US Stocks buoyed by Weak Economic Data...

- Marc Bentin

- Sep 15, 2025

- 9 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

US stocks posted another weekly gain, enthused by the perspective of the Federal Reserve cutting interest rates this week with more evidence that the US economy and in particular the job market are weakening, at the same time as inflationary pressures remained contained.

Wholesale prices surprisingly fell slightly in August (-0.1% for the month vs. +0.3% expected, following a downwardly revised 0.7% increase in July while the yoy headline PPI came at +2.6% (vs. +3.3% expected).

Later on Thursday, the August CPI report was less tame, gaining +0.4% for the month (vs. +0.3% expected and +0.2% for the previous reading) and +2.9% yoy (as expected). Notably, grocery prices climbed 0.6%, pushed higher by more expensive tomatoes, apples, and beef while the cost of air fares also rose 5.9% just from July to August.

This slight disappointment did not prevent stocks from rallying on that day, as it was accompanied by a 27k increase in US jobless claims to 263,000, the highest level in almost four years, confirming the weakening nature of the job market. Job market weakness was given additional confirmation with the BLS annual “benchmark” revision of the actual number of jobs creation observed over the past year, coming with 911k fewer jobs than originally reported in the year that ended in March 2025. The revision from the year prior was around 800k, providing ample evidence of the poor quality of the BLS job data.

J. Dimon said the Bureau of Labor Statistics’ record revision to US payrolls data was further proof that the US economy is battling a slowdown. ‘The economy is weakening,’ the JPMorgan… chief executive officer said… ‘Whether that is on the way to recession or just weakening, I don’t know.’”

Consumer data showed that serious credit-card and auto-loan delinquencies climbed to 2008-09 recession levels. Both the trade and fiscal deficits showed a deterioration as well. The sudden collapse of a Texas subprime car lender also sent shock waves, raising concern that pain in the multibillion-dollar market for bundled auto loans is starting to mount.

The income for the typical US household barely rose last year, matching its 2019 peak, the Census Bureau also said, illustrating the impact that the pandemic inflation spike had on Americans’ finances. The report also showed that the highest-earning households received healthy inflation-adjusted income increases, while middle- and lower-income households saw little gain, with housing affordability also declining which illustrated why many Americans have been dissatisfied with the economy since the pandemic, even as unemployment remained historically low.

In other words, the data pack from last week was less than stellar but it did not transpire from the buoyant stock (and credit) market and consumer spending as consumers (US consumer borrowing rose in July by most in three months, led by the strongest gain in credit-card balances so far this year), investors, businesses and the government are actually taking more debt to support the edifice , awaiting the Fed interest rate cut this Wednesday (on Sept. 17).

The median estimate from a Bloomberg survey of economists is for a 25 basis-point reduction but President D. Trump who has been putting pressure for months on Fed Chair J. Powell to cut rates, repeatedly encouraging him to resign, predicted a “big cut” this week. “I think you have a big cut,” Trump told reporters on Sunday on his way back to Washington.

Also, the US agricultural trade deficit widened further in July, highlighting the challenge facing President D. Trump as he vows to reverse the trend. Agricultural exports lagged imports by $4.97 billion in July, a gap 9% wider than a year earlier and the largest on record for the month.

With the inflation target still exceeded and the shift of power not yet totally in place, the market is still betting on 25bps…

More encouraging perhaps, after defending a too cautionary stance lately (and being blamed for it by D. Trump), Goldman’s CEO D. Solomon said the company will see its busiest week for IPOs since July 2021. “Rallying equity markets and bumper first-day performances from high growth tech-focused stocks have revived investor confidence in new issues, which had plummeted in April after sweeping US tariffs roiled global markets.”, he said.

In the US, the week was marked by a major political event after Charlie Kirk, a conservative activist who was shot and killed Sept. 10 at a college event in Utah. At a moment of extreme volatility in American politics, many MAGA leaders are now calling for retribution. The MAGA movement has long believed that it’s under siege, especially after the two assassination attempts against President Trump during the 2024 campaign.

The White House’s Stephen Miller said:

“Our nation is dealing with very serious issues of mental health and radicalization – particularly with young men. Social media is inciting hatred and violence. It has become so lucrative for some media and “influencers” to foment polarizing and emotionally charged views. When there’s a school shooting, the community doesn’t fracture and blame the other evil enemy side. We need a bipartisan group of leaders that will promote a much more constructive response to what, most regrettably, will be recurring acts of domestic terrorism. The course we’re on right now is spiraling toward some elements of civil war. we are going to do what it takes to dismantle the organizations and the entities that are fomenting riots, that are doxing, that are trying to inspire terrorism, that are committing acts of wanton violence. It has to stop.”

The ousting of Indonesia’s finance minister has rattled local markets, sending equities and the rupiah lower as investors worry about political pressure on fiscal and monetary policy. The move comes at a delicate time, with Indonesia rocked by protests against economic hardships and anger over proposed perks for politicians, something politicians across the world and in particular in Europe will be well inspired to look at carefully (the Government in Nepal fell for essentially the same reason) with an eye to take corrective measures (i.e. by sharing the burden of a more fiscal orthodoxy, not only among taxpayers but by reducing the government expenses, including perhaps by stopping to grant a Prime Minister’s pension for life to the 5 young (and less young) Prime Ministers of President E. Macron whose tenure each only lasted 1 year or less)…

French Prime Minister François Bayrou, was toppled in a no-confidence vote, with E. Macron now squarely in the line of public fire, with his popularity dropping to an all-time low.

E. Macron appointed in short order defense minister Sébastien Lecornu as his new prime minister, turning to one of his closest allies to try to quell political turmoil in the country…Lecornu, 39, is the only minister to have served continuously in all Macron’s governments since the president was first elected in 2017.

The market impact (on the OAT/Bund Spread) was limited as the confidence vote was deemed lost as early as it was called. On Friday, Fitch also downgraded Frances’ sovereign debt credit to A+ (from AA-), a decision that was also expected and which will only bear consequences (with forced institutional selling) after another of the top three rating agencies will have taken the same decision.

A measure of France’s borrowing costs exceeded Italy’s for the first time in the euro zone’s history, The trend toward convergence between France’s and Italy’s debt has long been in the making and for market veterans, “it’s a remarkable development given lower-rated Italy was for years the region’s poster-child for fiscal profligacy.”

Things did not quite settled down on the geopolitical side, with Russia and Belarus beginning a major joint military exercise on NATO's doorstep last Friday at a time of heightened tension with the Western alliance, two days after Poland shot down Russian drones that crossed into its airspace, an incident that German Chancellor Friedrich Merz said was a deliberate Kremlin provocation on NATO ‘This is a very serious threat to peace in Europe.’”, Mertz said emphatically.

UN Secretary-General A. Guterres decried the rise in global military spending to a record high, saying that priorities like child malnutrition, poverty and climate change were being neglected. ‘The evidence is clear: Excessive military spending does not guarantee peace,’ he said… ‘It often undermines it – fueling arms races, deepening mistrust, and diverting resources from the very foundations of stability.’”

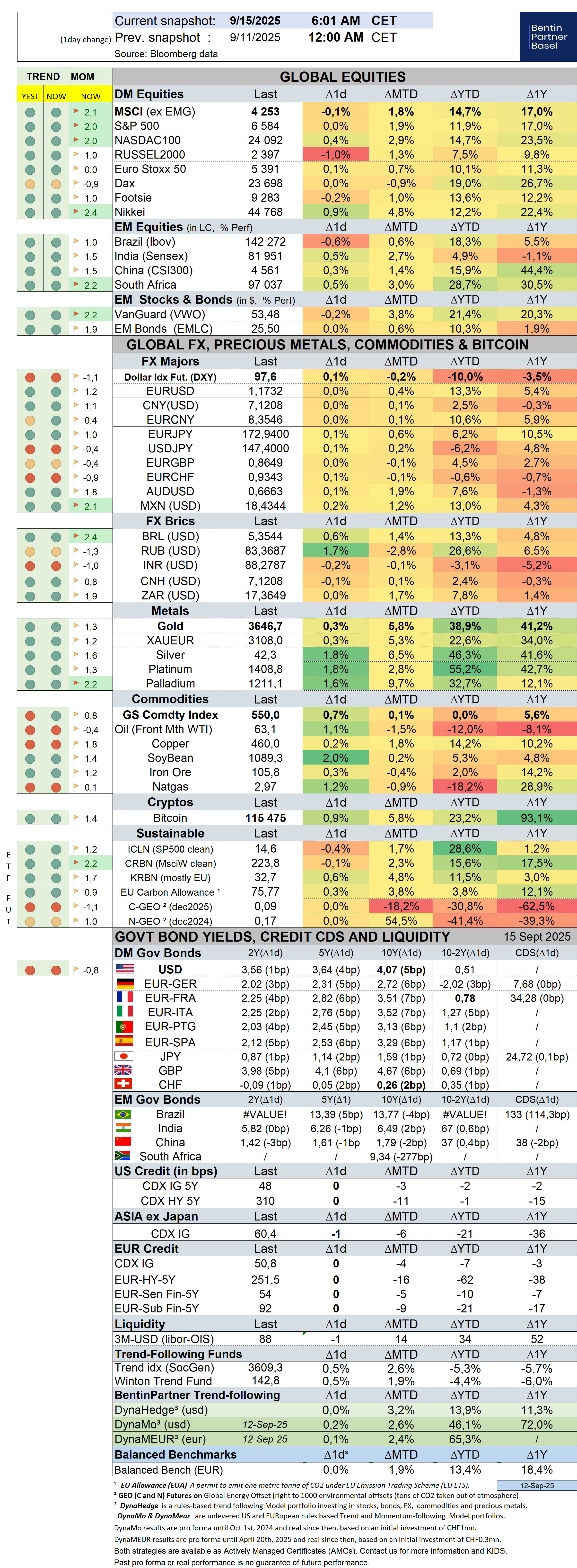

At the same time as equities improved further and broke records in the US (in local currency terms), bond markets posted mild losses while precious metals broke fresh records last week, led by a breakout in silver, as the dollar index dropped -0.2%, with potential further losses lying ahead.

The People’s Bank of China increased its gold holdings in August for a 10th month, in a continued push to diversify its reserves away from USD. China began this round of (“official”) gold purchases in November, accumulating a total of 1.22mn oz over the period.”

In addition to the Fed’s decision on Wednesday, the BOE and BoJ will also announce policy decisions later this week.

Over the past week, the S&P500 gained 1,6% (12,2% YTD, Z-score 2,4) while the Nasdaq100 gained 1,8% (14,8% YTD, Z-score 2,3). The US small cap index gained 0,2% (7,9% YTD). AAPL sold off by -2,3% (-6,5%).

The Equally Weighed SP500 gained 0,3% (7,8% YTD), underperforming the S&P500 by-1,3%. The median SP500 YTD return closed the week at 7,3%.

Cboe Volatility Index sold off by -2,8% (-14,9% YTD) to 14,76.

The Eurostoxx50 gained 1,4% (12,5%), underperforming the S&P500 by-0,2%.

Diversified EM equities (VWO) rallied 2,9% (21,4%, Z-score 2,7), outperforming the S&P500 by 1,3%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped 0,0% (-6,9%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,5% (6,8%).

10Y US Treasuries rallied -1bps (-50bps) to 4,06%. 10Y Bunds climbed 5bps (35bps) to 2,72%. 10Y Italian BTPs climbed 2bps (0bps) to 3,52%, outperforming Bunds by -3bps.

10Y French OAT's underperformed rising 6bps (31bps) to 3,51%, underperforming Bunds by 1bps.

US High Yield (HY) Average Spread over Treasuries dropped -2bps (-17bps) to 2,70%. US Investment Grade Average OAS dropped -3bps (-7bps) to 0,80%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -4bps (-10bps) to 0,54%.

Gold gained 1,6% (38,8%) while Silver rallied 2,9% (46,0%). Major Gold Mines (GDX) rallied 5,1% (105,7%).

Goldman Sachs Commodity Index gained 1,5% (4,5%). WTI Crude gained 1,3% (-12,6%).

Overnight in Asia…

Ø S&P future +5 points; Hong Kong +0.4%; Nikkei+0.9%; China +0.9%

Ø Asian shares followed US stocks higher.

Ø China’s retail sales rose 3.4% YoY while industrial production rose 5.2% YoY.

Ø HKD extended its gains, hitting a four-month high as supply of the currency continued to tighten toward the end of the quarter.

Ø Germany’s far-right party tripled support in municipal elections in the industrial state of North Rhine-Westphalia, intensifying pressure on Chancellor Friedrich Merz’s government to revive growth and push through reforms. In the country’s most-populous state, the anti-immigration Alternative for Germany party, or AfD, increased its share of the vote by 9.4 % to 14.5% and narrowly missed winning the mayor’s race in the industrial city of Gelsenkirchen, according to preliminary results.

Ø US and Chinese representatives discussed TikTok, trade and the economy during high-level talks in Madrid, a senior Treasury official said. The talks will continue today, laying the groundwork for a potential meeting between D. Trump and Xi Jinping as soon as October.

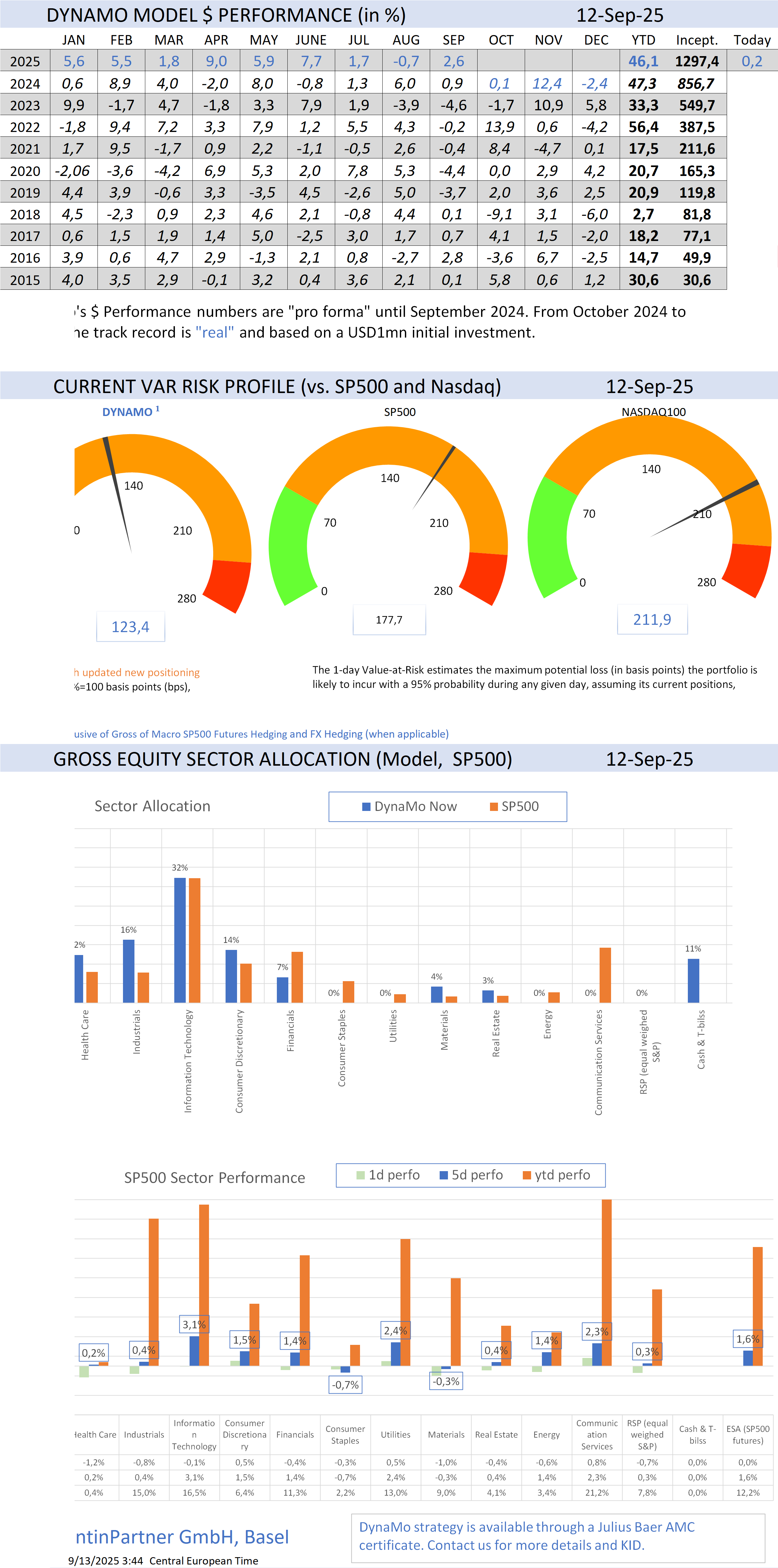

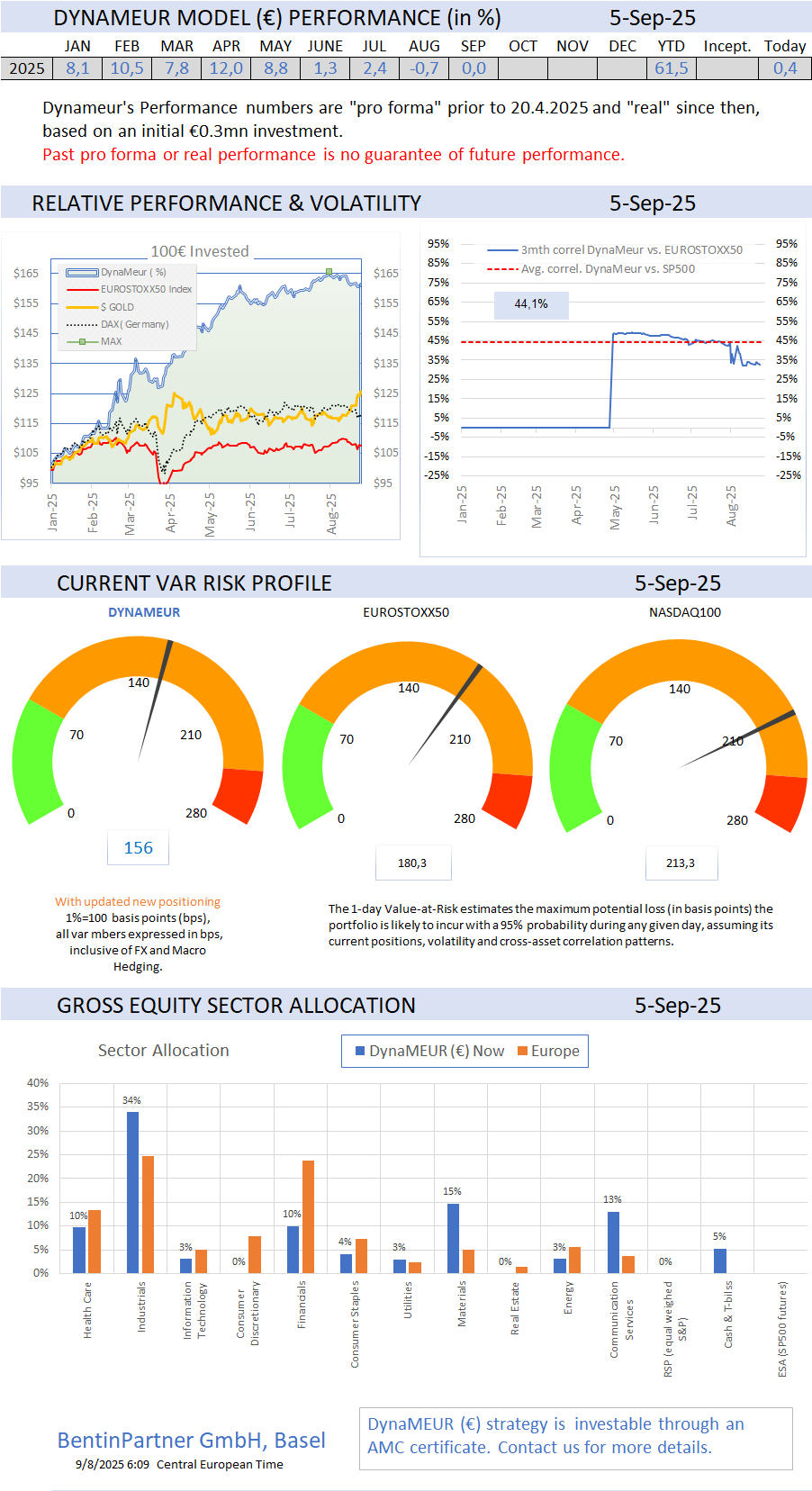

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments