7trn $ Tracking the SP500...

- Marc Bentin

- Jun 8

- 8 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Last week action was incapsulated for the most part in last Friday’s all-round selloff which hit across markets, signaling a distinct return of risk aversion of which the catalyst was the “good news” of a seemingly much stronger than expected Non-farm payrolls on Friday which led to some rerating of US monetary policy tightening expectations… Normally I take a day off (from markets) on every NFP Friday because for as long as I have been in markets, I have seen people over-reacting on a time serie that has lost all credibility over the years due to being systematically overrating job growth only to be revised sharply lower by some dramatic number once a year.

That said, May’s 172k gain in Non-farm Payrolls was double the estimates of 88k while the previous number was revised higher as well while the ADP, reported earlier in the week showed May employment gains of 122k, the strongest reading since January 2025, establishing some overall strength in the job market. Only the jobless claims published on Thursday, higher than expected, seemed to contradict this view of a strengthening job market.

The May ISM Manufacturing Index also rose to a stronger-than-expected 54.5 (from 53.8 expected) while the ISM Price paid (looked for its inflation guidance) index declined slightly.

Perhaps more materially, in my view, the key catalyst for Friday’ blast lower was a decision by S&P, defying previous expectations, not to fast track the entry of SPACEX into its flagship SP500 index which is by far the most followed index, tracked by USD7trn of investors’ money. The hope so far was for S&P to skip their long-held obligations for a company to show 4 consecutive quarters of profit, have 10% of its float listed and one year of public trading, before being added to the index. What S&P announced last Friday may simply have meant that SPACEX may ultimately not enter the SP500 for years, unless the 4 quarters of profit requirement is lifted.

The Russel and Nasdaq will maintain their own fast-tracking exception but their “real money” impact is far less (only 500bn are tracking the Nasdaq vs. 7trn tracking the SP500. This came as a shock (including to E. Musk most likely) and the implication is that a lot of people including institutional investors who thought they would have to buy SPACEX (and the next multi trillion tech IPO) had no other choice but running to buy surrogates in the AI bubbling space (which include the chip sector which was among the hardest hit on Friday with a loss of -11%).

Once, this new reality struck (compounded by the wrongly in my view expectation that the Fed might have tighten rather than ease later this year), many investors found themselves overdosed in the tech sector and the rotation into value turned into high gear (value also dropped on Friday but much less).

Rik appetite received no help from the lack of progress of so-called peace negotiations in the Middle East which remained in a stalemate situation, as Hezbollah’s leader also rejected the latest ceasefire agreement between Israel and Lebanon’s governments, after Israel pressed ahead with military operations against the militant group in southern and eastern Lebanon.

At the same time, domestic political pressure built on D. Trump after the Republican-led House voted to halt the US war with Iran. The 215-208 vote Wednesday showed worries over the war spreading five months before congressional elections… Last month, a Senate resolution was also advanced though that legislation hasn’t yet come to a formal vote.

There was also no progress on the Eastern war front as Ukrainian drones hit an oil terminal in St Petersburg and a warship in dry-dock at a nearby naval base, hours before Vladimir Putin’s showcase economic forum got under .way in the city. The day before, Russia had launched hundreds of drones and dozens of missiles against Kyiv and other Ukrainian cities in response to the Ukrainian killing of 25 school children.

The AI bubble has been looking for a needle for a long time, defying expectations of the most optimistic investors that the stratospheric valuation reached in the sector can be maintained and even allowed to grow further.

That said, the reason for near term optimism remains the billions of dollars in fees that Wall Street firms are set to collect from the IPO of SPACEX (while Anthropic and OpenAI could complete the IPO picture later in September) and maybe this will be sufficient for the market to remain resilient until (at least) next Friday, the day when SPACEX finally hits the market.

In any case, risk might have to be taken more seriously from now on, because the wounds inflicted last Friday are already profound spanning well beyond stock markets, towards Bitcoin (which dropped down to $60,000 or a brutal 18.9% on the week), and even precious metals. South Korea dropped -14%, while uranium, Silver, Bidu and even the more defensive Moderna all dropped by close -10% on Friday.

The VIX increased by 6 points on Friday and I would not expect vol to decline over the near term which may also guide investors towards a more conservative positioning (it certainly did for us), especially because the exceptional rally witnessed since March 31st which included a lot of short covering, has been nothing but breathtaking and historic.

Treasuries also remained under war and supply (from the tech lords …) and saw related selling pressure that spun across the globe, with 10Y yields rising 6bps on Friday (implying a full 25 bps Fed hike this year), following the stronger than expected NFP report that left few places to hide, showing one more time that bonds have become a very imperfect safe haven.

At the same time, in the credit space, Blackstone limited redemptions from its flagship private credit fund for the first time after investors sought to pull 10% of the shares, the latest firm to cap withdrawals amid a continued investor exodus in contrast to the previous quarter, when BCRED, made every effort to allow investors to pull all of the 7.9% of shares requested..., Bloomberg reported. More private credit funds remained at risk of losing the investment-grade ratings on their debt as they continue to face elevated redemption requests, Bank of America wrote.

Elsewhere in Europe, EU inflation rose to 3.2% in May, seemingly bolstering the case for the ECB to raise interest rates for the first time in nearly three years this week as it seeks to contain price pressures unleashed by the conflict in the Middle East (and in Ukraine).

It was also said that BoJ Governor Kazuo Ueda had baked in a June rate hike as well in a clear narrative pivot toward inflation fighting (and more likely to counter buying pressure on USDJPY).

In the context of risk aversion, the dollar rallied across the board.

In a context of rising yields and strengthening dollar, the precious metals was also dragged down.

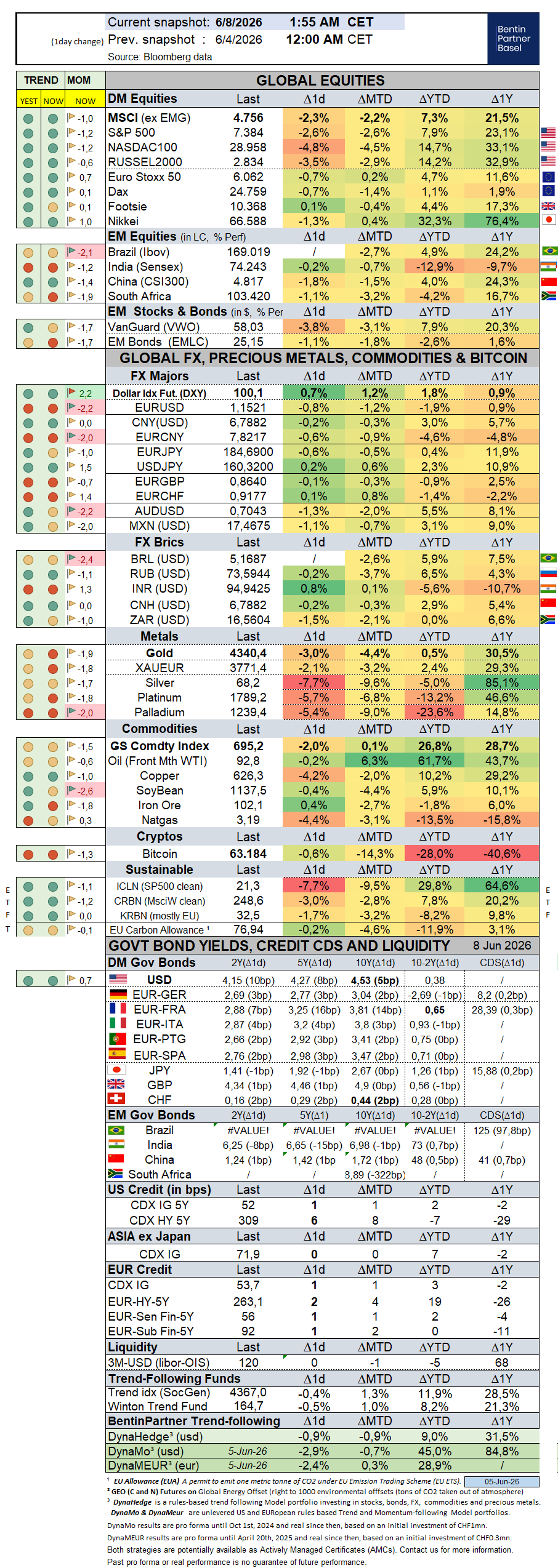

Over the past week, the S&P500 sold off by -2,5% (8,2% YTD) while the Nasdaq100 sold off by -4,5% (14,8% YTD). The US small cap index sold off by -3,0% (14,4% YTD). AAPL dropped -1,5% (13,1%).

The Equally Weighed SP500 dropped -0,5% (8,5% YTD), outperforming the S&P500 by 2,0%. The median SP500 YTD return closed the week at 4,9%.

Cboe Volatility Index rallied 40,4% (43,9% YTD, Z-score 3,1) to 21,51.

The Eurostoxx50 gained 0,2% (6,4%), outperforming the S&P500 by 2,7%.

Diversified EM equities (VWO) sold off by -3,1% (7,9%), underperforming the S&P500 by-0,6%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 1,3% (3,7%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,8% (0,4%).

10Y US Treasuries underperformed with yields rising 9bps (36bps) to 4,53%. 10Y Bunds climbed 10bps (18bps) to 3,04%. 10Y Italian BTPs underperformed rising 15bps (25bps) to 3,80%, underperforming Bunds by 5bps.

10Y French OAT's underperformed rising 14bps (13bps) to 3,69%, underperforming Bunds by 4bps.

US High Yield (HY) Average Spread over Treasuries climbed 8bps (-1bps) to 2,65%. US Investment Grade Average OAS climbed 1bps (-5bps) to 0,79%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 0bps (2bps) to 0,56%.

Gold sold off by -3,3% (0,5%) while Silver shed -9,1% (-5,1%). Major Gold Mines (GDX) sold off by -11,9% (-8,1%, Z-score -2,0).

Goldman Sachs Commodity Index dropped -0,8% (30,7%). WTI Crude gained 0,5% (61,4%).

Overnight in Asia…

Ø S&P future +x points; Hong Kong +0.0%; Nikkei+0.0%; China +0.0%

Ø Asian shares extended their selloff overnight as oil (+3%) and bonds fell following more military exchanges in Iran and Lebanon and as the Korean exchange dropped -5% on more AI liquidation selling.

Ø Donald Trump said the Federal Reserve would be wrong to raise interest rates…as he sought to push back against market sentiment after a “blowout” US jobs report for May spurred bets that the Fed’s next move will be a rate hike to keep inflation in check.

Ø Israel said it struck several military targets in Iran, retaliating against missile attacks by Tehran despite President Donald Trump’s call for Prime Minister Benjamin Netanyahu to refrain from hitting back.

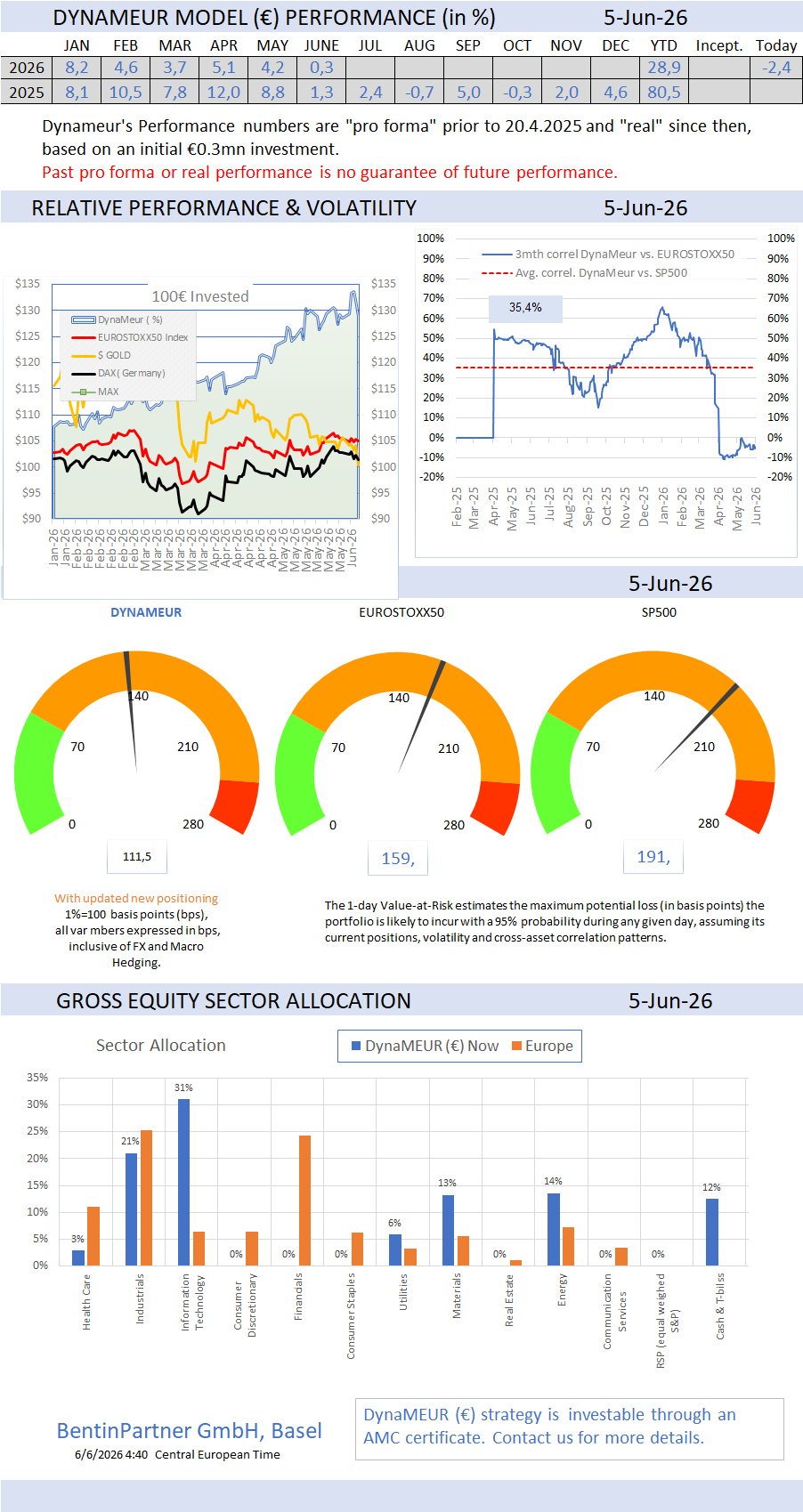

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments