Warshed Out...

- Marc Bentin

- Feb 2

- 5 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Global markets were shaken, seemingly by the choice of K. Warsh as the new Fed Chair to succeed J. Powell seen as more “hawkish” than the other candidates. While K. Warsh has been more critical of QE, having notably pushed back in 2010 against Bernanke’s move to restart QE, he is by no means a dove…It would appear that he fitted the bill to fuel a narrative seeking to justify a deleveraging that was brought to extremes in several markets sector (including precious metals) and looking for an excuse to start to unwind. S: Druckenmiller who worked with K. Warsh, said no less overnight arguing that seeing K. Warsh as someone who is always hawkish is simply wrong. It would not be a stretch of the imagination to believe that he managed to convince D. Trump to choose him for the top Fed job by being more dovish than others and even supportive of QE if/when the time comes.

One thing K. Warsh is supportive of, is fiscal “prudency”. After voting with B. Bernanke on adopting QE2, the following week, he published an op-ed piece for the Wall Street Journal where he stated inter alia;

“Fiscal authorities should resist the temptation to increase government expenditures continually in order to compensate for shortfalls of private consumption and investment.”

“Pro-growth policies include reform of the tax code to make it simpler, more transparent and more conducive to long-term investment. These policies also include real regulatory reform so that firms—financial and otherwise—know the rules, and then succeed or fail.”

All it says is that he is capable to talk hawkish (to please the bond vigilantes) and act dovish (to please everybody else) including D. Trump who had already considered appointing him the last time… (but Trump said he had not tried hard enough …which he must have done now, I suppose).

Still, excessive leverage leads to leverage unwind and with excesses present in every corner of financial markets, starting with the AI spending boom, massive related debt issuance and even precious metals to a certain extent, some form of correction should come as no surprise. In any case, deleveraging was everywhere to be seen on Friday and this morning including in precious metals and cryptos.

The dollar rebounded on Wednesday after S. Bessent reminded what the US Treasury always says …that “the US pursues a strong dollar policy” (even when everything is pointing in the other direction).

We still prefer JPY and CNY here and now (and probably the US Treasury as well).

Bonds closed slightly stronger last week, albeit with slightly higher HY spreads.

In Geopolitics, things did not turn for the better with the approaching US armada in the Middle East still conveying elevated risks of an intervention against Iran. US President Trump also authorized his administration to slap tariffs on goods from countries that provide oil to Cuba, tightening the squeeze on the communist-run government he wants to see replaced.

The US might one day run short of countries to be sanctioned and that is when its currency might ultimately crater… The reality is that fewer and fewer countries will need USD reserves as trade will increasingly take place in domestic currencies and increasingly in CNY in the new world order.

Internal US politics were focused on the ICE developments and the further Epstein files revelation which are surprising no one but compromising those who see their crimes impossible to cover up.

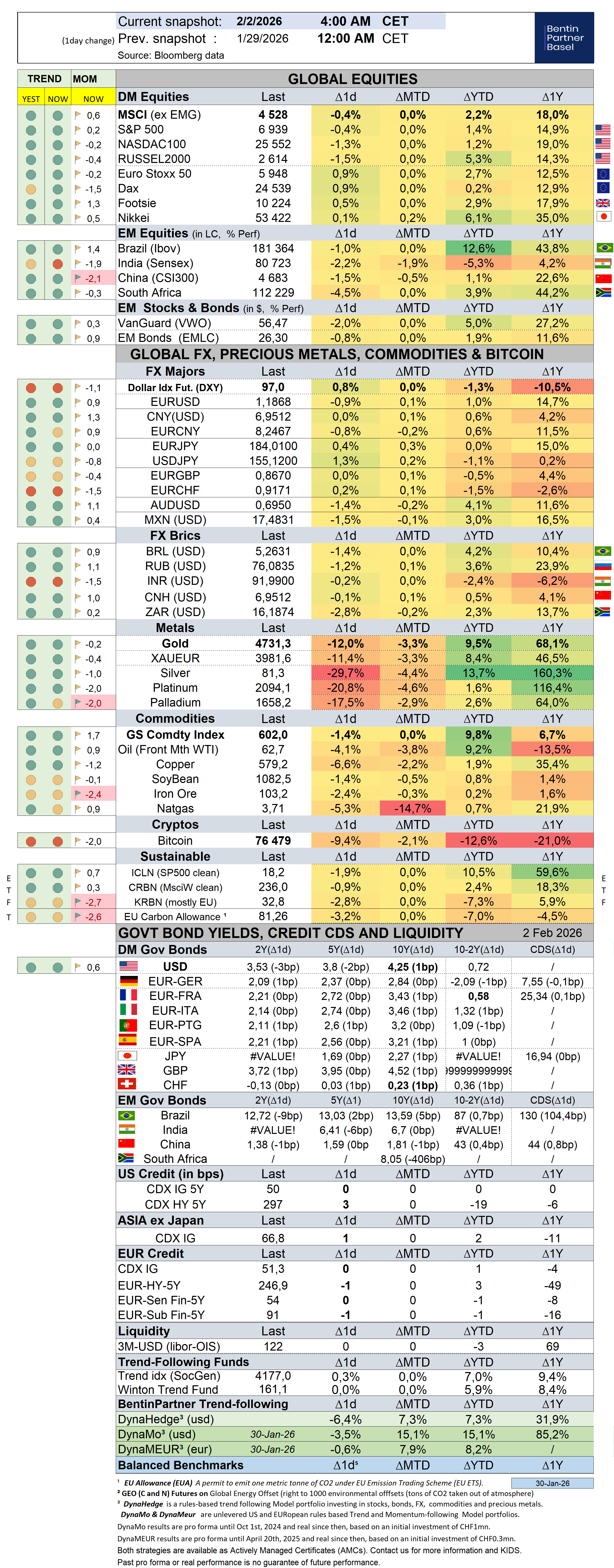

Over the past week, the S&P500 gained 0,4% (1,5% YTD) while the Nasdaq100 dropped -0,1% (1,2% YTD). The US small cap index dropped -1,9% (5,5% YTD). AAPL rallied 4,6% (-4,6%).

The Equally Weighed SP500 dropped -0,3% (3,4% YTD), underperforming the S&P500 by-0,7%. The median SP500 YTD return closed the week at 3,1%.

Cboe Volatility Index rallied 8,4% (16,7% YTD) to 17,44.

The Eurostoxx50 was unchanged (2,6%), underperforming the S&P500 by-0,4%.

Diversified EM equities (VWO) dropped -0,5% (5,0%), underperforming the S&P500 by-0,9%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,2% (-0,7%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,0% (0,6% ).

10Y US Treasuries dropped 2bps (7bps) to 4,23%. 10Y Bunds dropped -6bps (-1bps) to 2,84%. 10Y Italian BTPs rallied -6bps (-10bps) to 3,46%, matching Bunds.

10Y French OAT's rallied -7bps (-14bps) to 3,43%, outperforming Bunds by -1bps.

US High Yield (HY) Average Spread over Treasuries climbed 9bps (-1bps ) to 2,65%. US Investment Grade Average OAS climbed 2bps (-4bps) to 0,80%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 1bps (-1bps) to 0,54%.

Gold sold off by -7,2% (7,6%) while Silver sold off by -26,1% (7,0%). Major Gold Mines (GDX) sold off by -12,0% (9,8%).

Goldman Sachs Commodity Index gained 1,0% (9,3%). WTI Crude rallied 3,0% (8,7%).

Overnight in Asia…

Ø S&P future -78 points; Hong Kong -2.6%; Nikkei -1%%; China -1.4%

Ø A sea of red hit futures overnight ranging from silver dropping another -10%, Gold falling in sympathy by -5% and the SP500 and Nasdaq dropping -1.5%. Bitcoin participated to the purge continuing Friday’s selloff to 75’500.

Ø Oracle reported that it plans to raise $45bn to $50bn this year through a combination of debt and equity sales to build additional cloud infrastructure capacity

Ø The BoE is expected to keep interest rates on hold at 3.75% this week as policymakers weigh contradictory signs that the economy is both strengthening and losing jobs with unemployment at a near five-year high.

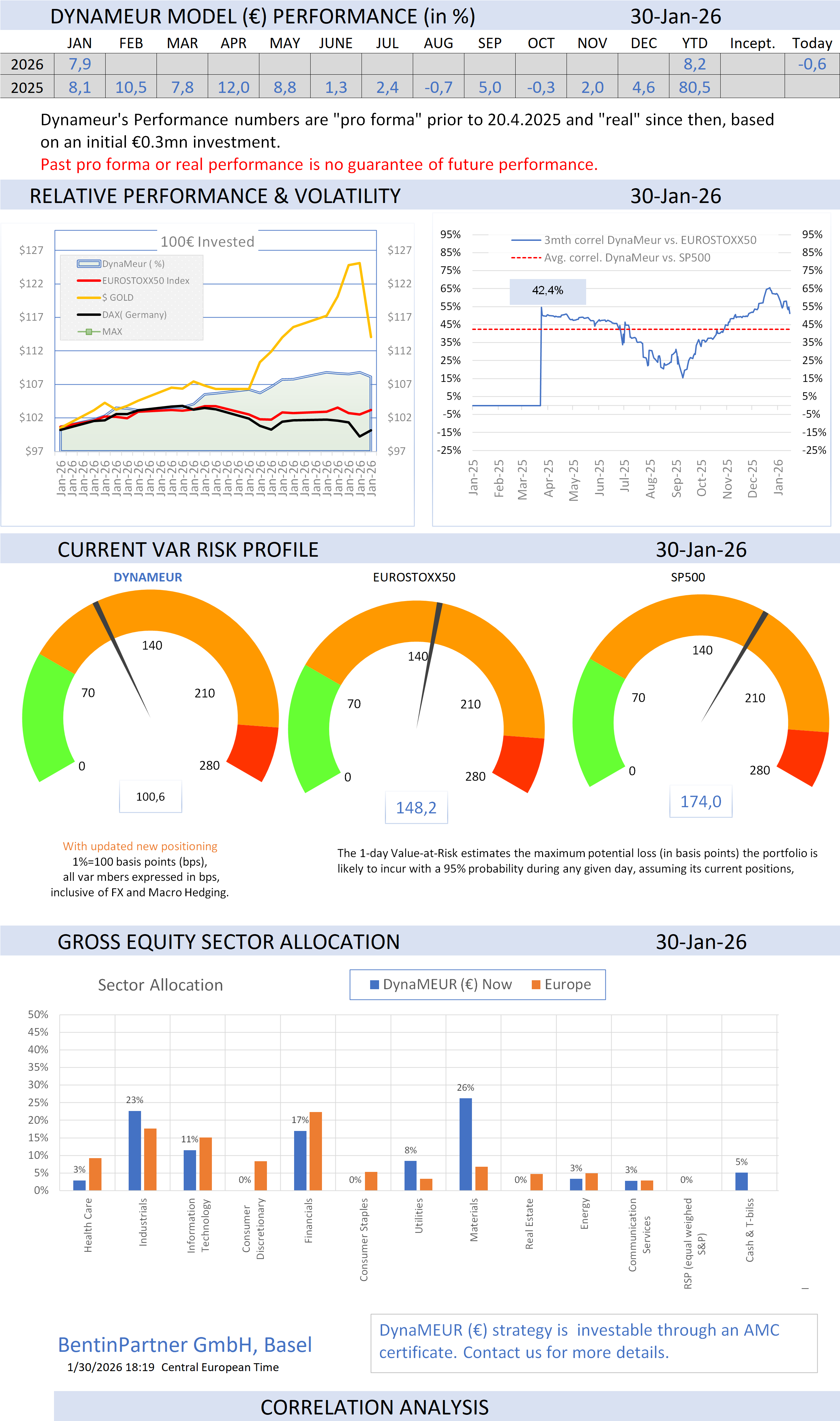

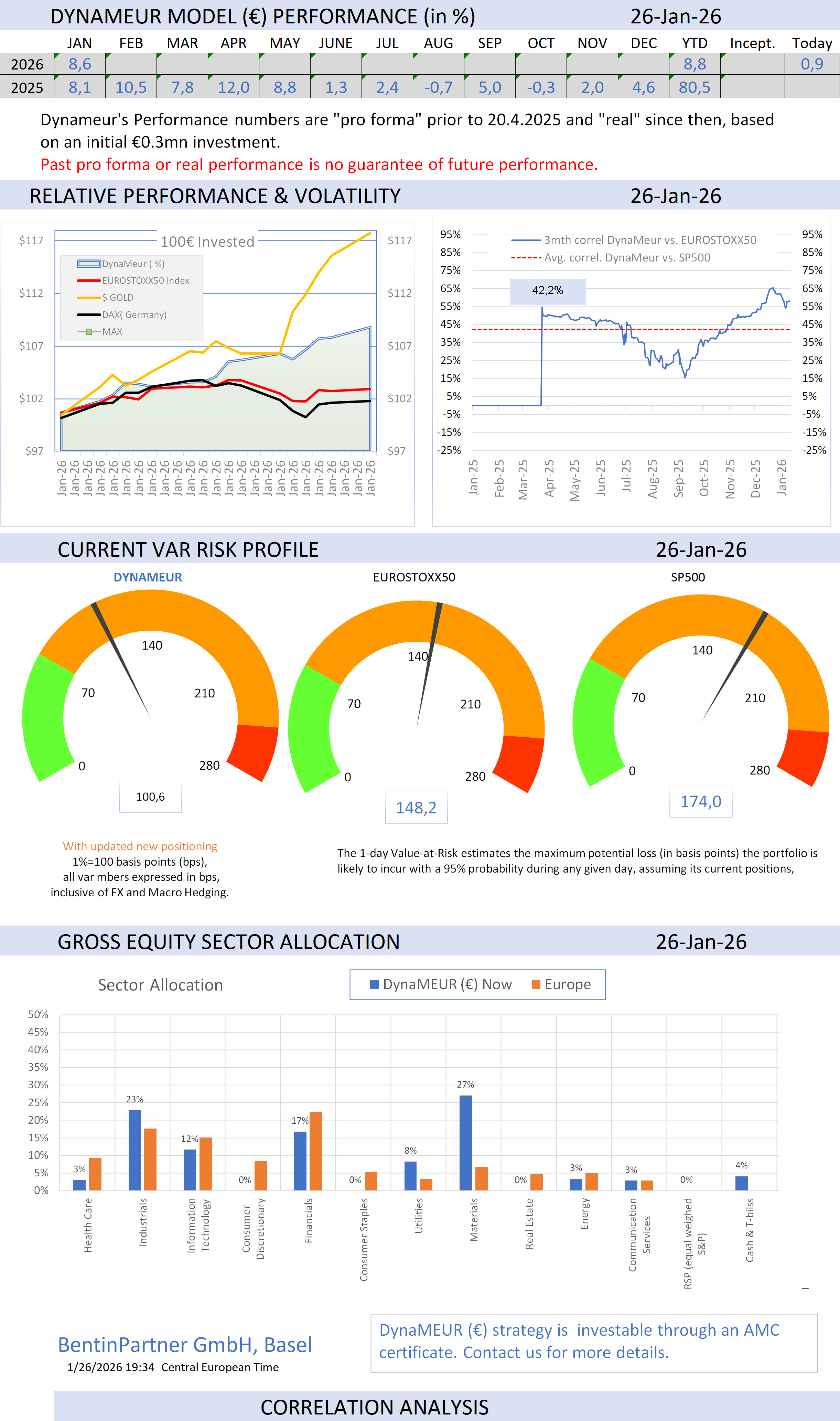

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments