A Two-Tiered Economy...

- Marc Bentin

- Sep 22, 2025

- 9 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Last week delivered the largely anticipated 25bps easing (to 4.25%) in the Fed funds with an 11-1 vote, signaling less dissent than anticipated at the board level. As expected, newly installed Governor Stephen Miran was the only policymaker voting against, advocating a half-point cut.

The Fed Chair sent a warning to the consensus view that a series of rate cuts are baked in “It’s gratifying to see that economic activity is holding.” “Consumer spending numbers were well above expectations.” “I think the economy is – it’s moving along.”

At the same time, the Fed leaned heavily on its “full employment” mandate, saying “Payroll job gains have slowed significantly…, still opining that a good part of the slowing likely reflected a decline in the growth of the labor force, due to lower immigration and lower labor force participation.”

In any case, the Fed’s rate cut decision unleashed another wave of buying/squeezing among risk assets (and precious metals) although bond markets did not participate in the broad rally, closing the week slightly worse off, raising some eyebrows.

After listing the impressive Ytd returns from a whole range of assets, Goldman trader Paolo Schiavone, opined that behind this seemingly relentless frenzy to buy everything, lies a certain sense that hyperinflation is looming, or as he puts it "There’s a sense that money is losing value anyway, so better to use it now than hold it"

BoA Strategist Hartnett conveyed a similar message attributing the move in risk to "tariff cuts, tax cuts, rate cuts…”run-it-hot” US policy, implicit guarantee economy & stocks “too big to fail”; and biggest jump in US mortgage refi since Mar'20 on lower rates says Fed cutting into acceleration."

It is difficult to contest the bubble argument. But it remains that the best thing to do with a bubble, after leaving it on time, is to ride it as long as possible and especially through its last phase which is usually the most powerful.

BoA Strategist Hartnett’s summarized his "how to trade a bubble” saying;

“There have been 10 equity bubbles since 1900:

The average trough-to-peak gains are 244%, ending with average trailing PE of 58x, and equity index trading 29% above 200dma

Today, the Mag7 is the best bubble proxy... it is up 223% since Mar'23 lows, and trades at a trailing PE of 39x, and is currently 20% above 200dma, i.e. more to go.”

To Hartnett, the best equity trade for growth up/yields down is long small cap, REITs, biotech…noting that small cap in US (up 8% YTD) have been lagging big, small cap in China 51%, EU 25%, Japan 25%.

ZH also opined …”there is 3 months left until bonus time: "you buy the junk — the lowest-quality, highest-beta names — not because you believe in them, but because benchmarks demand it"... "If the junk keeps rallying, you survive; if it turns, you blow up, but at least you weren’t alone." So for all those hedge fund managers who are underperforming the market (and certainly retail investors) they have no choice but to chase the high beta momentum names, and sure enough, take one look at Goldman's high-beta momo basket: we have just witnessed the biggest one-month surge in history!”

There may be some truth in this (reckless) statement as well, considering that sentiment among hedge fund managers has been too cautious this year and that many of them are running behind the tape.

In this context, the BIS also warned: “Recent gains in financial markets don’t adequately reflect dangers looming from higher sovereign debt and disrupted world trade in both stocks and credit, cheered by prospects of government spending and lower borrowing costs, have driven buoyancy that might paint a brighter picture for the world than warranted. ‘This very sanguine assessment seems to be disregarding some of the very real challenges in the real economy,’ Hyun Song Shin, head of the BIS’s monetary and economic department, told reporters. Markets are ‘vulnerable to repricing from bad news,’ he added… Shin echoed earlier warnings by his institution that national borrowing burdens seen around the world are reaching levels that are at the limits of sustainability. ‘Historical experience shows that market stress can emerge long before debt levels exceed textbook definitions,’ he said.”

At the same time, the BIS said US authorities should consider “looking through” the inflationary impact of President Trump’s record import taxes “ (and thus cut rates).

“The current level of US tariffs — the highest since the 1930s — would raise estimated inflation in the US economy by 3 per cent and lower economic growth by 1 per cent over the next 12 months, the BIS said. However, if the Fed chooses to tolerate higher inflation, the hit to the US economy over three years would fall from an estimated 1.6 per cent of GDP to just 0.1 per cent of GDP, the BIS said.

US Economic data mostly came on the stronger side last week.

- Retail sales rose more than expected than-expected in August (by 0.6% MoM vs. July, when sales were also up a revised 0.6%).

- At the same time US jobless claims retreated significantly last week after surging to a nearly four-year high a week earlier, falling by 33,000 to 231,000 (less than the expected 241,000.

- Finally, US factory production unexpectedly rose in August amid a rebound in the output of motor vehicles and some nondurable goods, though tariffs continued to cast a shadow over the manufacturing sector.

- Mortgage rates last week dropped to the lowest level since October of last year, leading applications to refinance a home loan to jump 58% from the previous week. This came despite sentiment among US homebuilders remaining at one of its lowest levels in years in September, underscoring some cooling off in the housing market.

Actually, the US economy now boils down to a two-tiered economy;

- There are two economies in the U.S. right now, and they are moving in different directions. For high earners and many older Americans, the economy looks robust. They are still spending generously while their 401(k) accounts and homes soared in value… Wealthy consumers continue to account for a growing share of US consumer spending, highlighting the lopsided strength of the economy as a slowdown in hiring and wariness among other income cohorts raise fears of a slowdown.

- A recent Moody’s report best summarized the situation writing that consumers in the top 10% of the income distribution accounted for 49.2% of total spending in Q2 (up from 48.5% in Q1), reaching the highest level in data going back to 1989, a Moody’s report showed. The fact that 87% of US stocks belong to the top 10% of the population was likely another illustration of the same phenomenon of concentrated wealth leading to a two-tiered economy.

Last week’s only surprise perhaps was the dollar initially selling off to new lows for the year before closing higher and bond yields doing the same, initially dropping 2-3 bps before closing 8 bps higher as the Fed expressed concerns about the job market, seemingly overriding concerns about inflation, but still signaling a shallow sequence of interest rate cuts and more precisely 2 more rate cuts for this year.

In China, China’s internet regulator has banned the country’s biggest technology companies from buying Nvidia’s artificial intelligence chips, as Beijing stepped up efforts to boost its domestic industry and compete with the US. The Cyberspace Administration of China told companies, including ByteDance and Alibaba, last week to end their testing and orders of Nvidia’s tailor-made (watered down) product for the country. A blistering rally in Chinese technology shares accelerated mid last week as renewed bets on local AI ventures sent a key gauge to the highest in nearly four years. Search engine operator Baidu led gains with a 16% on Thursday.

China’s factory output and retail sales rose but less than expected, keeping pressure on Beijing to roll out more stimulus to fend off the slowdown… Industrial output grew 5.2% year-on-year while Retail sales rose 3.4% in August, cooling from a 3.7% rise in the previous month.

Elsewhere, on the heels of the murder of conservative influencer Charlie Kirk last week, the WSJ noted that “the White House is moving swiftly to galvanize the outpouring of support for slain conservative activist Charlie Kirk into political momentum (going into the Midterms), as President Trump’s advisers weigh a slate of executive actions targeting liberal organizations. Among the actions being discussed by the president’s team: reviewing the tax-exempt status of left-leaning nonprofit groups and targeting them with anticorruption laws, according to administration officials. The president could begin rolling out the actions as soon as this week, officials said, part of a bid to harness support for Kirk, particularly among young voters, ahead of the midterm elections. Officials across the administration are working to identify groups suspected of targeting conservatives or causes conservatives’ support.”

President D. Trump also added The New York Times to the list of media companies he’s challenged in court, filing a $15 billion defamation lawsuit that targets four of its journalists in a book and three articles published within a two-month period before the last election… Trump called the Times ‘one of the worst and most degenerate newspapers in the nation’s history’ and a virtual mouthpiece for Democrats.

We are getting closer to a situation where the First Amendment right to free speech might now be in jeopardy on the pretext of defending free speech…

French yields climbed 5 bps to 3.55% with the French to German 10-year bond spread widening about two to 80 bps as the political situation remained in flux.

Over the past week, the S&P500 gained 1,0% (13,2% YTD) while the Nasdaq100 rallied 2,2% (17,2% YTD, Z-score 2,4). The US small cap index gained 1,9% (10,0% YTD). AAPL rallied 4,9% (-2,0%, Z-score 2,6).

The Equally Weighed SP500 gained 0,1% (8,0% YTD), underperforming the S&P500 by-0,8%. The median SP500 YTD return closed the week at 7,5%.

Cboe Volatility Index rallied 4,7% (-11,0% YTD) to 15,45.

The Eurostoxx50 gained 1,3% (14,0%), outperforming the S&P500 by 0,3%.

Diversified EM equities (VWO) gained 0,8% (22,4%), outperforming the S&P500 by -0,1%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 0,1% (-6,8%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,3% (7,2%).

10Y US Treasuries underperformed with yields rising 6bps (-44bps) to 4,13%. 10Y Bunds climbed 3bps (38bps) to 2,75%. 10Y Italian BTPs climbed 1bps (1bps) to 3,53%, outperforming Bunds by -2bps.

10Y French OAT’s dropped 5bps (36bps) to 3,55%, underperforming Bunds by 2bps.

US High Yield (HY) Average Spread over Treasuries dropped -6bps (-25bps, Z-score -2,2) to 2,62%. US Investment Grade Average OAS dropped -3bps (-9bps) to 0,78%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -1bps (-10bps) to 0,53%.

Gold gained 1,2% (40,4%) while Silver rallied 2,1% (49,1%). Major Gold Mines (GDX) rallied 3,7% (113,4%).

Goldman Sachs Commodity Index dropped -0,4% (4,1%). WTI Crude was unchanged (-12,6%).

Overnight in Asia…

Ø S&P future -5 points; Hong Kong -1.1%; Nikkei+1.5%; China -0.2%

Ø Canada, the UK and Australia have formally recognized a Palestinian state, joining a growing global consensus and pushing ahead with a policy that has drawn criticism from US President Donald Trump. US officials have criticized the move and warned that it would incentivize Hamas to prolong the war with Israel.

Ø Porsche AG is hitting the brakes on electric vehicles, correcting an expensive strategy that’s depressed the luxury-car maker’s margins and is dragging down parent Volkswagen AG, Bloomberg wrote.

Ø Bernard Arnault has waded into an ongoing debate on how to restore France’s finances, calling an economist who has advocated a wealth tax a far-left activist whose ideology will destroy the country’s economy, Bloomberg reported. Zucman is “first and foremost a far-left activist,” Arnault told the newspaper. “He uses his pseudo-academic expertise — which itself is the subject of widespread debate — to serve his ideology (which aims to destroy the liberal economy, the only one that works for the good of all.)”

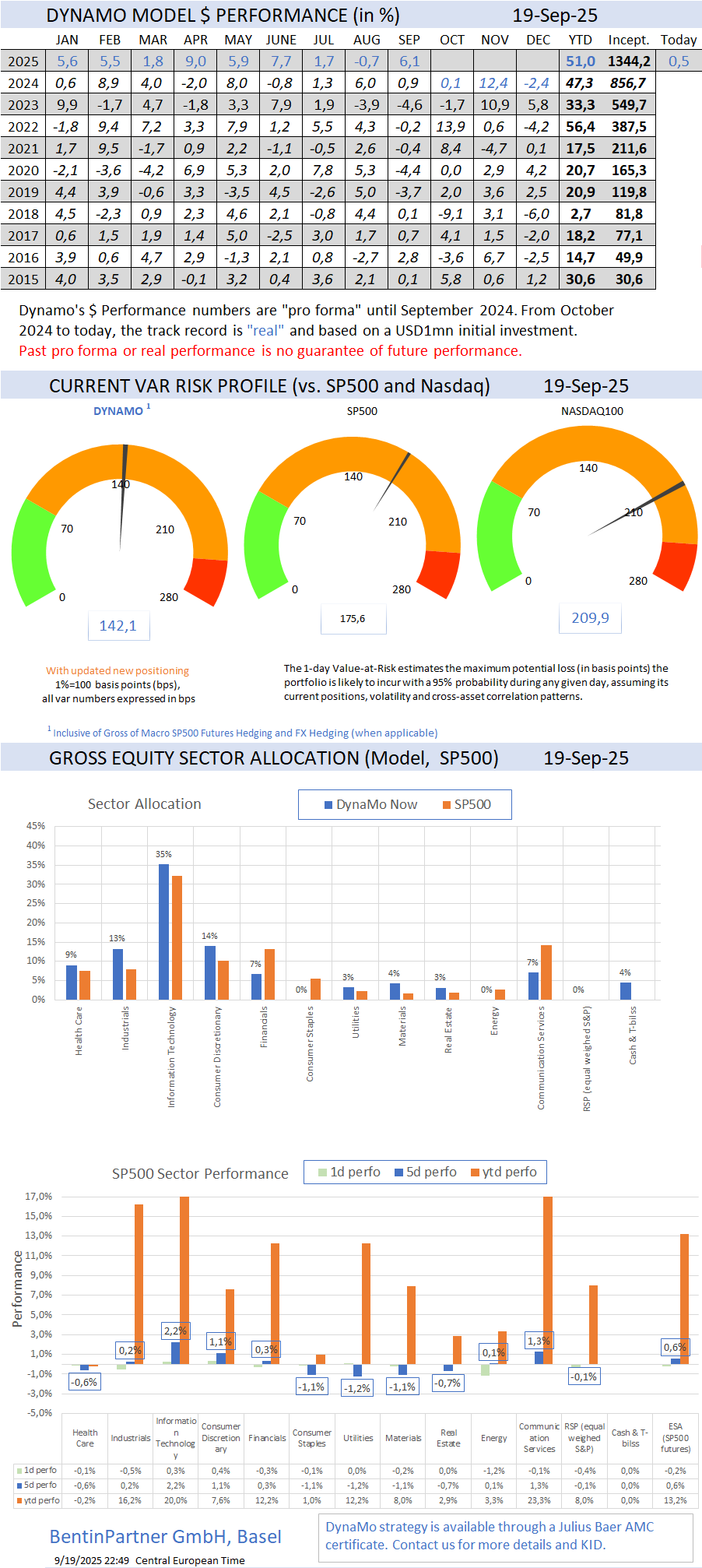

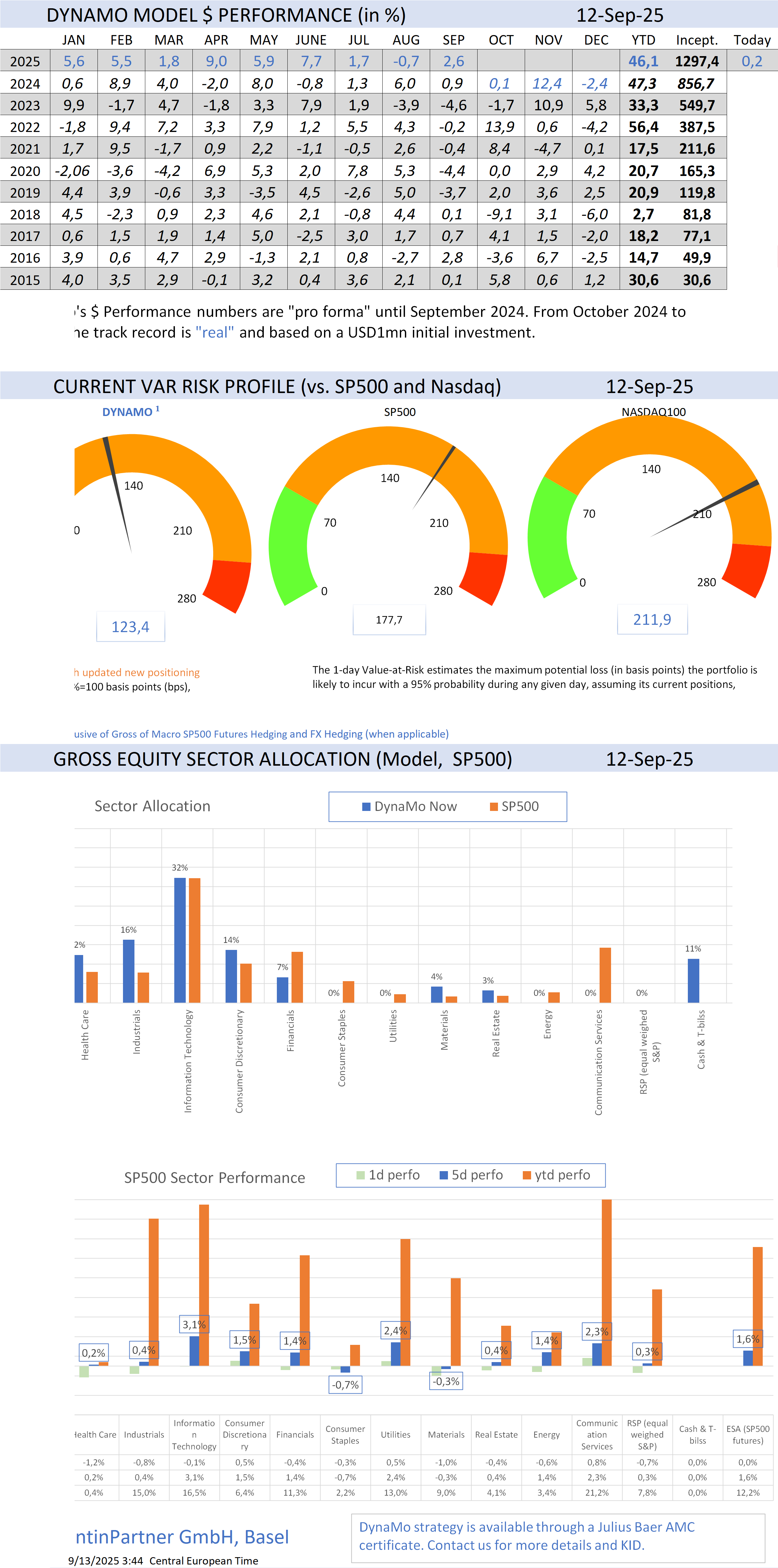

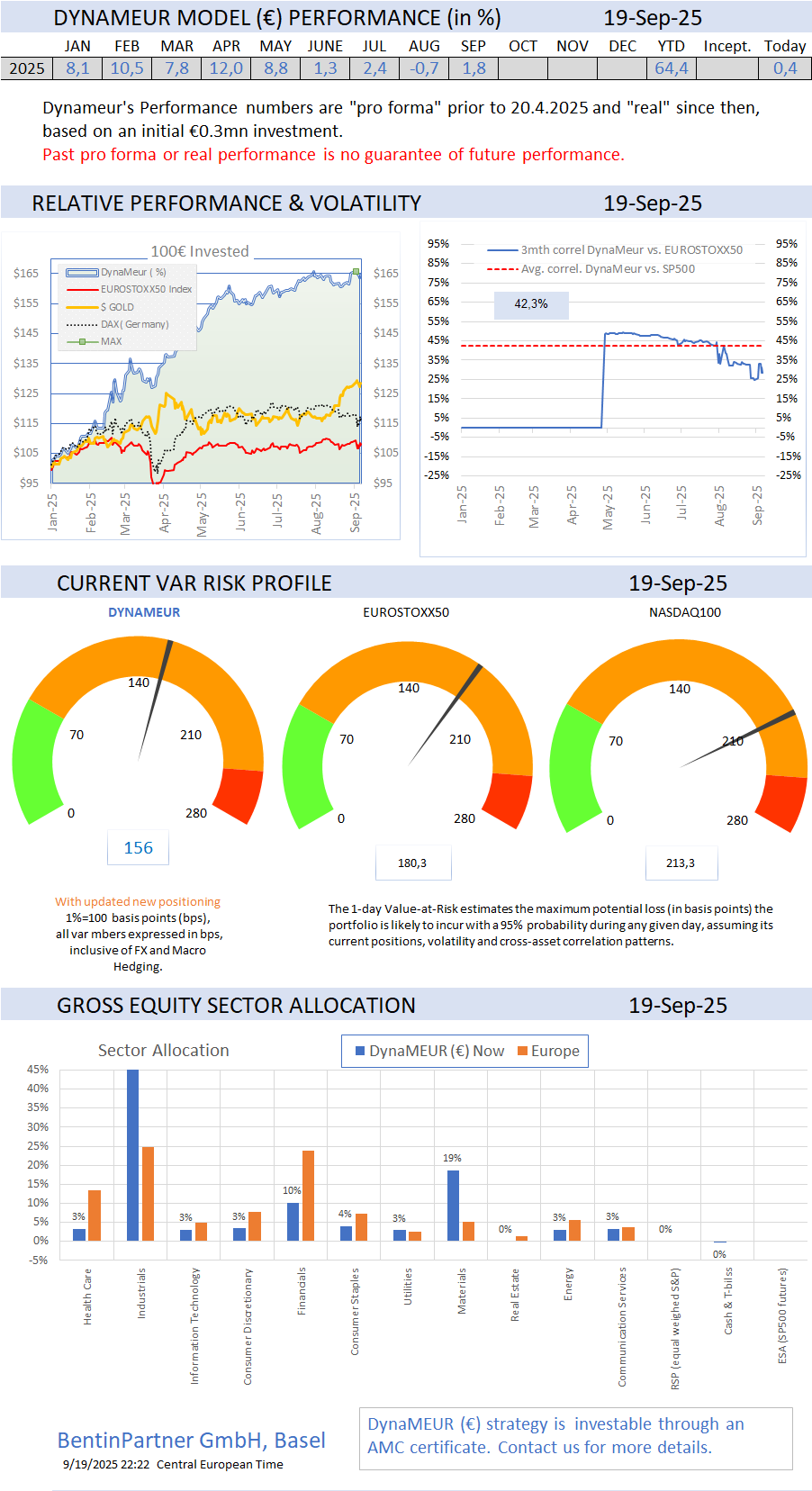

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments