Waiting For Big Tech Earnings..

- Marc Bentin

- Apr 27

- 7 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

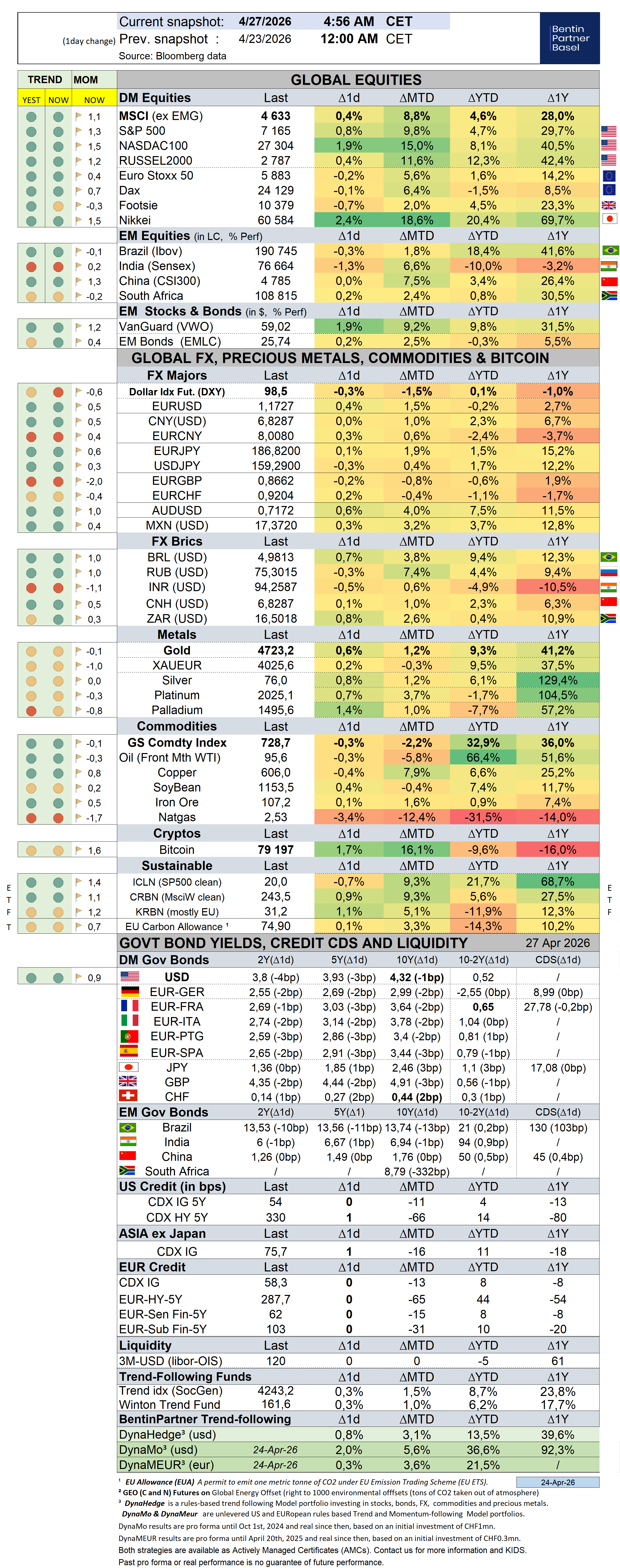

US stocks climbed, led by the Nasdaq 2% weekly gain, still taking in stride the Middle East war as they remained driven by continued positive AI headlines and big earnings performance that propelled the semi sector 8% higher. The breadth among tech was not that great however with IBM and ServiceNow ending the week 10% lower.

WTI still surged 12%, propelling the broader commodity index 3.5% higher as well.

US Treasury yields dropped slightly in opposition with what they did in Europe in Japan with Treasuries reassured by K Warsh’s Congressional hearings for his nomination where he committed to stick to the Central Bank independence and to not take his orders from the US President.

“The president never asked me to predetermine, commit, fix, decide on any interest rate decision in any of our discussions, nor would I ever agree to do so.” “Now, the President, as you might know, much like virtually all presidents I’ve either known or studied, presidents tend to be for cutting rates. I think the difference is President Trump expresses it quite publicly without surrogates or subterfuge, but presidents want lower rates.”, K Warsh subtly opined. “Working with the Treasury Secretary, we’re going to have to find a way in which we can take the balance sheet and make it smaller, because a large balance sheet where the Fed owns more outstanding debt than many parts of the financial markets, that’s fiscal policy in disguise. The Fed needs to get out of the fiscal business, focus on the monetary business, so the Fed can deliver on the remit you gave us.”, Warsh also commented, delivering a blunt critic of QE (of which he approved USD1trn in 2008, however).

Credit markets did not play ball and HY spreads widened with private credit troubles still a looming concern and major players and their funds underperforming (OWL, KKR). The FT reported that big banks such as Morgan Stanley, UBS and Bank of America Merrill Lynch and other independent wealth managers benefited from the boom in private funds targeting individual investors before it started to sour last year…. ‘The advisers themselves are stuck in this incentive structure where their behaviour is going to be aligned with pushing clients into these products’ ‘It’s not a surprise that this stuff has been over-allocated to the retail investor base’.”, the FT reported analysts saying.

On the lack of resolution of the conflict, D. Trump clamored several times that he holds all the cards and that he has time working for him while Iran does not which is questionable considering a. the international pressure to reopen the SoH and prevent the global economy from choking, b. the fact that D. Trump faces a meeting with his Chinese counterpart in May and c. that Trump will soon be pressured by Congress to end the war as well which he started without its authorization. Iran on its side has “vast amounts of oil pouring through their pipes system which if it cannot be put on containers threatens to explode from within” Trump said, justifying Iran’s time constraint.

Last week, UAE said it was considering a formal funding request, warning that if it runs out of dollars, it may be forced to use Chinese yuan or other currencies for oil sales and other transactions, hinting that UAE may be forced to seek US financial backing. It may also be forced to sell liquid assets like treasury bonds for fiscal support, a decision which would both hurt US bond yields and threaten the stability of the region’s currency pegs to the USD. Late on Friday, S. Bessent tweeted in defense of the possibility of the US participating in currency swaps in the Persian Gulf and Asia.

Going into the week end, efforts to resume peace talks over the Iran war stalled after D. Trump canceled a planned trip by Jared Kushner and Steve Witkoff (two US real estate agents which Iran obviously fails to consider as serious negotiators). At the same time, Iran said it won’t negotiate while being threatened and Iranian Foreign Minister said he will convey Iran’s conditions for ending the war, including a new legal framework for Hormuz, lifting the blockade, compensation for damage, and guarantees against further military action.

On the Ukraine front, Ukraine started receiving a €90 billion loan from the EU to keep the country going for one year (in addition of another EUR15bn requested for military spending) which the ailing EU tax payers will fund after Hungary lifted its veto. They also approved a fresh package of Russian sanctions at the meeting. On the same week, a Ukrainian billionaire bought the most expensive flat in the world worth EUR540mn in Monaco (besides owning the most expensive EUR900mn yacht in the world and several properties in Miami).

Heralding the busiest week of the year, this week earnings’ releases are likely to be critical with Alphabet. Microsoft, Amazon and Meta worth nearly $16trn combined or a quarter of the S&P 500 Index, are expected to report Wednesday, and Apple on Thursday.

The Fed, ECB, BoJ, BoE and BoJ and BoC are also all scheduled to set interest rates this week, starting with BoJ tomorrow in a context of renewed price pressures (but with $$none expected to hike rates).

Amid the sudden reported de-grossing of hedge fund positions, the pain trade is likely to remain higher, Goldman reported.

Over the past week, the S&P500 gained 0,5% (4,7% YTD) while the Nasdaq100 rallied 2,3% (8,1% YTD). The US small cap index gained 0,3% (12,4% YTD). AAPL gained 0,3% (-0,3%).

The Equally Weighed SP500 dropped -0,6% (5,5% YTD), underperforming the S&P500 by-1,1%.. The median SP500 YTD return closed the week at 3,4%.

Cboe Volatility Index rallied 7,0% (25,2% YTD) to 18,71.

The Eurostoxx50 sold off by -2,9% (2,0%), underperforming the S&P500 by-3,4%.

Diversified EM equities (VWO) dropped -0,3% (9,8%), outperforming the S&P500 by -0,8%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 0,4% (1,7%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,3% (0,9%).

10Y US Treasuries dropped 5bps (13bps) to 4,30%. 10Y Bunds climbed 3bps (14bps) to 2,99%. 10Y Italian BTPs underperformed rising 10bps (23bps) to 3,78%, underperforming Bunds by 7bps.

10Y French OAT's underperformed rising 6bps (8bps) to 3,64%, underperforming Bunds by 3bps.

US High Yield (HY) Average Spread over Treasuries climbed 6bps (6bps) to 2,72%. US Investment Grade Average OAS was unchnaged (1bps ) to 0,85%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 2bps (8bps) to 0,62%.

Gold sold off by -2,5% (9,0%) while Silver sold off by -6,4% (5,7%). Major Gold Mines (GDX) shed -6,0% (10,0%).

Goldman Sachs Commodity Index rallied 5,5% (33,5%). WTI Crude rallied 12,6% (64,4%).

Overnight in Asia…

Ø S&P future +10 points; Hong Kong -0.1%; Nikkei+1.4%; China +0.3%

Ø US futures dropped mildly before erasing all losses and climbing 0.2% while crude oil gained 1% after peace talks between the US and Iran stalled, prolonging the closure of the SoH over the week end but with Iran also reported to have given the US a new proposal for reaching a deal to reopen the SoH, ending the war with nuclear negotiations postponed for a later stage, Blomberg wrote.

Ø The man who stormed the White House Correspondents’ Dinner earned a mechanical engineering degree from Caltech in 2017 and was pursuing a master’s degree in computer science at California State University-Dominguez Hills as recently as 2025, Bloomberg reported. He did send a lengthy manifesto to family members that was seen by Bloomberg where he appeared to blast President Donald Trump as a “traitor” who committed crimes.

Ø BoJ will deliver its policy decisions early tomorrow (where policy rates are expected to remain unchanged) with investors still encouraged by strong corporate earnings and the AI boom “while keeping the US-Iran situation on their side mirrors”, analysts opined.

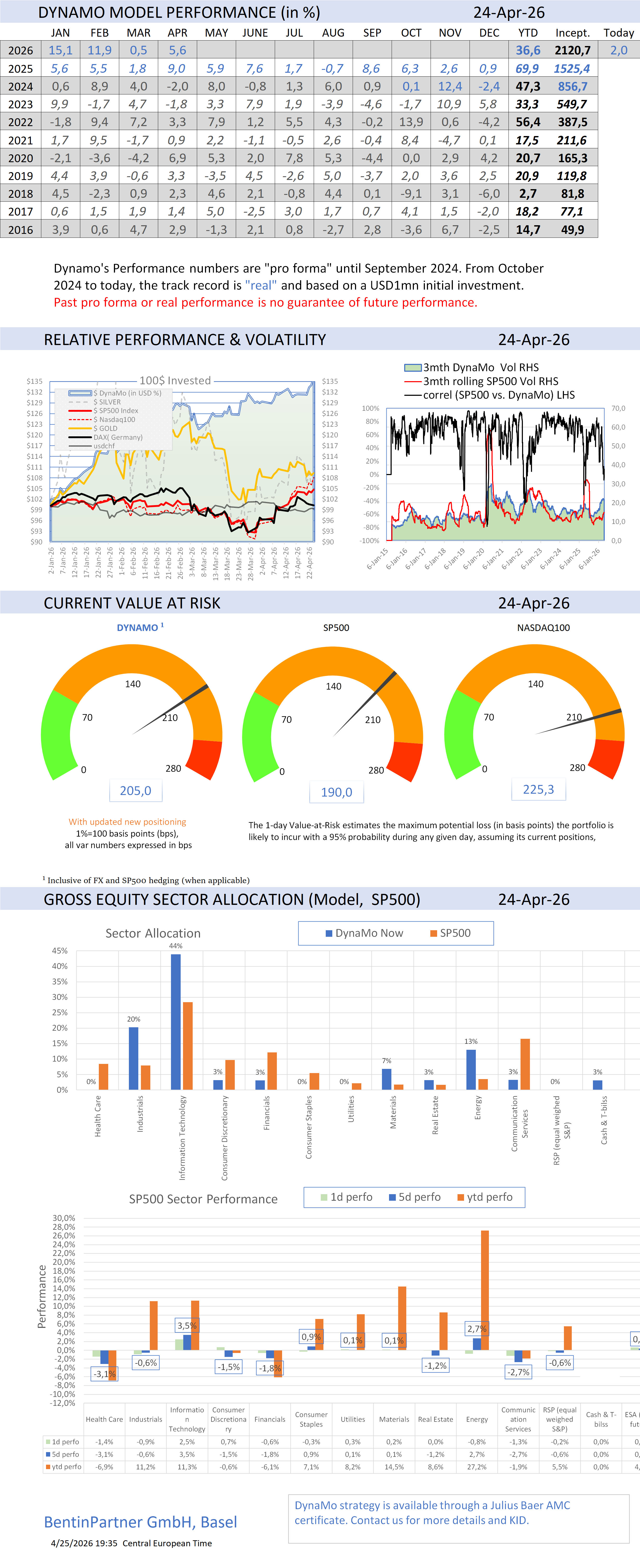

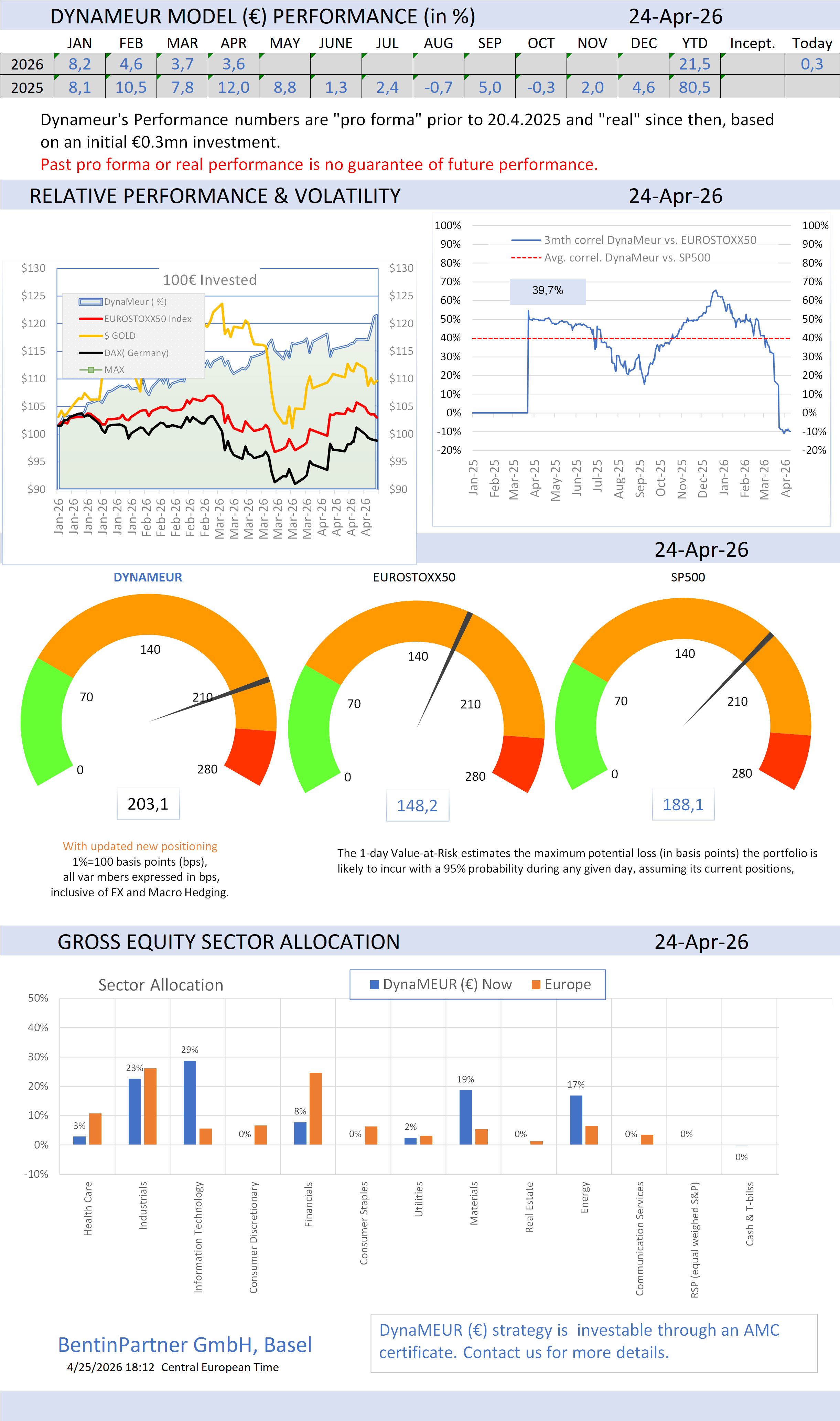

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments