Weekly Trend Status Update

- Marc Bentin

- Apr 14, 2019

- 5 min read

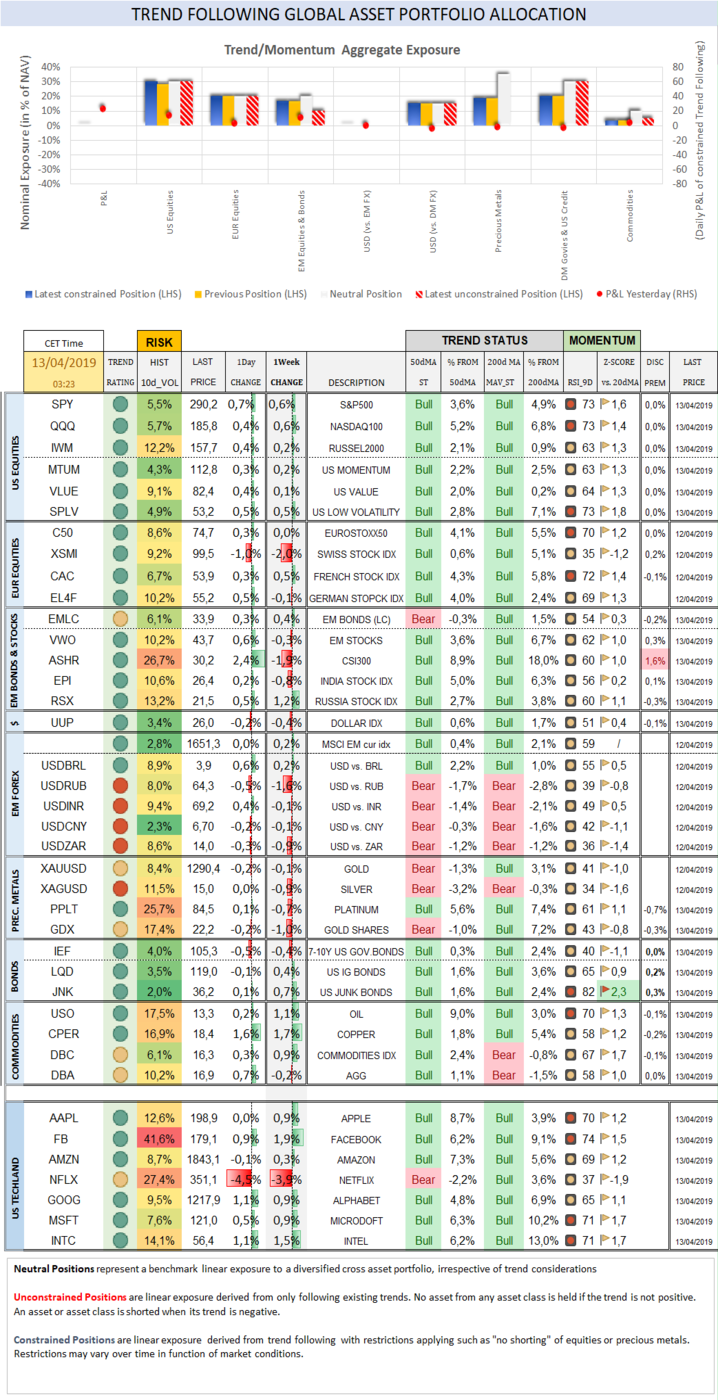

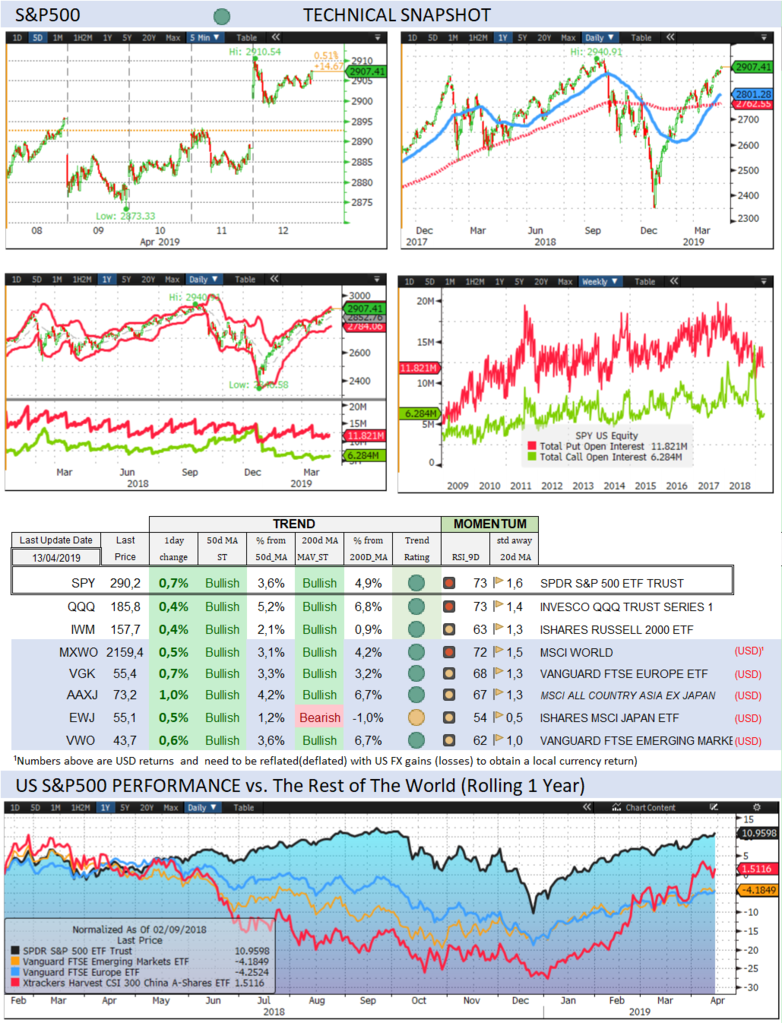

What a Week It Was…. Market changes over the past week were mostly uneventful although a slow grind higher (and pain trade for some) continued for US markets with the S&P500 adding 0,6% (16,1% YTD) and the Nasdaq showing a similar gain (20,5% YTD). The US small cap index added 0,2% (17,8% YTD). CBOE Volatility Index sold off by -6,3% to 12 (-52,8% YTD). In US tech land, AAPL gained 0,9% (26,1%), FB 1,9% (36,6%), AMZN 0,3% (22,7%) with only NFLX selling off by -3,9% (31,2%) following the compelling proposition presented on Friday with Disney+ which will offer “family” content and very serious competition to the streaming services of Netflix for just USD7 per month, starting in November. XLV (Health care sector) was the worst performing sector last week, dropping -2,4% (3,8%, Z-score -2,3) along with Biotechs. The Eurostoxx50 closed the week unchanged (14,4%), underperforming the S&P500 by-0,5%. Diversified EM equities (VWO) dropped -0,3% (14,8%), also underperforming the S&P500 by -0,8%. Although Chinese shares recovered nicely on Friday from Thursday’s stumble, the CSI300 Chinese equity index (ASHR) closed -1,9% on the week (37,8%). Russian shares (RSX) gained 1,2% (14,4%), supported by RUB’s 1.6% weekly gain and oil firming a little over 1% as well over the same period. The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,4% (2,0%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,2% (2,3%). MXN was particularly strong, gaining 1,7% (4,6%). Gold dropped -0,1% (0,6%) and Silver dropped -0,9% (-3,4%) while Major Gold Mines (GDX) dropped -1,0% (5,3%) on no particular reason that I could discern other than the optical need to keep it repressed. The bear raid that affected some commodities beyond precious metals as well was not enough to prevent the Goldman Sachs Commodity Index gaining 1,0% (18,6%) on the week. WTI Crude added 1,3% (40,7%) while Copper gained 1,7% (12,0%). Suggesting more flows went to credit markets last week, while 10Y US Treasury yields climbed 7bps (-12bps) to 2,57%, US Aggregate Corporate Average Spread over Treasuries dropped -6bps (-43bps, Z-score -2,8) to 1,10% while US High Yield (HY) Average Spread over Treasuries dropped -19bps (-177bps, Z-score -2,1) to 3,49%. 10Y Bunds climbed 5bps (-19bps) to 0,06% while EUR 5Y Subordinated Financial Spread dropped -16bps (-87bps) to 1,38%. 10Y Italian BTPs underperformed rising 6bps (-20bps) to 2,54%, underperforming Bunds by 11bps.

What We Are Doing & Thinking... Our paper tactical model (and actual portfolios) continue to favour holding a barbelled position between equities (with an inclination towards EM) and precious metals as a way to also position for dollar weakness and selective currency debasement later in the year. We stay out of bonds (and credit) and cautious buyers, more so than sellers of equity options to capitalize on momentum where developing trends are favourable and to occasionally implement tactical portfolio insurance. Implied Volatility dropped further last week, might well continue to do so for as long as central banks signals will remain rather universally dovish but has become way too low historically to be sustainable. One of the reasons why we prefer buying options than selling them has to do, beyond the fact that they are cheap, with our strong held (and widely shared) belief that market liquidity I scarce … despite it looking abundant. We refer not to the money flushing around but to the structural (tubing) liquidity deficiency of financial markets, be them credit or equity related. Air pockets and discontinued markets have become the rule not the exception. Liquidity is provided by light year fast moving robots withdrawing liquidity at any sign of problem (as amply illustrated in December and nearly every day since then in less visible ways). As the Spring IMF meeting draws to an end, the following FT article excerpt conveyed a similar concern of the IMF head of capital markets. Central banks and most likely D. Trump as well, must be similarly concerned to be flat out (or wanting even more) easing because at this juncture, no decline of anything (except gold perhaps) can be easily absorbed without causing instant panic...and recuperation. “Recent abrupt gyrations in financial markets could be the ‘tip of the iceberg’, according to a top International Monetary Fund official. Since the financial crisis, stricter regulations and commercial pressures have forced many banks to pare back or close their once-vast proprietary and market-marking desks. The latter have become more like independent high-speed traders, which are now some of the biggest intermediaries on global markets… Tobias Adrian, director of the IMF’s monetary and capital markets department, said that while banks were safer as a result, the implications for market ‘liquidity’ …were worrying. ‘There are no red flags at the moment, but obviously we haven’t seen a recession since the whole market-making system has morphed into this new system… We don’t quite know how that would play out if there’s a major adjustment.’” Ray Dalio’s recent warning against inequality found a similar echo in an OECD study published last week. “The middle classes in developed nations are under pressure from stagnant income growth, rising lifestyle costs and unstable jobs, and this risk fuelling political instability, a new report by the OECD has warned. The club of 36 rich nations said middle-income workers had seen their standard of living stagnate over the past decade, while higher-income households had continued to accumulate income and wealth. The costs of housing and education were rising faster than inflation and middle-income jobs faced an increasing threat from automation, the OECD said. The squeezing of middle incomes was fertile ground for political instability as it pushed voters towards anti-establishment and protectionist policies, according to Gabriela Ramos, OECD chief of staff.” (As reported by the FT) The silly pricing of upcoming Unicorns (LYFT was one, UBER will be next with many more to follow) will further build inequalities as most of these companies besides not making nor planning to make any money any time soon will yield hundreds of billions to VC’s and founders that will be selling. The money of these industry wide ‘disruptors’ will come straight from squeezing the income of “human resources” operating them for one part and from gullible, greedy and somewhat desperate (savings deprived) investors for the other.

———- To receive our daily updates and market reviews, consider our premium research: https://www.bentinpartners.ch/research And join our free trial. https://www.bentinpartners.ch/subscribe Important Disclaimer © Copyright by BentinPartner llc. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation or particular needs of any person who receives this report. Accordingly, the opinions discussed in this Report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner llc, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner llc. The content and views expressed in this report represents the opinions of Marc Bentin and should not be construed as guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner llc believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets or developments referred to in the Report. #fx #forex #investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants

Comments