Fighting Another Lizz Truss Moment...

- Marc Bentin

- Jan 26

- 9 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

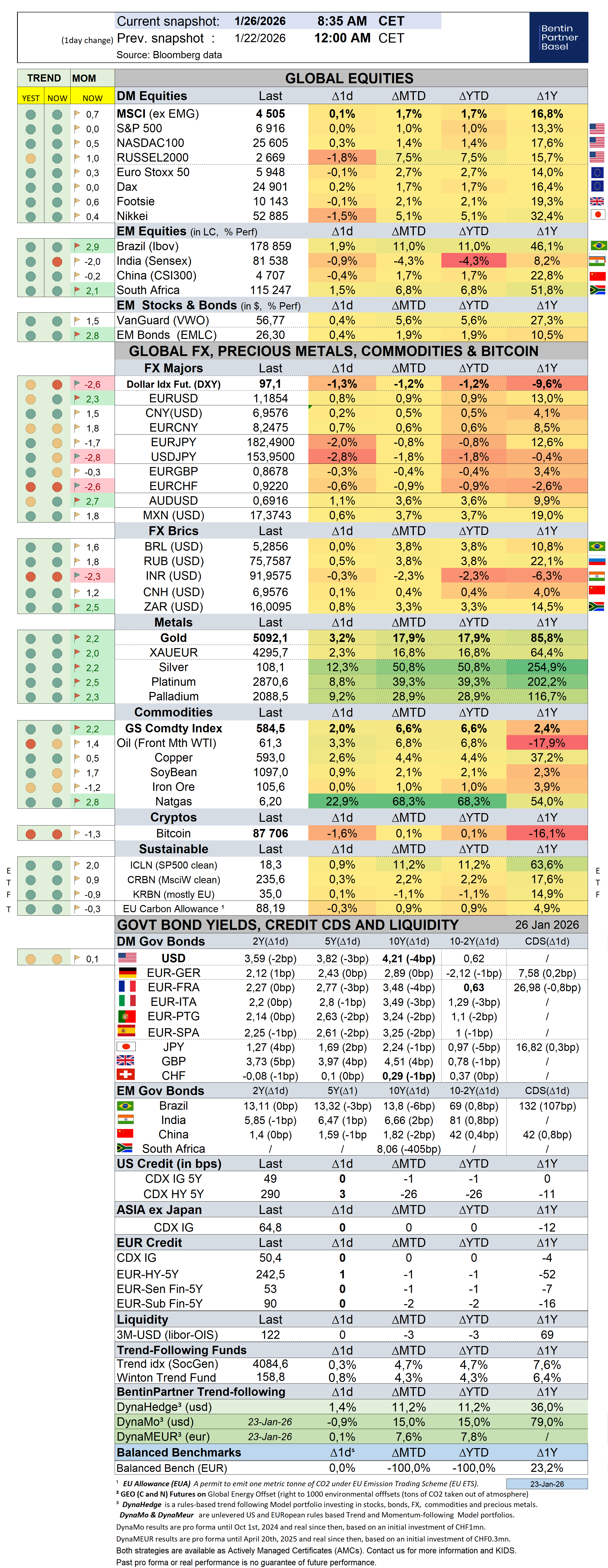

Although the equity markets’ correction of the past two weeks remained mild so far, it still seemingly took investors off guard who remained the most bullish since July 2021 with protection holding at an eight-year low, and with cash levels at a record low, according to BoA survey. These findings also pushed BofA’s Bull and Bear indicator into ‘hyper-bull’.

As one of the major developments so far this year, small caps further outperformed last week with MAG7 morphing into MAG5 and perhaps even Fab4 due to a more cautious view of the AI (circular) spending boom. Only Alphabet and Nvidia outperformed the SP500 last year and so far this year, five of the Mag 7 are faring worse than broad indices.

Last week’s major event was Japan‘s debt market suddenly boiling over last Tuesday, sending 30Y yields 27bps higher to all-time highs of 3.85% (before ebbing back to 3.6% towards the end of the week) as Prime Minister S. Takaichi’s plans to cut taxes and boost spending raised doubts about Japan’s financial health, triggering what some called a Japanese Liz Truss moment (Japan carries a 250% debt/GDP ratio with almost half of bonds held by the BoJ).

This triggered a broader bond market malaise which sent Greek yields also surging 18 bps to 3.52% and German 10Y yields 7 bps higher on the week to 2.91%, 5 bps away from the highest yield level since July 2011.

This caught the attention of K. Griffith (Citadel) at the Davos forum last week who delivered some important cautionary remarks;

“I actually think there’s an explicit warning – that if your fiscal house is not in order, the bond vigilantes can come out and extract their price. And what’s particularly troubling is that if you look at what happened in Japan – when bonds and stocks move together in prices then bonds are no longer a hedge for your equity portfolio. And they lose a substantial part of what makes them so special in constructing a portfolio. If U.S. Treasuries are viewed as being at risk - because the United States is not seen as being creditworthy – then bonds and stocks will move together in price and that will result in bonds having a much-higher demanded yield in the marketplace. So, mortgage interest rates will be higher. The cost for us to finance our deficits will be higher. I think that what happened in Japan is a very important message to the House and to the Senate: you need to get our fiscal house in order.”

On that topic, Citigroup also warned that “Risk parity” funds, allocating capital across multiple asset classes from stocks to bonds and commodities with equal volatility, may need to sell as much as one third of their current exposure, increasing volatility and potentially triggering up to $130 billion of bond selling in the US alone.

A Wednesday Fortune headline read: “Ray Dalio Warns that the Monetary Order is Breaking Down, Leaving us with a Terrible Choice: ‘Do Your Print Money or Let a Debt Crisis Happen.” Trapped.

Linking the dire debt and geopolitical context, R. Dalio opined;

‘Let’s not be naive and say, ‘Oh, we’re breaking the rule-based system,’’ ‘It’s gone’.” The billionaire founder of Bridgewater, the largest hedge fund also opined that as a student of financial history, he pays close attention to the economic cycles of the last 500 years and sees cycles repeat themselves over time. ‘And what I learned through that exercise is the same thing happens over and over again… And it’s like a movie for me. It’s like watching the same movie happen’.

Interestingly, Polymarket betting odds have turned upside down in J. Powell’s succession race with Rick Rieder (BackRock senior managing director) now at 53% versus Kevin Warsh at 28%. The explanation perhaps is that Warsh is more independent and favors a smaller balance sheet as opposed to the new contender working for Blackrock…

In between these two warnings, ECB President C. Lagarde tongue slipped (or showed foresightedness) when she said in a sentence…as long as central banks exist… showing her troubles with D. Trump threatening Central Banks’ independence and trying to place of puppet at the helm of the most important central bank of the world and as Central Banks face the extraordinary challenge (and danger in my view) of stable coins which are doing no less than trying to privatize the issuance of money with all the associated risks …

The ECB tries to address those challenges with its CBDC…but I am not sure these will be serious contenders as neither I nor anybody else, should like the fact that they could be used to police the use of money and ultimately facilitate a Chinese-like “social scoring” system at a time when Europe is already hitting a serious brake on individual freedoms.

That said, stable coins remain first and foremost political tools to place in private hands the seignorage benefits of money and in the case of the US to the benefit of a happy few, including inter alia, the siblings of D. Trump.

The biggest benefit for sponsors of stable coins (who back them with US tbills and other short-term securities) is to keep the collateral interest for them because the law (trying to protect banks’ interest and unfair competition) forbids so far (Genius Act) the sharing/distribution of any of the collateral yield … Some large foreign “public” projects are already funded with those stable coins which can be diverted, in my view, as an elegant and modern from of corruption (say country X agreed to fund a project paying it with a given stable coin, this creates fresh stable coins that grants seignorage rights going straight in the pockets of the given stable coin sponsors…. who are…).

The growth of stable coins will go exponential if left unchecked by a complicit regulation.

True, stable coins have some legitimate use in less favored nations (for ex Africa) where inflation is so high that it can hedge their users’ savings in non-interest-bearing dollar stable coins. Another benefit of USD stable coins (such as UST) is to force the purchase of US treasuries (as collateral to the stable coins) in countries under sanction that would not otherwise be inclined or even authorized to use the dollar anymore for trading and saving.

The rest, including the speed of settlement, could be just powder in the eyes of those seeking validation and compromising regulatory oversight, in my view.

On the economic side, powered by strong consumer spending, the US Atlanta Fed GDPNow Forecast was up to 5.37%, from a Q3’s slightly upwardly revised 4.4% GDP growth, implying that overheating risks remained., the U.S. economy grew at the fastest pace in two years from July through September.

Mortgage refinancing also jumped for the second straight week with applications to refinance a home loan rising 20% compared with the previous week and applications 183% higher than the same week one year ago.

US jobless claims inched up last week by 1,000 to 200,000 but US layoffs remained historically low despite signs of a softening labor market.

The Fed’s preferred inflation gauge also ticked up in November in the latest sign that prices remain stubbornly elevated, while consumers spent at a healthy pace. Consumer prices rose at an annual pace of 2.8% in November from a year earlier, up from a 2.7% in October.

The dollar traded sharply lower across the board last week, considering recent past volatility patterns with the U.S. Dollar Index dropping 1.8% to 97.599 (down 0.9% y-t-d).

Silver closed the week at USD103, offering little resistance to the USD100 barrier, with Gold flirting with USD5,000. Gold jumped 15.5% so far this month, adding to 2025’s 64% gain while silver surged 44%, following last year’s 148% gain. At the same time, Bitcoin shed 6.2% to USD89,300 (up 1.9%).

Commodities were also on fire with the Bloomberg Commodities Index jumping 5.3% (+ 9.0% YTD). Natural Gas spiked 71.9% higher to $5.333 (+45% YTD).

On the geopolitical scene, EU leaders welcomed D. Trump’s decision to drop his threat of tariffs against European allies and to promise not to use force to seize Greenland.

At the same time, D. Trump vowed ‘big retaliation’ if European countries sell US assets in response to his tariff threats related to Greenland, adding pressure on them to stick with an emerging deal over the future of the island. ‘If they do, they do. But you know, if that would happen, there would be a big retaliation on our part,’ Trump said… ‘And we have all the cards’.” I am not so sure…

ECB President C. Lagarde during a panel discussion at Davos attended by L. Fink (Blackrock) and K. Griffin (Citadel), also warned that a big societal challenge now lies ahead with wealth disparity. On that subject, Bloomberg published an article on the subject last week stating that the share of total wealth held by the richest Americans is now at the highest level since World War II. The top 1% of households controlled 31.7% or 55trillions and nearly as much as the bottom 90% combined.

Over the past week, the S&P500 gained 1,6% (1,8% YTD) while the Nasdaq100 rallied 2,2% (2,0% YTD). The US small cap index rallied 4,6% (5,7% YTD, Z-score 2,1). AAPL shed -4,3% (-4,6%).

The Equally Weighed SP500 rallied 2,5% (3,2% YTD, Z-score 2,3), outperforming the S&P500 by 0,9%. The median SP500 YTD return closed the week at 2,4%.

Cboe Volatility Index dropped -0,1% (-3,1% YTD) to 14,49.

The Eurostoxx50 rallied 2,5% (3,4%, Z-score 2,2), outperforming the S&P500 by 0,9%.

Diversified EM equities (VWO) gained 0,9% (3,1%), underperforming the S&P500 by -0,7%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 0,8% (1,1% , Z-score 2,5) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,1% (-0,1%).

10Y US Treasuries rallied -3bps (0bps ) to 4,17%. 10Y Bunds dropped -4bps (1bps) to 2,86%. 10Y Italian BTPs rallied -12bps (-6bps) to 3,50%, outperforming Bunds by -8bps.

10Y French OAT's rallied -9bps (-4bps) to 3,52%, outperforming Bunds by -5bps.

US High Yield (HY) Average Spread over Treasuries dropped -11bps (-9bps ) to 2,57%. US Investment Grade Average OAS dropped -1bps (-1bps) to 0,83%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 0bps (-1bps) to 0,53%.

Gold rallied 2,6% (5,7%) while Silver rallied 8,2% (15,7%). Major Gold Mines (GDX) rallied 8,0% (7,9%).

Goldman Sachs Commodity Index rallied 2,3% (2,4%). WTI Crude gained 1,1% (2,6%).

Overnight in Asia…

Ø S&P future -32 points; Hong Kong +0.2%; Nikkei+1.6%

Ø US stocks dropped and Gold jumped to a record high on geopolitical concerns (and deadly troubles in Iran) and as the US Justice Department threatened the Federal Reserve with a criminal indictment, reviving concerns over its independence. D. Trump also reiterated threats to take Greenland while questioning the value of the NATO alliance, just over a week after seizing Venezuelan leader Nicolas Maduro. Silver also jumped 4%.

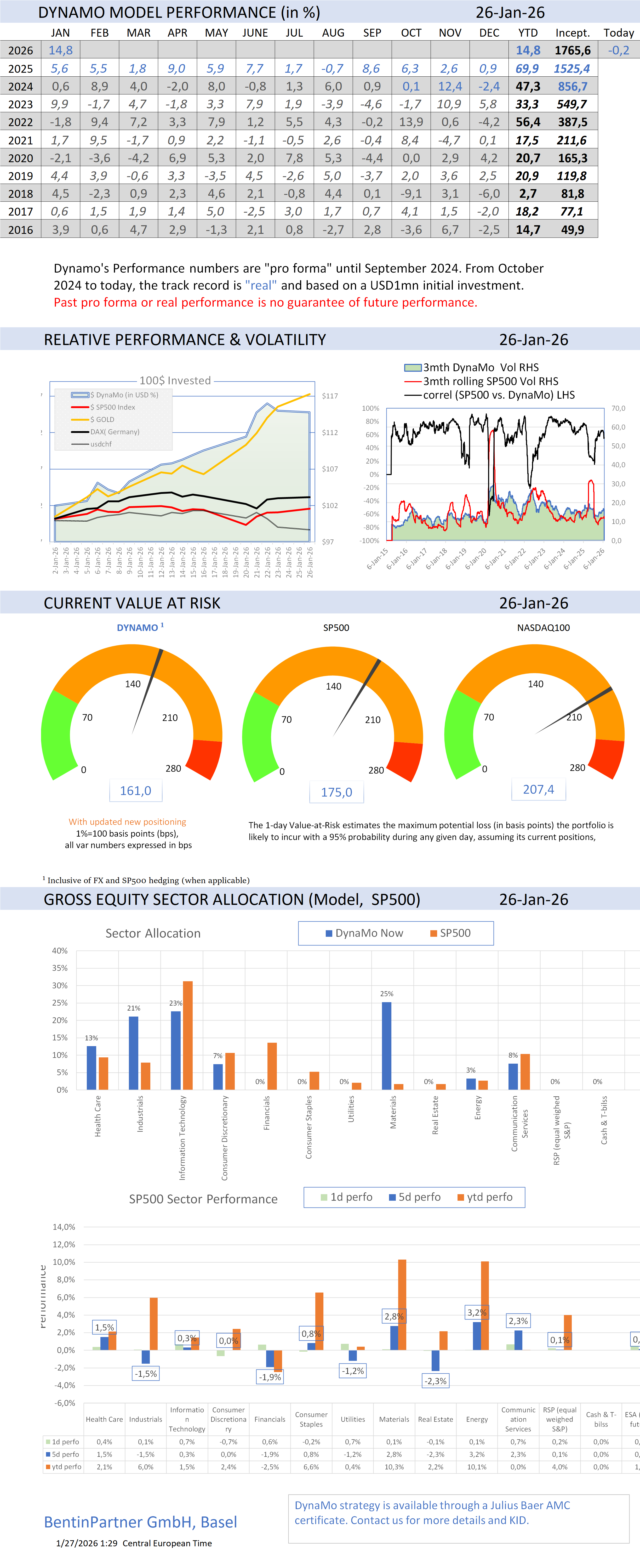

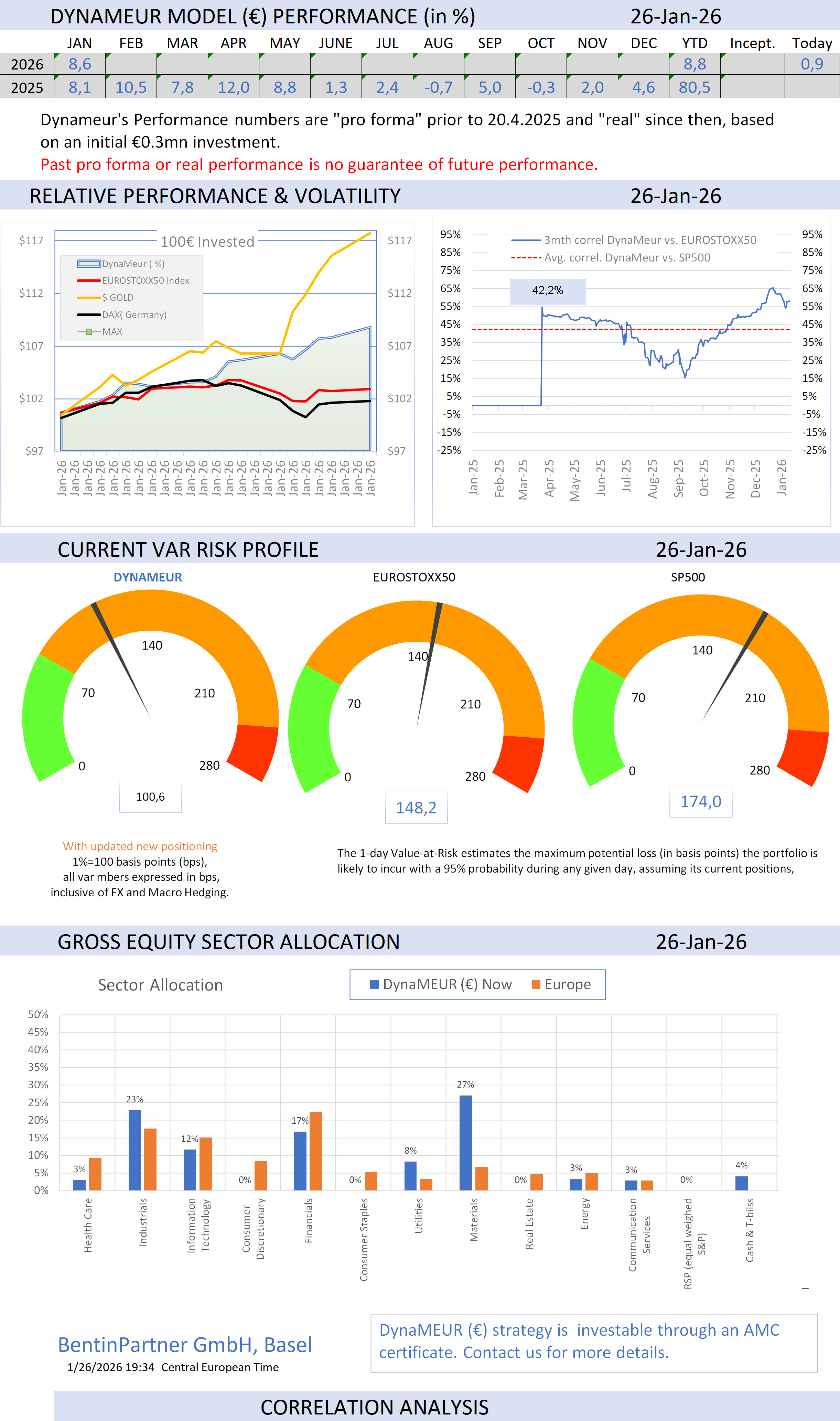

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments