Stocks and Bonds Cavernous Divide..

- Marc Bentin

- May 4

- 8 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

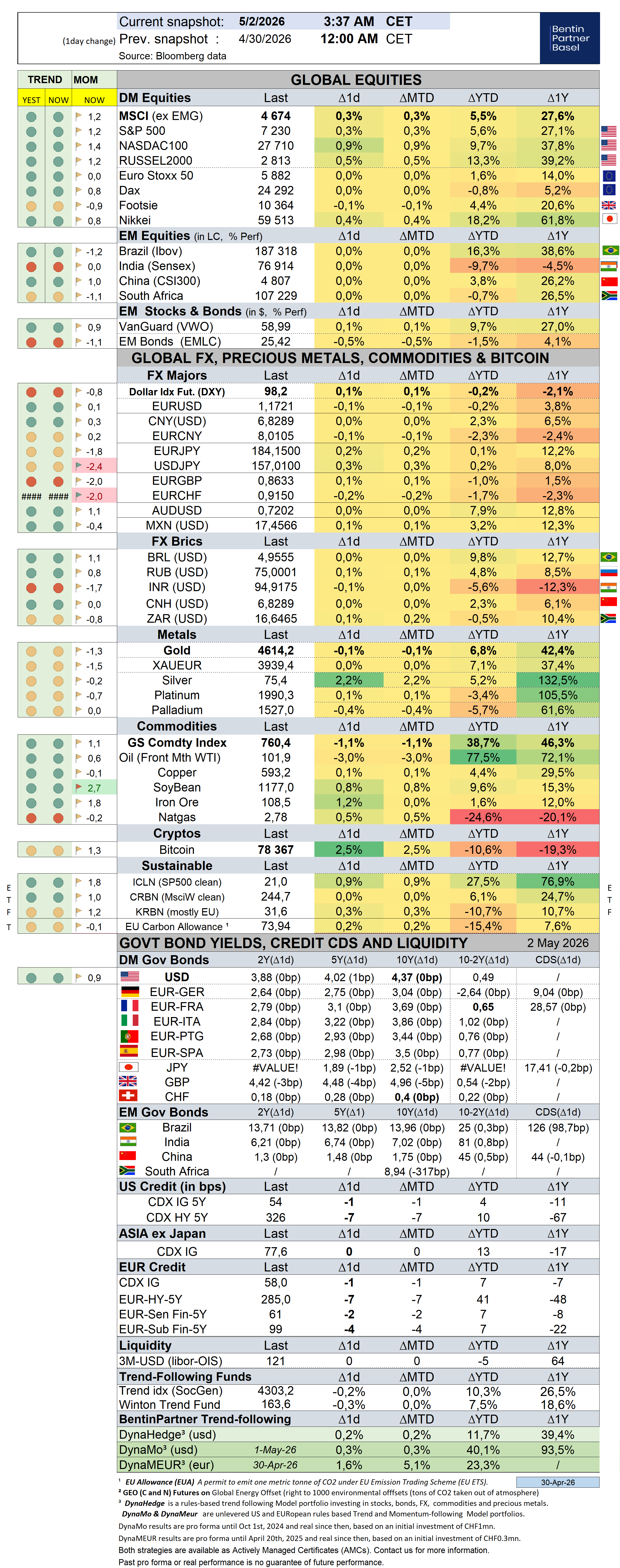

US stocks witnessed another week of (moderate) gains, still finishing April at all time highs with 81% of stocks so far in the reporting period, beating expectations.

The Fed’s decision on Wednesday to leave rates unchanged, keeping an easing bias, despite an unusually fractious FOMC vote that saw four officials break from the consensus.

On the economic side, US data came unusually strong with jobless claims tumbling to their lowest level in more than 50 years last week (-26k to 189k) while US orders for business equipment also increased in March by the most since mid-2020, extending a yearlong stretch of solid capital investment fueled by spending on artificial intelligence (with core capital goods jumping 3.3% (from 1.6% in February), according to Bloomberg. The ISM Manufacturing Index was unchanged at a four-year high of 52.7, with 13 industries reporting growth versus only three experiencing a contraction. April Personal Income was also reported up 0.6% (double forecast).

While this may confront the Fed with overheating risks, directly related to the AI super investment cycle and to investors remaining exuberant about stock markets prospects, D. Trump’s policy to save the mid-term elections, despite the chaos caused in the lower echelons of society by soaring energy prices, remain centered about getting stocks creeping higher with Wall Street also working to keep the ground fertile enough for this Summer’s coming IPOs that will turn MAG7 into MAG10 (SpaceX, Anthropic, Opean AI). (See article from the Economist suggesting that these 3 stocks are already driving the market higher through the revaluation of companies owning shares of them).

Bonds, as has become customary, stayed dissociated from stock markets enthusiasts as 10Y US yields climbed 10 bps on the week (to 4.37%) with inflation still pressing higher. For what it is worth, Fitch Ratings warned the US’s credit grade faces the challenges of a widening deficit that leaves its debt burden ‘far above’ other nations sharing a AA score.

Higher inflation, out of control issuance and dropping foreign appetite for US treasuries remain a poor recipe for the forward-looking return of long dated treasuries going forward and an asset class that we continue to shun altogether (except for tbills), preferring to barbell stocks with gold for much of our asset allocation.

While the usual players in the private sector tried to reassure markets last week (with some success as their share price rose), private credit is slated to become the next focus of the Financial Stability Board’s task force on nonbank data, as regulators globally step up their scrutiny of the ballooning asset class, Bloomberg reported. J. Dimon (JPM’s CEO) also and again cautioned that a credit market downturn could be worse than expected… “In private credit specifically, the fact that there are more than 1,000 firms in the space probably means not all of them will fare well when the cycle turns”, he said. In the same vein, Apollo’s former risk chief has warned that some Wall Street-backed life insurers will be ill-prepared to manage policyholder funds in a downturn…Chak Raghunathan said some newer life insurers could struggle to stay afloat, citing their heavy reliance on private credit and newer savings products that may be vulnerable to policyholder withdrawals, the FT reported.

On currencies, the highlight late last week was BoJ intervention that saw the yen increase by (a still modest) 1.5% which derailed the dollar index tepid weekly gains, leaving it weaker by -0.4% on the week. CNY continued to grind higher (+0.6%, +2.4% YTD) as well, with low volatility.

The Bloomberg commodity index jumped 3% (+28% YTD) supported by an 8% gain for oil while gold dropped -2% and silver -0.5%.

Last week, UAE announced it will leave OPEC effective May 1, stripping the oil cartel of its third-largest producer and further weakening its leverage over global oil supplies and prices. The move which will likely further strain relations with Saudi Arabia, so far had minimal impact on oil prices but it is believed UAE has several more mbd to bring to the market.

On the geopolitical scene, German Chancellor F. Merz said the US was ‘being humiliated’ by Iran, as the German chancellor warned that he saw ‘no exit strategy’ to end the Middle Eastern conflict any time soon, adding that the Iranians were ‘obviously negotiating very skillfully— or simply very skillfully not negotiating’,

Unsurprisingly perhaps, this triggered the ire of D. Trump who announced he was pulling 5’000 US soldiers out of Germany (some 100’000 are stationed on EU soil), promising to consider additional withdrawals from Italy and Spain.

In the meantime, while must of the attention remained centered on the developments in Iran, the war in Ukraine is slowly but surely taking a much more dangerous turn with drones (some of which built outside of Ukraine) last week with attacks on the Russian oil infrastructure going as deep as 1’000 miles from the Ukraine border. Russia is unlikely to tolerate this for much longer and the absence of forced restraint on Ukraine (likely emboldened by a now approved EUR 90bn loan that will never be reimbursed and continued talks of an accelerating adhesion of Ukraine to the EU) are, in our view, only bringing Europe as whole, closer to a direct confrontation with Russia (in the total indifference or delusion of local politicians), at the exact moment where the US increasingly desolidarizes itself from Europe. In this context, economic prospects and confidence in and within Europe are likely to keep deteriorating at a faster pace.

A glimmer of hope and common sense came (again) from Belgium’s Prime Minister Bart De Wever announcement that the Belgian state will take full control of all seven nuclear reactors, halt all decommissioning, and begin negotiations to nationalize the entire nuclear fleet currently operated by Engie (which itself previously had absorbed Electrabel, an internationally recognized Belgian national champion central to Belgium and France energy system), stating that a country with nuclear ambitions cannot rely on an operator that wants to exit the sector.

Over the past week, the S&P500 gained 0,9% (5,7% YTD) while the Nasdaq100 gained 1,5% (9,7% YTD). The US small cap index gained 1,0% (13,5% YTD). AAPL rallied 3,3% (3,0%, Z-score 2,1).

The Equally Weighed SP500 gained 0,4% (5,9% YTD), underperforming the S&P500 by-0,5%. The median SP500 YTD return closed the week at 2,6%.

Cboe Volatility Index sold off by -9,2% (13,6% YTD) to 16,99.

The Eurostoxx50 was unchanged (2,3%), underperforming the S&P500 by -1%.

Diversified EM equities (VWO) dropped -0,1% (9,7%), underperforming the S&P500 by -1,0%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,3% (1,4%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,1% (0,7% ).

10Y US Treasuries underperformed with yields rising 7bps (20bps) to 4,37%. 10Y Bunds climbed 4bps (18bps) to 3,04%. 10Y Italian BTPs underperformed rising 8bps (31bps) to 3,86%, underperforming Bunds by 4bps.

10Y French OAT's dropped 5bps (13bps) to 3,69%, underperforming Bunds by 1bps.

US High Yield (HY) Average Spread over Treasuries dropped -8bps (-2bps) to 2,64%. US Investment Grade Average OAS climbed 0bps (1bps) to 0,85%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -1bps (7bps) to 0,61%.

Gold sold off by -2,0% (6,8%) while Silver dropped -0,5% (5,2%). Major Gold Mines (GDX) sold off by -7,7% (1,6%).

Goldman Sachs Commodity Index rallied 3,2% (37,8%). WTI Crude rallied 8,0% (77,5%).

Overnight in Asia…

Ø S&P future +6 points; Hong Kong +1.7%; Nikkei+0.4%; China -0.1%

Ø President D. Trump said late on Sunday that the US will begin guiding some neutral ships trapped in the Persian Gulf out through the Strait of Hormuz starting Monday. “The Ship movement is merely meant to free up people, companies, and Countries that have done absolutely nothing wrong — They are victims of circumstance….” said D. Trump in substance (or his AI chatbot given the unusual length and considerate tone of his “tweet”).

Ø US futures (stocks and oil) reaction so far has been fairly muted (still erasing a quick 3% loss for oil) after a senior Iranian official warned that Tehran would consider any US interference in the SoH a ceasefire breach.

Ø Asian shares rallied, led by Korea’s tech heavy Kospi gaining 2.8% in response to the strong US close and SP500 closing April at all time highs on strong earnings reports from the AI driven tech sector that was led on Friday by a strong release, solid iphone sales and a buy back announcement that triggered some catch-up action of AAPL (which is a heavy weight in the Sp500 and Nasdaq index).

Ø Over the week end, D. Trump had described discussions with Tehran as “very positive”. Still, Iran’s proposal called for a complete end to the conflict within 30 days along with guarantees against renewed strikes. The plan reiterated Tehran’s earlier demands, including that US forces withdraw from near Iran, a maritime blockade be lifted, sanctions removed and reparations paid, it said. It likely still remains a draft.

Ø Concern about a possible euro-area recession is “real and justified” as conflict in the Middle East causes a supply-side disruption, Greek ECB Governing Council member Yannis Stournaras said in a week end interview.

Ø JPY is “quiet” following Thursday BoJ intervention. The EU economic surprise index is now falling sharply, suggesting most data are now falling faster than expected as the EU economy bows under pressure of higher energy prices caused by the wars in Iran and Ukraine and an obvious lack of adequate policy response.

Ø Secretary of State Marco Rubio will travel to Rome later this week to meet with Vatican officials and Foreign Minister Antonio Tajani. Will he apologize or “threaten” to withdraw more US troops from Italy (which seems to be the new bargaining chip of the US administration)?

Ø Greg Abel earned wide praise from shareholders for his leadership and management abilities but the aura created by his predecessor and mentor Warren Buffett has begun to fade and empty seats were noticeable throughout Berkshire's annual shareholder weekend in Omaha, Nebraska, the first since Abel succeeded Buffett as CEO in January, Reuters wrote.

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments