TACO+...

- Marc Bentin

- Mar 31

- 7 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Wall Street staged a dramatic comeback with stocks climbing as oil fell on hopes that the war may be nearing a conclusion. US President D. Trump called on other nations to take control of the Strait of Hormuz, expressing his frustration that the monthlong war remains unresolved. “You’ll have to start learning how to fight for yourself” as the US “won’t be there to help you anymore,” he added, the latest sign he’s looking to exit a conflict that’s triggered a surge in oil and gas prices stoking fears of a global economic crisis. “Go get your own oil!” he added. The US President also said that “regime change” in Iran had de facto already materialized…

US Defense Secretary Pete Hegseth also said that talks to end the war with Iran are “gaining strength” and the US military would maintain pressure to compel Tehran to make a deal. A “regime change has occurred” in Iran, he also commented.

Iran for its part said it was prepared to end the war if security guarantees were offered, calling ongoing negotiations, “just messages.”

Tehran also kept up strikes on Israel and countries around the Persian Gulf, including the United Arab Emirates and Saudi Arabia, with one attack hitting a large Kuwaiti oil tanker off the coast of Dubai on Tuesday.

On the economic front, data showed consumer confidence unexpectedly rose in March on slightly more upbeat views of business and labor-market conditions but investors and consumers need to see notable de-escalation in the Middle East and some relief at the gas pump before confidence can rebound significantly.

Job openings fell and hiring slowed in February, pointing to cooler labor demand prevailing before the war.

The dollar dropped as bond yields declined and, I reckon, with the perspective that a US strategic defeat in Iran (it will not be depicted as such) could leave investors in the Middle East and elsewhere wonder what is next with US policy (the cost of the war will further deteriorate public finances making the need for more accommodative policy even more pressing) and what is the point of piling on more USD reserves… This questioning comes at a time when investors such as so-called Bond King J. Gundlach continue to believe that the US could at some point proceed to a debt restructuring by for example reducing the coupon of outstanding US Treasuries… on top of the usual methods more commonly used to deflate debt away (money printing and inflation).

Since the advent of the Petrodollar, the explicit or implicit reason to own US dollars was to recycle USD oil proceeds into US assets to alleviate the US twin deficits in exchange for US military protection. The problem is that the exact opposite of the initial objective has now materialized with the war in Iran inflicting enormous damage throughout Gulf countries simply because of their allegiance to the US and the targets that constituted US military bases in the region.

For what it worth, we have reinstated a long CNY/USD position as a cautious initial way to return to the theme of expected dollar weakness.

Gold (+3.5%) and even more so silver (+7%) rallied strongly as risk appetite stormed back across asset class with bonds also starting to come to terms with the reality that after all the Fed may soon start to cut interest rates and do whatever is required to ease financial conditions and bring yields down. The violence of the move yesterday occurred as most of the speculation in precious metals was previously washed away by a very adverse price action in March. We also bought back some silver…lifting “paper” hedges.

The consequences of a US/Israel strategic defeat (it is still too early to call it that) will/would be far reaching, so much so, that I would be very surprised if the current deescalation initiated by D. Trump was not another deception and a step back to better push forward in a few weeks’ time.

The political wounds inflicted on D. Trump from a war that has failed so far to meet its objectives (a minima, regime change, oil grabbing and control seizure of the Strait of Hormuz) are deep. If the US President is forced (as seems to be the case today) to leave the war at that (including, beyond hitting missile launchers and nuclear sites, with the bombing of schools, hospitals, the electrical grid, the industrial base and the food industry of Iran), he will have contributed to leave a US reputation and credibility (for anything else than make things go Boum!) in shambles among foes and friends alike.

The pan European EU rejection of the legality, moral legitimacy and motives advanced for this war left France, Spain, Italy, Portugal, Switzerland and even Poland (and more) aligned to decline participation in the conflict and/or to refuse the use of US bases or flying over authorizations, that all render the pursue of the war more complicated, especially with carriers forced to retreat for servicing and repairs (due to laundry fires, Iranian missiles or both).

D. Trump lost much support in Europe (and pretty much elsewhere in the world) and sadly enough, because some of his ideas were salutary …but the moment of retribution could be approaching if he fails... Trump has not pursued a very different strategic agenda so far than many US Presidents before him but everybody will remember the brazenness of his actions, his “in your face” method of communication and the extreme vulgarity of his public rhetoric.

Even if it too early to write his obituary… another collateral victim of this conflict will be NATO from which “Daddy” likely now wishes to part ways with after being refused support for his misguided campaign in Iran.

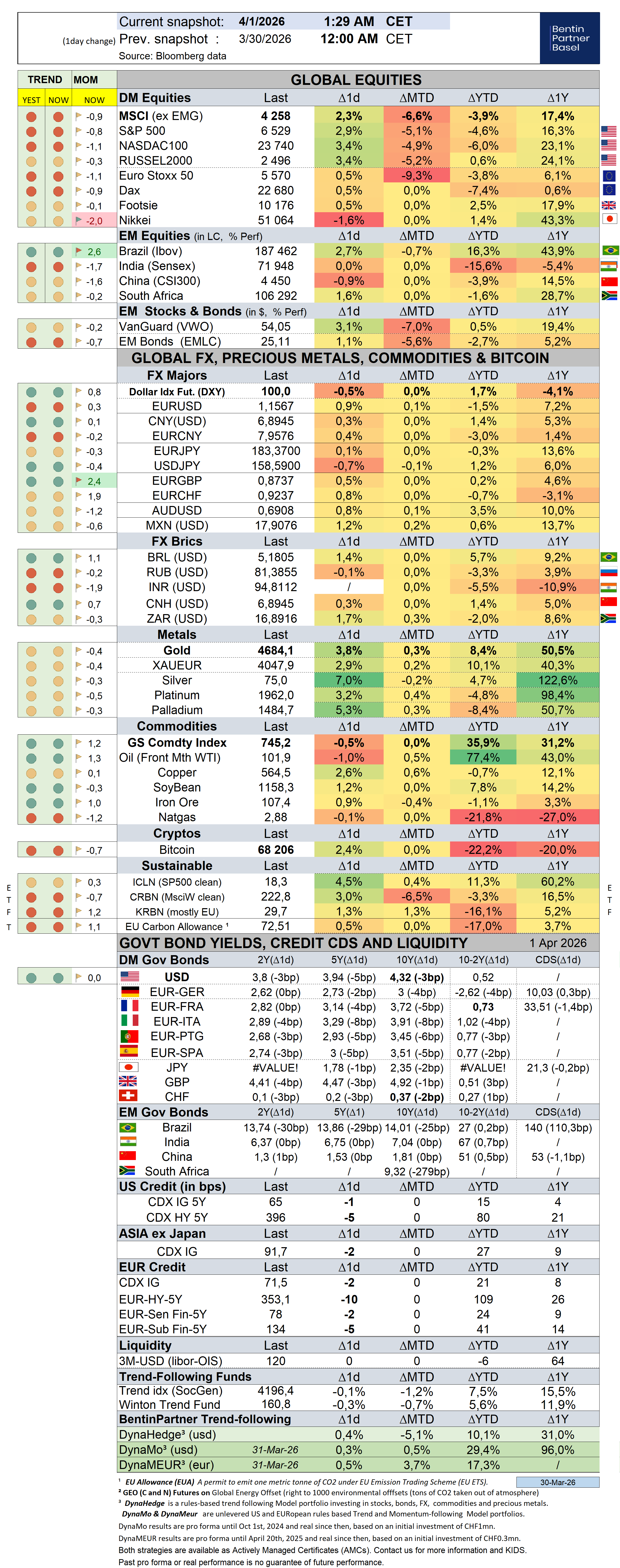

S&P500 rallied 2,9% (-4,6% YTD) while the Nasdaq100 rallied 3,4% (-6,0% YTD). The US small cap index rallied 3,5% (0,7% YTD).

The equally weighed SP500 Index rallied 2,0% (0,2% YTD), underperforming the S&P500 by -0,9%.

The proportion of stocks in the SP500 index trading above their medium- and long-term trend stand at 2,6% and 46,5% respectively.

Cboe Volatility Index dropped -17,5% (68,9% YTD) to 25,25.

The Eurostoxx50 gained 0,4% (-3,8% ), underperforming the S&P500 by -2,5%.

CSI300 Chinese equity index (ASHR) gained 1,3% (-0,6%), underperforming the S&P500 by -1,6%.

Diversified EM equities (VWO) rallied 3,1% (0,5%), outperforming the S&P500 by 0,2%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,7% (2,8% YTD) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,1% (-1,1% YTD).

RUBUSD was unchanged (-3,2%). INRUSD rallied / (-5,2%). CNYUSD gained 0,3% (1,4%). ZARUSD gained 1,7% (-2,0%). MXNUSD gained 1,2% (0,6%).

EURUSD gained 0,9% (-1,5%). EURCHF gained 0,8% (-0,7%). EURJPY gained 0,1% (-0,3%). EURGBP gained 0,5% (0,2%, Z-score 2,4).

10Y US Treasury yield dropped -3bps (15bps) to 4,32%, with the 10/2 spread at 52 bps (8,8). 30Y US Treasury yield was unchanged (7bps) to 4,91%.

10Y Bund yield dropped -4bps (15bps) to 3,00%. 10Y French OAT yield dropped -5bps (16bps) to 3,72%, matching Bunds.1bp.10Y Italian BTP yield dropped -4bps (36bps) to 3,91%, matching Bunds.

US Investment Grade Average OAS dropped -1bps (11bps) to 0,95%. US High Yield (HY) Average Spread over Treasuries dropped -5bps (51bps) to 3,17%. US High Yield (HY) Caa Average Spread over Treasuries dropped -18bps (110bps) to 7,25%. USD Repo Govt GC ON closed at 3,75% while the US Federal Funds Effective Rate stood at 3,64%.

XAUUSD rallied 3,8% (8,4%) while Silver rallied 7,1% (4,7%). Major Gold Mines (GDX) rallied 7,0% (7,0%). Bitcoin rallied 2,4% (-22,2%).

Goldman Sachs Commodity Index dropped -0,5% (35,9%). WTI Crude dropped -1,0% (77,4%). COPPER (COPA IM) gained 0,7% (-1,2%).

Overnight in Asia…

Ø S&P future +7 points; Hong Kong +2%; Nikkei -4.4%; China +1.5%

Ø Asian stocks bounced back from their worst month in more than 17 years on optimism the Middle East conflict may be nearing a conclusion, Bloomberg commented.

Ø D. Trump said he would address the nation for an important update on Iran war on Wednesday. “We’ll be leaving very soon” (seemingly in 2 to 3 weeks), he said, brushing aside the idea of having to reach a deal “Iran does not have to make a deal. It is a new regime and they are much more accessible.It is irrelevant now.

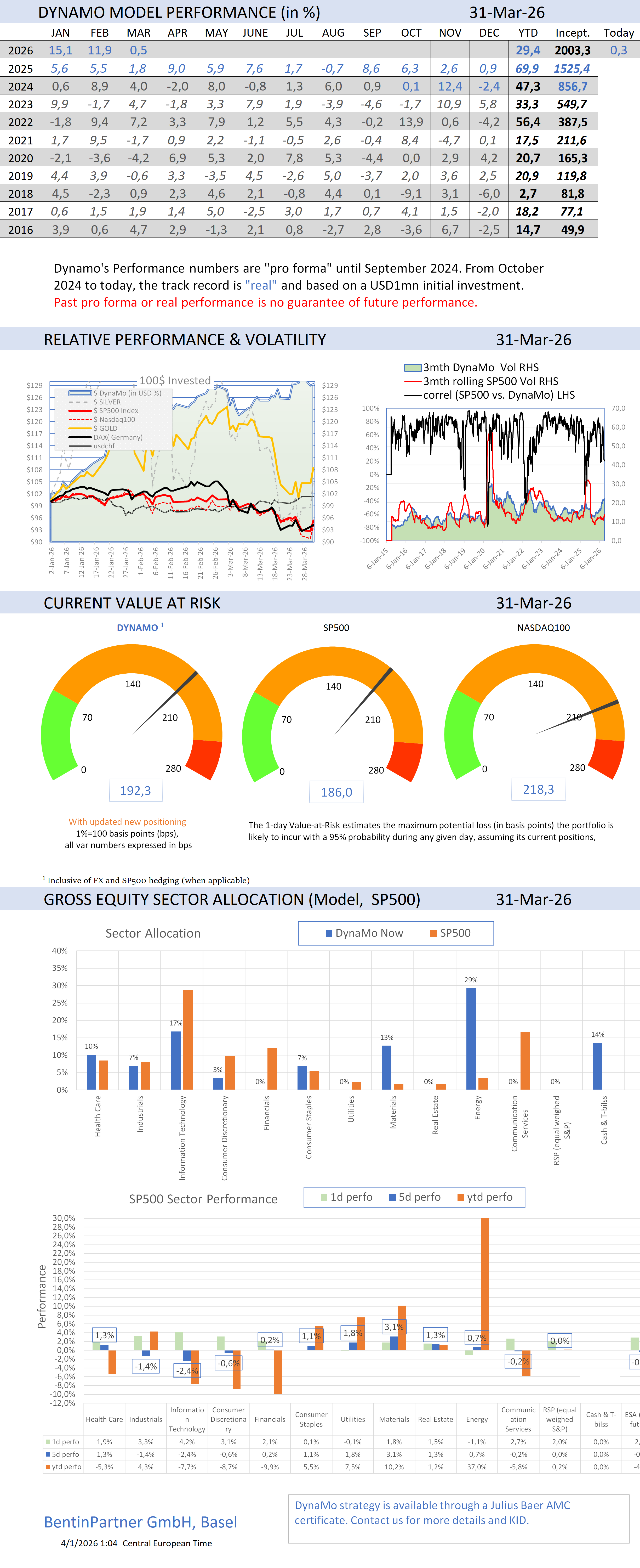

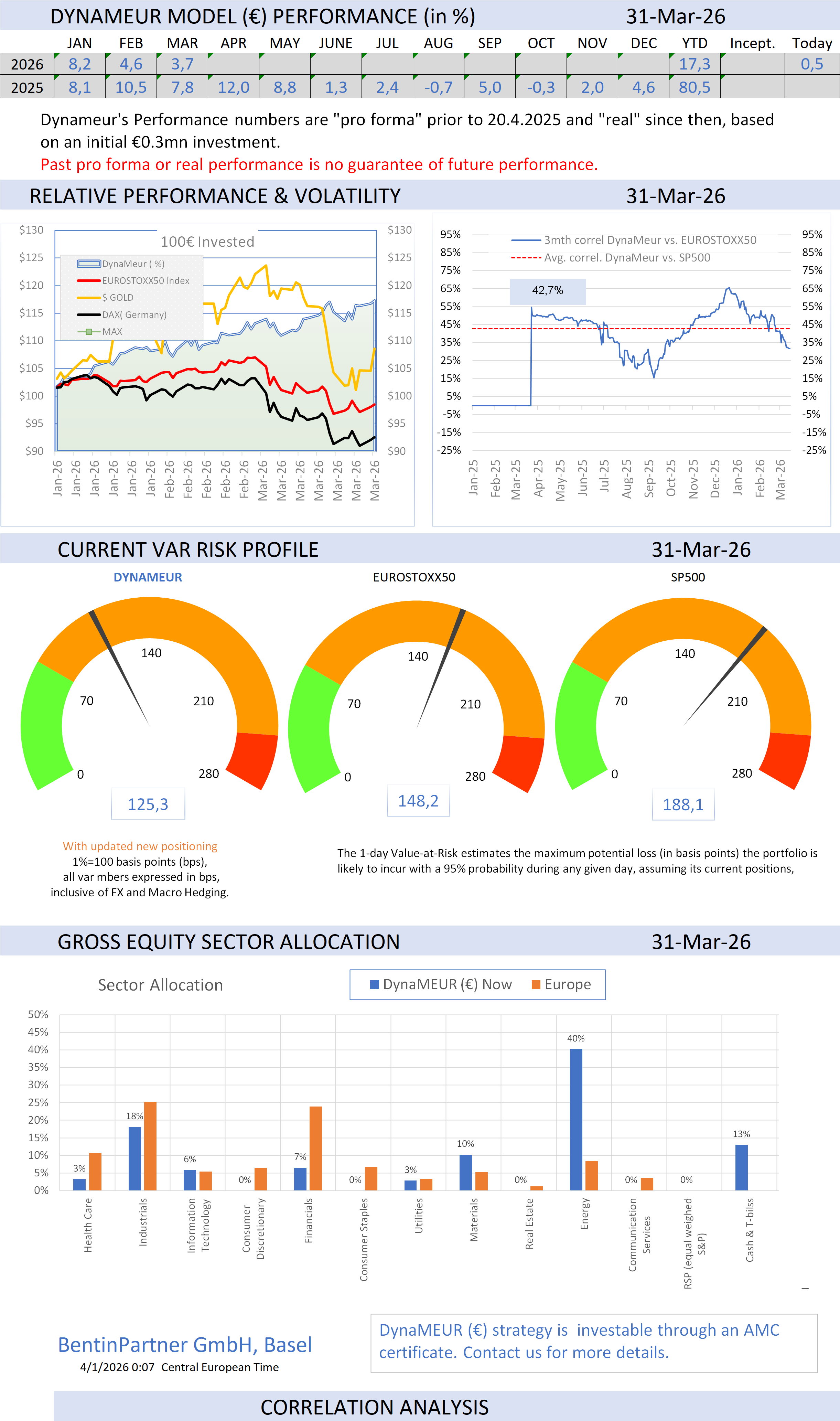

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments