Is Private Equity the New Subprime?

- Marc Bentin

- Oct 6, 2025

- 7 min read

Updated: Oct 11, 2025

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

US stocks continued their relentless rally last week albeit with a fly in the ointment as cracks continued to appear in the private credit boom amidst the collapse of First Brands, a US auto parts company that appears to have accumulated more than USD4bn in opaque debt by tapping all sorts of non-bank lenders.

This is occurring within a context where companies borrowed a record USD207bn in US investment grade in September at the same time as a wave of high yield debt issuance showed no sign of abating, also reaching a near record.

In this context, the share price of private credit firms underperformed meaningfully last week (KKR sank 15% over 7 days, Apollo -12% and Areas Management -17% over the same period).

Short seller Jim Chanos (known for exposing Enron accounting chicanery and benefitting from its ultimate collapse) in an interview to the FT said he was predicting more First Brands fiascos in private credit.

Chanos likened the near USD2trn private credit apparatus fueling Wall Street’s lending boom to the packaging of subprime mortgages that preceded the 2008 financial crisis due to the layers of people in between the source of the money and the use of the money. “There is going to be hell to pay when lending standards tighten, speculative flows reverse, deleveraging commences and credit becomes less freely available”, Chanos opined.

The bitter taste of First Brand was “peppered” by Monday’s announcement of the USD55bn take-private of video game maker Electronic Arts by a consortium including Saudi-Arabia sovereign Wealth Fund and Silver Lake Management, run by the son in law of D. Trump.

The real concern, might be around what happens next to the private credit boom and fast developing “vendor financing” scheme observed in the AI space which we have covered in our remarks from last Friday. Those concerns also led to the AI trade (and MAG7) to underperform last week.

Some were reassured by Goldman Sachs Most Short Index rallying another 9% last week while Biotech also squeezed nearly 8% but it could also be an indication of trouble in some Long /Short hedge fund strategies.

Also, Goldman noted a bizarre phenomenon that VIX has actually recently increased due to “call” buying (instead of the traditional “put” buying seeking protection), possibly indicative of a “peak momentum chasing” frenzy as calls in relation to puts option buying volumes reached an all-time high last Wednesday,

In any event, we raised our level of awareness last week to the possibility of a near term correction and added some equity hedges to our core long trend and momentum strategy in US and European markets (while reinforcing our exposure to precious metals).

On the economic side, the non-release of the US Non-Farm Payrolls report due to the government shutdown left investors to rely on private reports evidencing more job weakness ahead, contributing to make the outlook more uncertain.

While US bonds closed mostly unchanged, and Japanese bonds just 1bp higher, European bonds rallied last week by 5 to 8 bps across the board with Spain and Italy outperforming German bunds by 3 bps.

The Dollar Index declined -0.4% last week (-9.9% ytd) while Gold surged 3.4% to a fresh record (and more gains overnight). WTI dropped on supply and growth concerns while copper surged 7.1%

D. Trump said “a lot of good” could stem from the government shutdown, threatening to oust federal workers and eliminate programs that are favored by Democrats. Democrats said they were ready to battle, assuming the republicans have more to lose or to be blamed for, from a government shutdown.

The US President also faced more pushback last week as White House nominees to lead the BLS and CFTC were withdrawn after both ran into political resistance (E. J Antoni was deemed unqualified to lead an agency releasing key economic data).

Same on his trade policy …after South Korea said Washington’s terms of the trade deal were unrealistic. “We are not able to pay USD350bn investment pledge as part of a broader deal to lower US tariffs to 15% from 25%”, South Korea’s officials said.

Taiwan’s top trade representative also pushed back on the idea that the island will shift more of its chip production to the US.

The willingness of D. Trump to “negotiate” with China (without a hammer) is also demonstrating that the US is no more in a position to unilaterally weigh against China without fears of painful retribution (not least in the field of exports of rare earth minerals). According to people familiar wit the matter (and the WSJ), Xi Jinping is even now chasing his ultimate prize; a change in US policy that Beijing hopes could help pressing the US to formally state that the US formally opposes Taiwan’s independence.

Elsewhere in Europe, much time was spent on trying to defend a more aggressive approach towards Russia, the same one that failed to change the outcome of the war, except for jeopardizing and severely impairing Europe’s competitiveness and growth prospects at the exception of a small debt-financed growth boost from a “war machine” preparation.

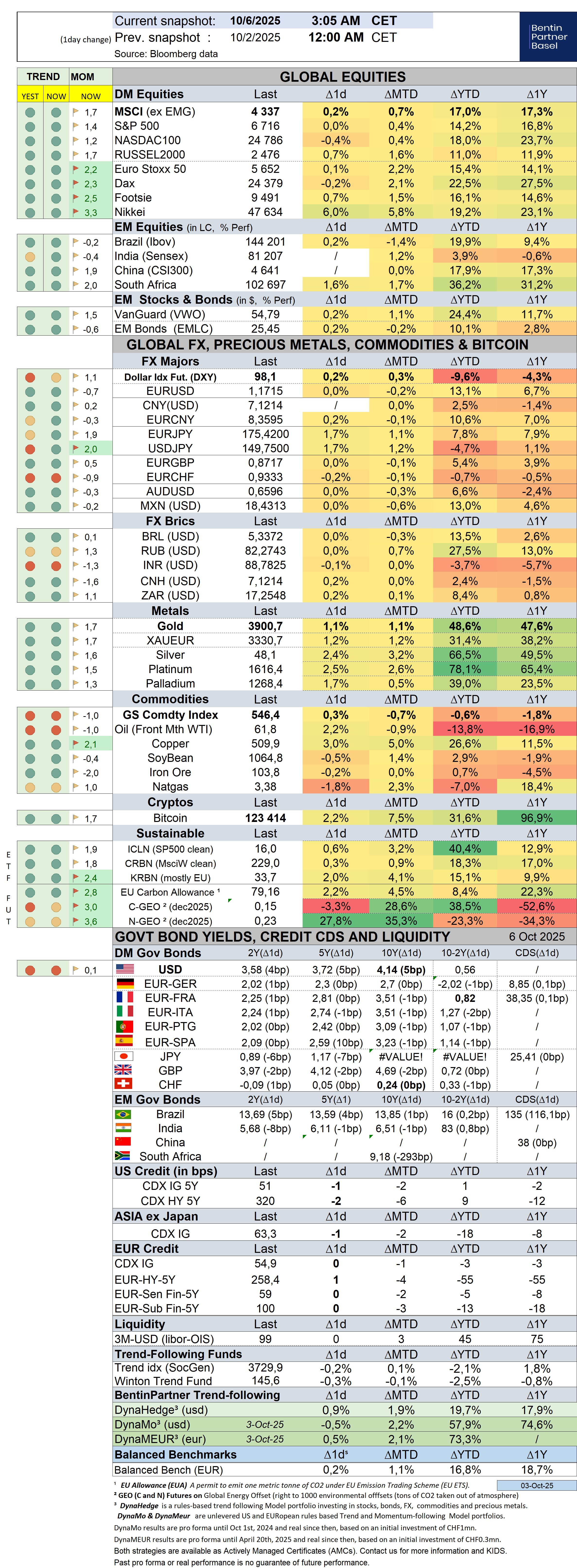

Over the past week, the S&P500 gained 1,1% (14,2% YTD) while the Nasdaq100 gained 1,2% (18,0% YTD). The US small cap index gained 1,9% (11,3% YTD). AAPL gained 1,0% (3,0%).

The Equally Weighed SP500 gained 1,4% (9,1% YTD, Z-score 2,2), outperforming the S&P500 by 0,3%. The median SP500 YTD return closed the week at 8,4%.

Cboe Volatility Index rallied 8,9% (-4,0% YTD) to 16,65.

The Eurostoxx50 rallied 2,8% (18,2%, Z-score 2,2), outperforming the S&P500 by 1,6%.

Diversified EM equities (VWO) rallied 2,3% (24,4%), outperforming the S&P500 by 1,2%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,4% (-6,6% ) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,2% (6,8% ).

10Y US Treasuries was unchanged (-43bps) to 4,14%. 10Y Bunds dropped -5bps (33bps) to 2,70%. 10Y Italian BTPs rallied -7bps (-1bps ) to 3,51%, outperforming Bunds by -2bps.

10Y French OAT's rallied -6bps (31bps) to 3,51%, outperforming Bunds by -1bps.

US High Yield (HY) Average Spread over Treasuries climbed 2bps (-19bps) to 2,68%. US Investment Grade Average OAS dropped -1bps (-9bps) to 0,78%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -1bps (-5bps) to 0,59%.

Gold gained 1,8% (48,7%) while Silver rallied 2,7% (66,7%). Major Gold Mines (GDX) rallied 3,2% (127,3%).

Goldman Sachs Commodity Index dropped -1,8% (4,8%). WTI Crude sold off by -2,6% (-13,8%).

Overnight in Asia…

Ø S&P future +20 points; Hong Kong -0.7%; Nikkei+4.5%; China +0.5%

Ø Japanese stocks stormed higher (with bonds unchanged) xausueafter a ruling-party vote positioned pro-stimulus lawmaker Sanae Takaichi (a proponent of easy fiscal and monetary policy) to become the next prime minister. The yen hit a record low against the euro and dropped back above 150 vs. USD.

Ø Other Asian shares climbed in sympathy, often to a record, while Gold powered towards 4’000 (now USD3’924) as investors bet on looser (international) monetary policy while the US government remained shut.

Ø Oil is recovering 1.5% from its -7% decline last week after OPEC said on Saturday it will raise its output by much less than expected (137k vs. 500k “feared”)

Ø French President Macron’s appointment of a broadly unchanged cabinet sparked an immediate backlash from opposition parties, undermining Prime Minister Sebastien Lecornu’s chances of surviving a make-or-break week in parliament, Bloomberg reported. Far-right leader Marine Le Pen said that Macron’s continuity was “pathetic” and leaves her National Rally party “speechless.” The Socialist Party repeated warnings that it would support a motion to topple Lecornu unless he marks a clear adjustment in direction, Bloomberg also reported.

Ø President D. Trump is pressing Israel and Hamas to seal a settlement to the two-year conflict. For Trump, a truce in the coming days and the freeing of the hostages could boost his campaign to win the Nobel Peace Prize, with the next winner being announced on Oct. 10.

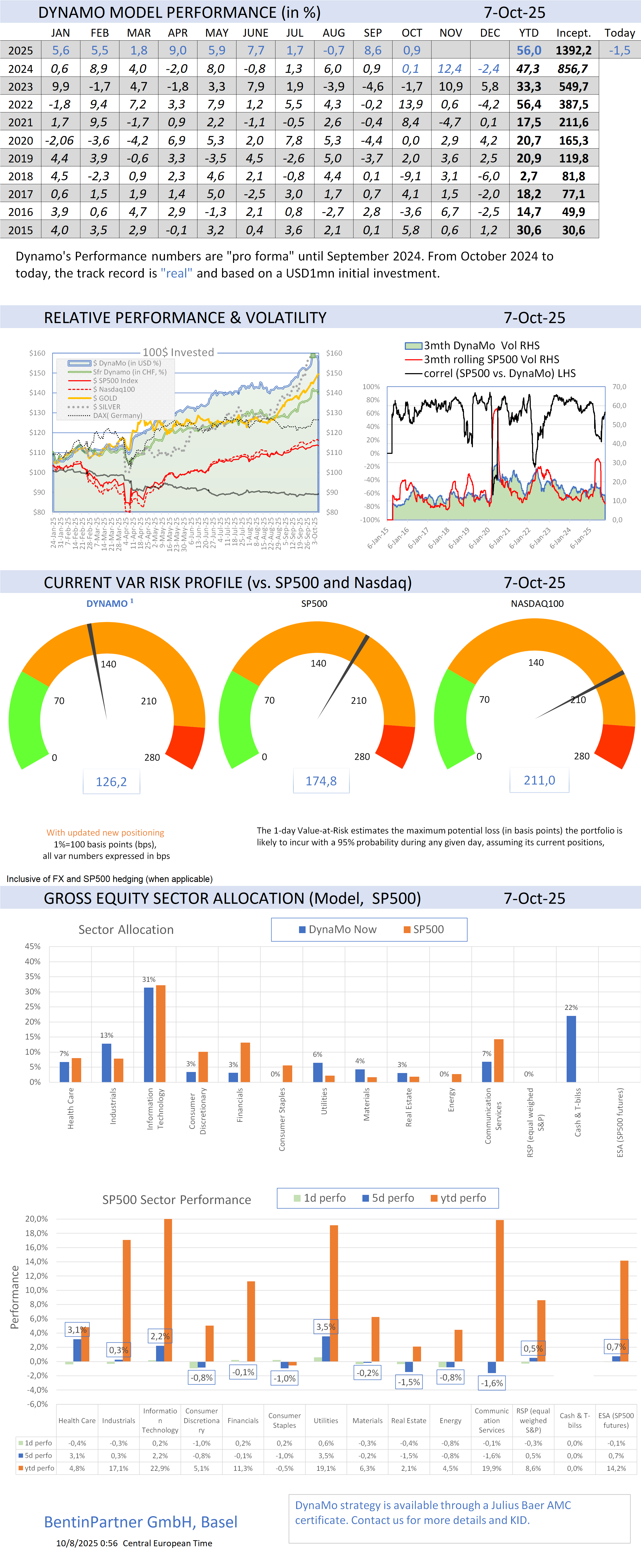

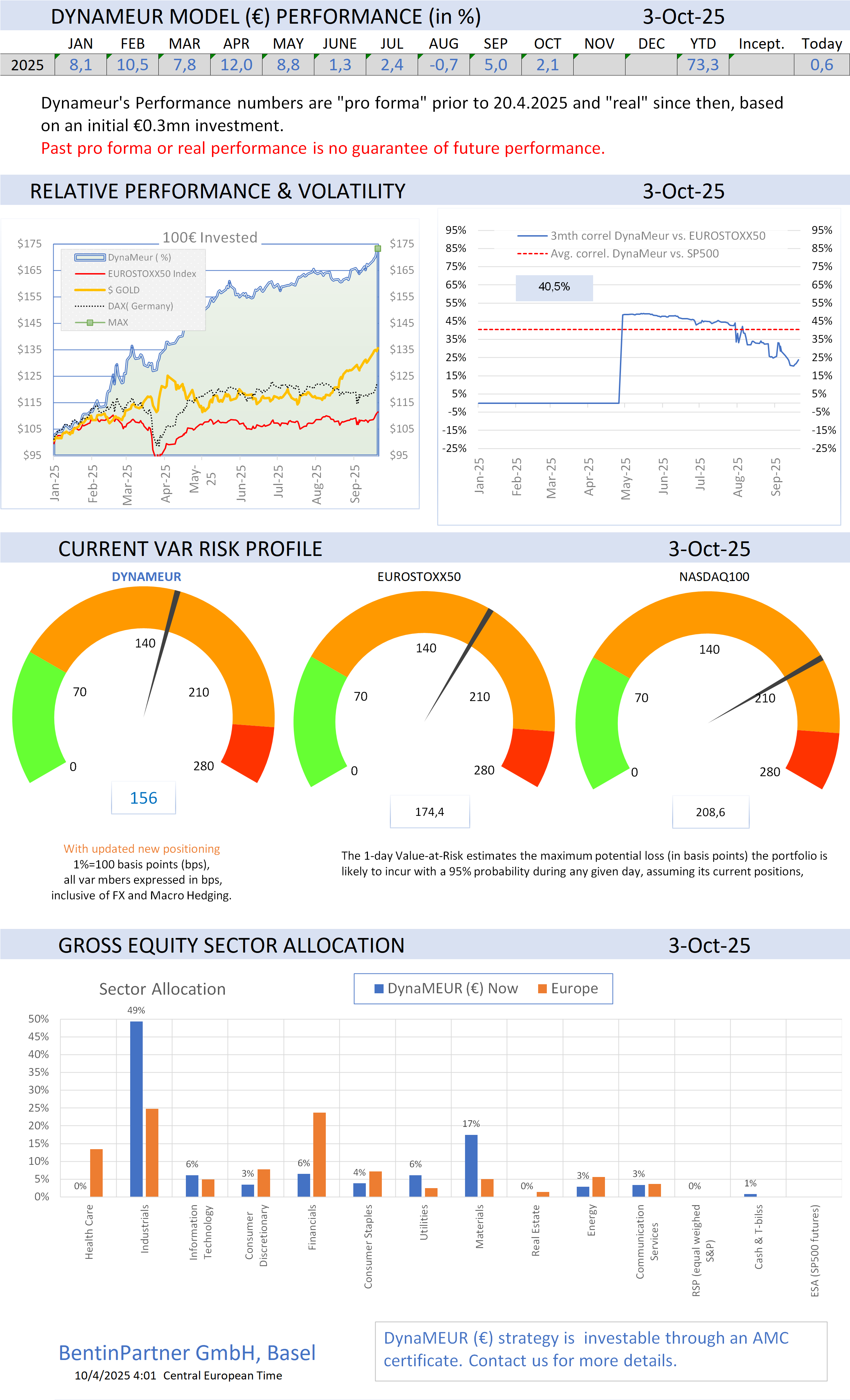

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments