Squeezing Further...

- Marc Bentin

- Apr 20

- 7 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Last week, global markets short squeezed further, embracing the scenario of appeasement and peace …which may or may not materialize at the look of the week end’s events.

While D. Trump seemed in a hurry to declare victory on all points of his negotiation with Iran, Iran responded over the week end by restoring its authority on the SoH and forcing all tankers trying to cross the strait to hit the reverse gear.

At this stage, Iran seems ready to challenge the US interpretation, saying that SoH remained closed as long as the US blockade persists.

There is no point going through the litany of grotesque declarations that went through last week that included D: Trump calling Italy’s Prime Minister “weak” for defending the Pope in doing what he is supposed to do (speak in defense of peace) or declaring that the straight is open (actually closed now) or that Iran agreed to return the uranium “dust” left in possession of Iran which may not be “dust” and which Iran seemingly did not agree yet to return…

D. Trump is in a hurry to declare an all-round victory saying “Iran has agreed on everything” while negotiating an off-ramp in the background because he cannot win this war (fast enough), despite making a lot of things go Boum!, creating a situation that now threatens the world economy. Another US President has done just that, JFK, which ended the US Cuba blockade (and very tense nuclear standoff) in exchange of the quiet removal of US Jupiter nuclear missiles from Turkey and Italy, which the United States agreed to do only privately, while publicly insisting that only the Soviet Union had made concessions… We can only hope this is what is going on…

This was a particularly enlightening interview to see through the fog of propaganda and wishful thinking from the former US Ambassador to the Soviet Union, an elder statesman like the Western world is missing so many, led by mostly (war) inexperienced and history illiterate war mongerers.

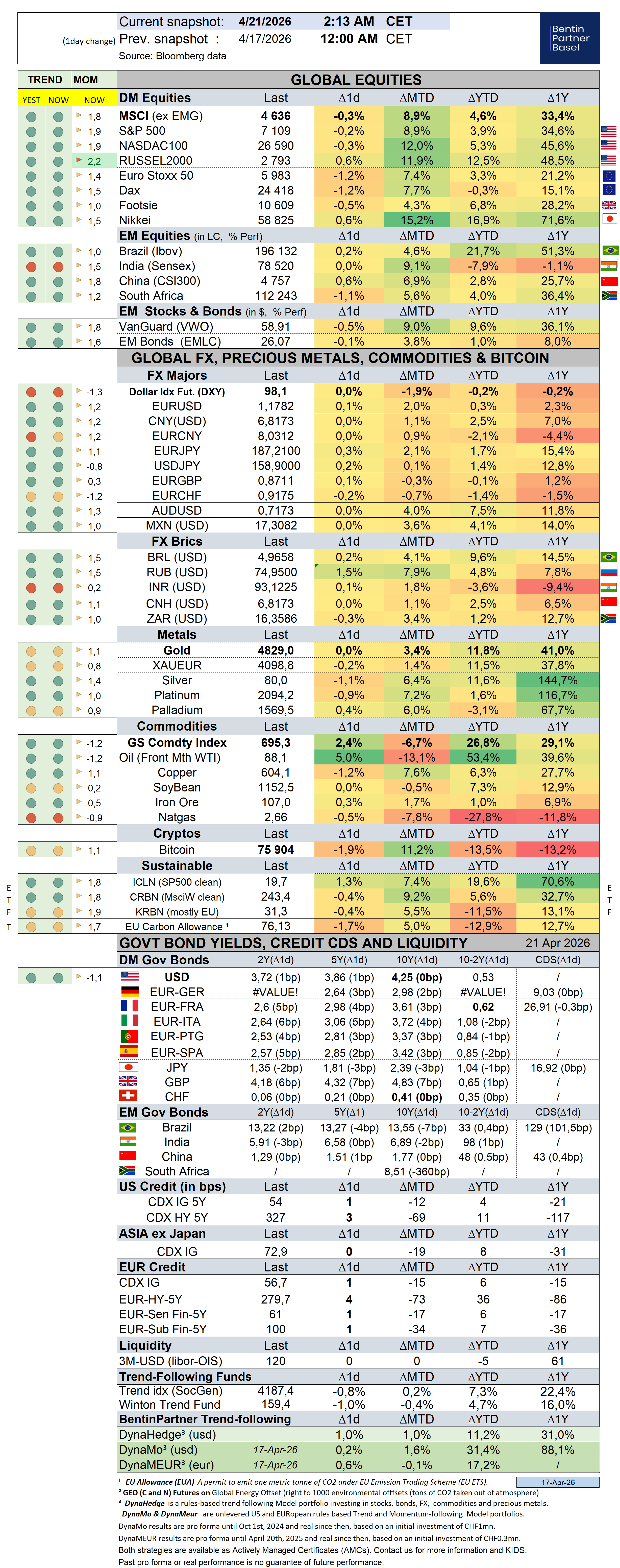

The SP500 gained a little over 4% (and Goldman’s most shorted index 3 times as much) last week with both SP500 and the Nasdaq reclaiming all-time highs with a chemistry of market dynamics that we referred to last week and which may or may not have much further to go but enabled stocks to rally for 13 days in a row.

Admittedly, sentiment was also jolted by major banks beating expectations in a big way but not unsurprisingly, this sector lagged the rest of the market, especially tech stocks (including software which staged a powerful rebound starting with MSFT and TESLA gaining 13% on the week as MAG7 but especially those two, initiated a strong recovery) while investors hurried to trim some oil shares (that might return in favor today as uncertainties remained) in order to capture more beta.

While stocks recovered, bonds also rallied, albeit more modestly, with US yields declining by 7 bps and Bunds by -10bps (despite some warning from H. Paulson on the risks that a lack of buyers would entail and urging authorities to have a “back-up” plan).

“The deficit is one trillion dollars. We are on a path to have it be USD3trn in 2025…And you look at this, clearly, we use the word “unsustainable” a lot. But this is on a path to destroy our economic well-being and our national security which is rooted in our national strength”, Paulson said. “The first rule of holes is to stop digging. And we are digging big time”, he warned.

The dollar was mostly weaker last week while precious metals and in particular silver surged +6.6% with copper also gaining 5% (as did bitcoin).

The FT reported that the last oil tankers to traverse the SoH before the outbreak of the war will reach refineries in the coming days, in a pivotal moment that analysts warned could herald physical shortages in Europe with US oil exports surging +1 mn b/d to a record last week as Asian and European buyers rushed to replace lost Middle Eastern crude.

Over the past week, the S&P500 rallied 4,5% (4,1% YTD) while the Nasdaq100 rallied 6,2% (5,6% YTD, Z-score 2,0). The US small cap index rallied 5,5% (12,0% YTD, Z-score 2,0). AAPL rallied 3,7% (-0,6%, Z-score 2,3).

The Equally Weighed SP500 rallied 3,3% (6,1% YTD, Z-score 2,0), underperforming the S&P500 by-1,2%. The median SP500 YTD return closed the week at 2,7%.

Cboe Volatility Index sold off by -9,1% (16,9% YTD) to 17,48.

The Eurostoxx50 rallied 2,4% (5,1%), underperforming the S&P500 by -2,2%.

Diversified EM equities (VWO) rallied 4,3% (10,1%), outperforming the S&P500 by -0,2%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,3% (1,2% ) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,3% (1,2%).

10Y US Treasuries rallied -7bps (8bps) to 4,25%. 10Y Bunds dropped -10bps (11bps) to 2,96%. 10Y Italian BTPs rallied -17bps (13bps ) to 3,68%, outperforming Bunds by -7bps.

10Y French OAT's rallied -13bps (2bps) to 3,58%, outperforming Bunds by -3bps.

US High Yield (HY) Average Spread over Treasuries dropped -12bps (0bps ) to 2,66%. US Investment Grade Average OAS dropped -1bps (1bps ) to 0,85%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -4bps (6bps) to 0,60%.

Gold gained 1,7% (11,8%) while Silver rallied 6,6% (12,9%). Major Gold Mines (GDX) gained 1,0% (17,0%).

Goldman Sachs Commodity Index dropped -0,7% (26,5%). WTI Crude sold off by -13,2% (46,0%).

Overnight in Asia…

Ø S&P future -40 points; Nikkei+0.8%

Ø Stock futures are starting weaker overnight (and already grinding higher) after last week’s optimism on a peace deal faded a little with seemingly more negotiation needed (which JD Vance said he would attend on Tuesday, assuming Iran agrees to hold these talks which it has not yet done).

Ø The zero percent remaining of Iran’s naval fleet forced the tankers hurrying to pass the strait to reverse gear on Saturday and oil recouped what it had lost on Friday after the SoH remained essentially cut off for maritime traffic over the week end.

Ø In response, US President D. Trump said the US Navy fired upon and seized an Iranian-flagged cargo ship in the Gulf of Oman after it failed to heed warnings to stop as it left the Strait of Hormuz. Trump said in a social media post earlier on Sunday. “NO MORE MR. NICE GUY!”. President Donald Trump, who on Friday said a deal with Iran was all but agreed, threatened by Sunday morning to destroy every power plant and bridge in Iran if negotiations fail.

Ø The UAE asked the US for a possible financial backstop, the WSJ reported.

Ø Hungary’s incoming leader, Peter Magyar, whose Tisza party scored a landslide election win a week ago, and who expects to form his new government in mid-May said on Friday that Druzhba flows from Russia may resume this week. Orban has conditioned the aid for Ukraine on the resumption of supplies via that pipeline.

Ø Keir Starmer is preparing for a showdown with the senior official he sacked over the appointment of Peter Mandelson as US ambassador, and will make a statement to the House of Commons as calls for the prime minister to resign grow, Bloomberg reported.

Ø Chancellor Friedrich Merz said he plans to convene Germany’s national security council to discuss the global energy crisis, signaling increased concern about its impact on Europe’s biggest economy.

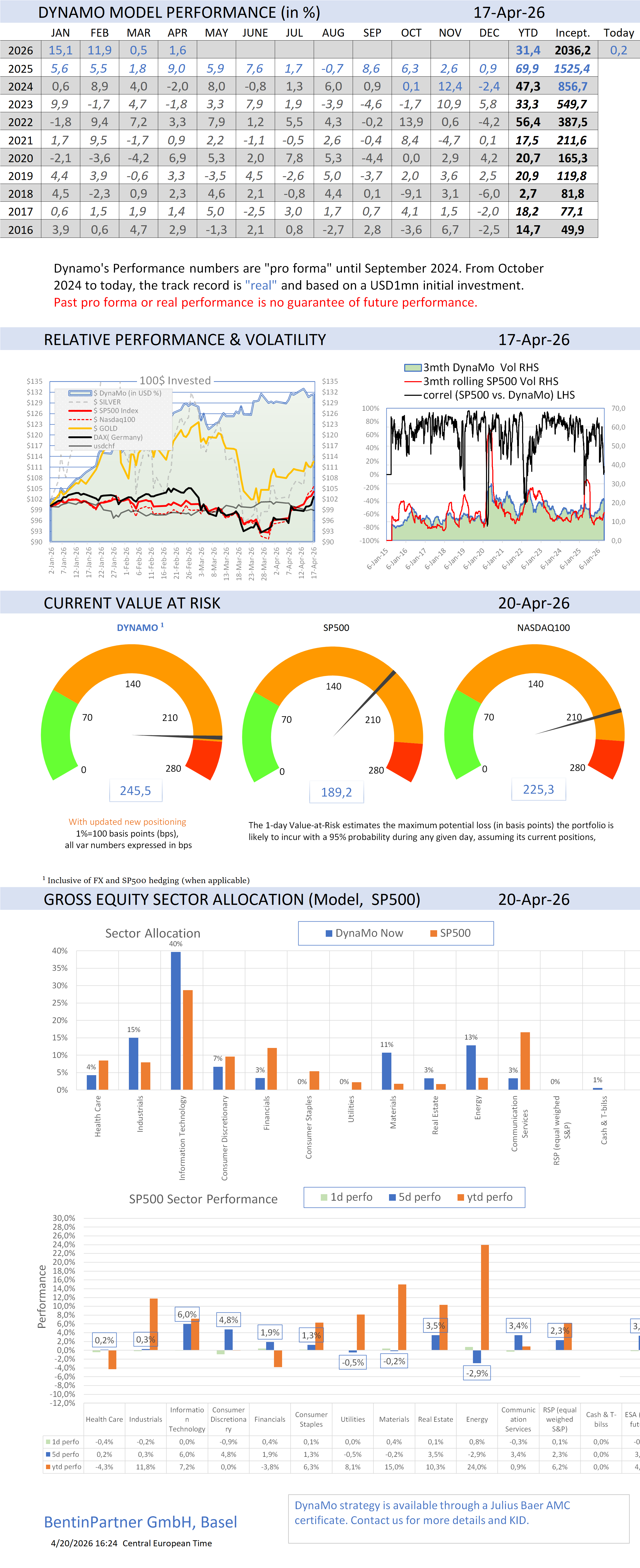

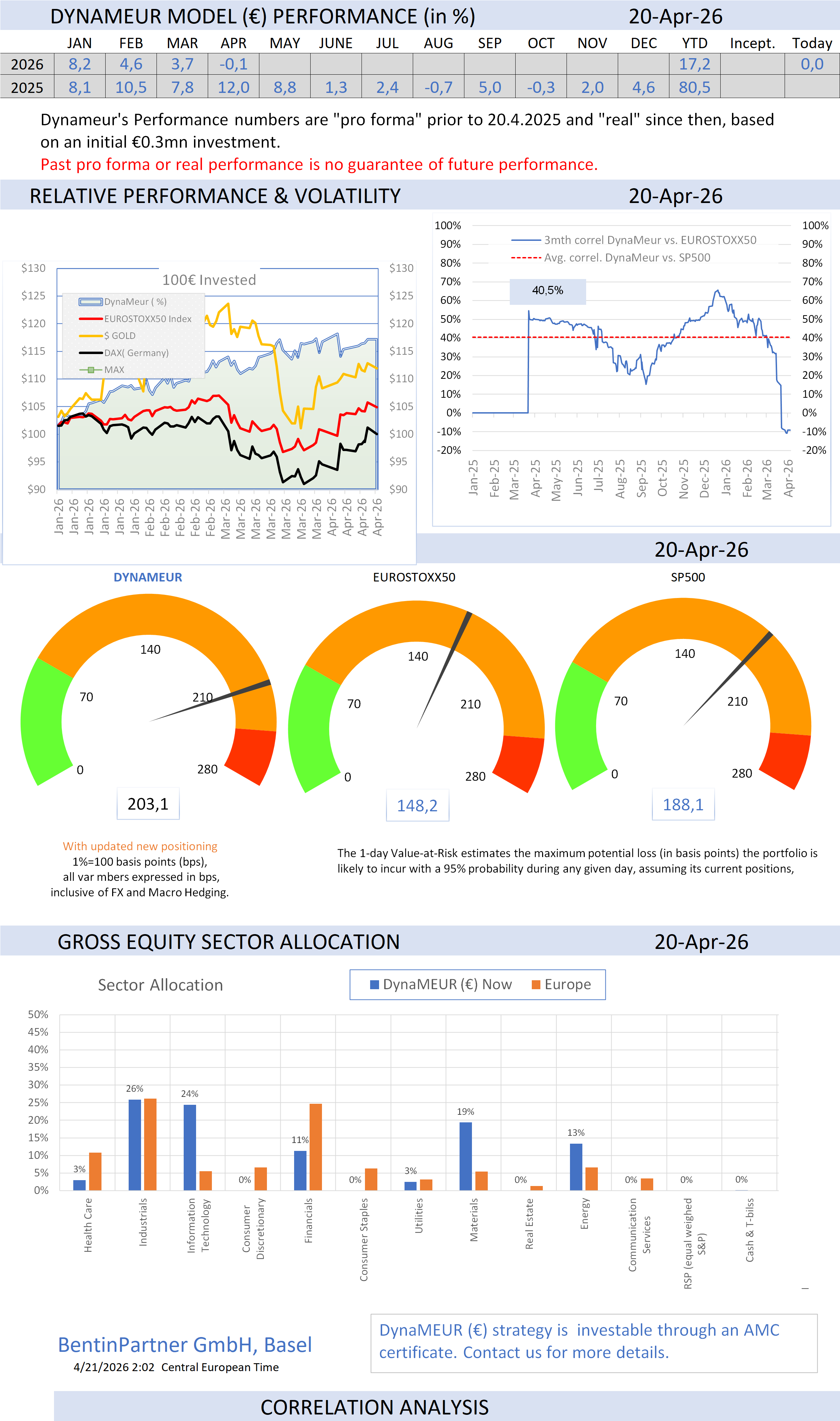

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments