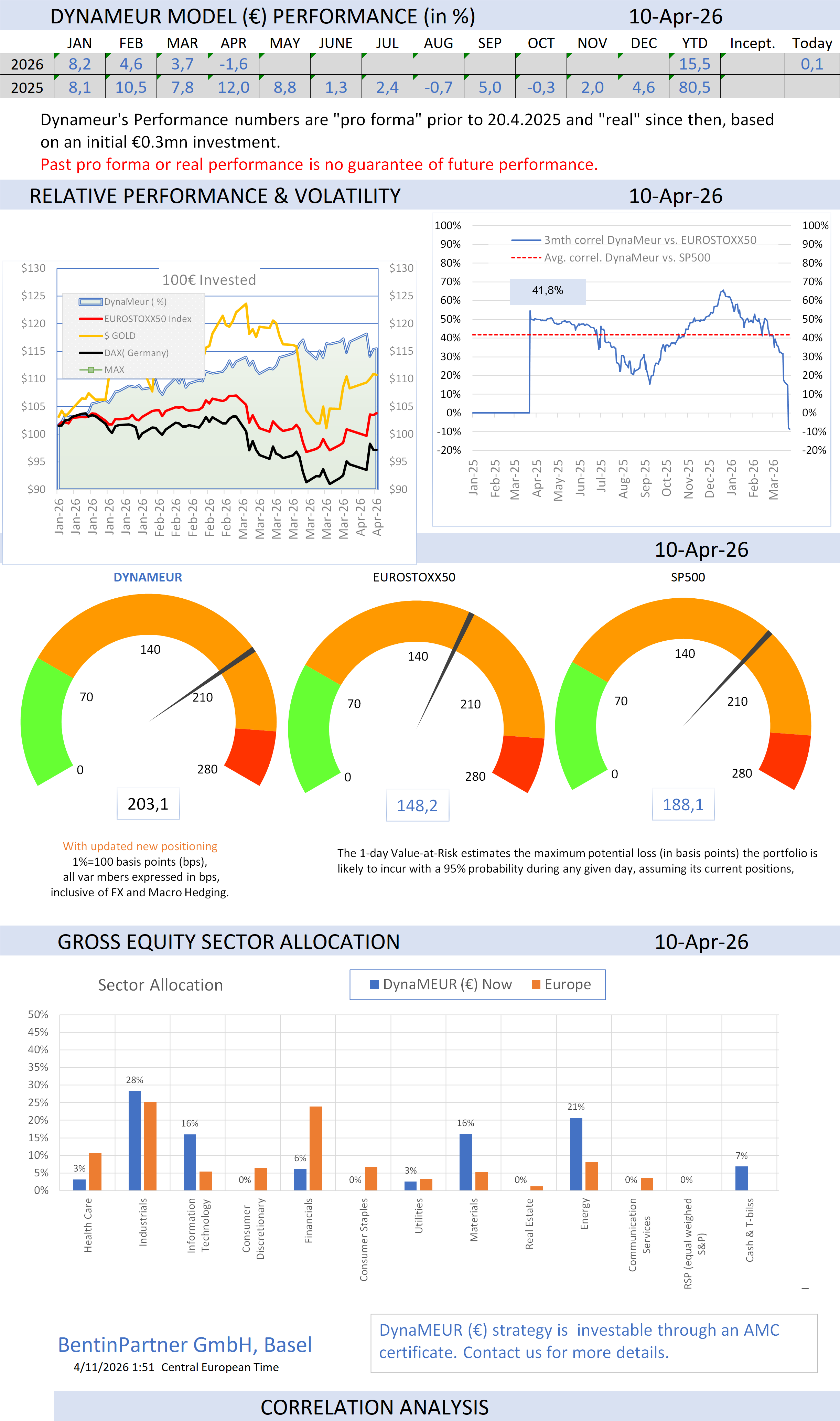

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments