Gearing for Historic IPO’s

- Marc Bentin

- Jun 1

- 7 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

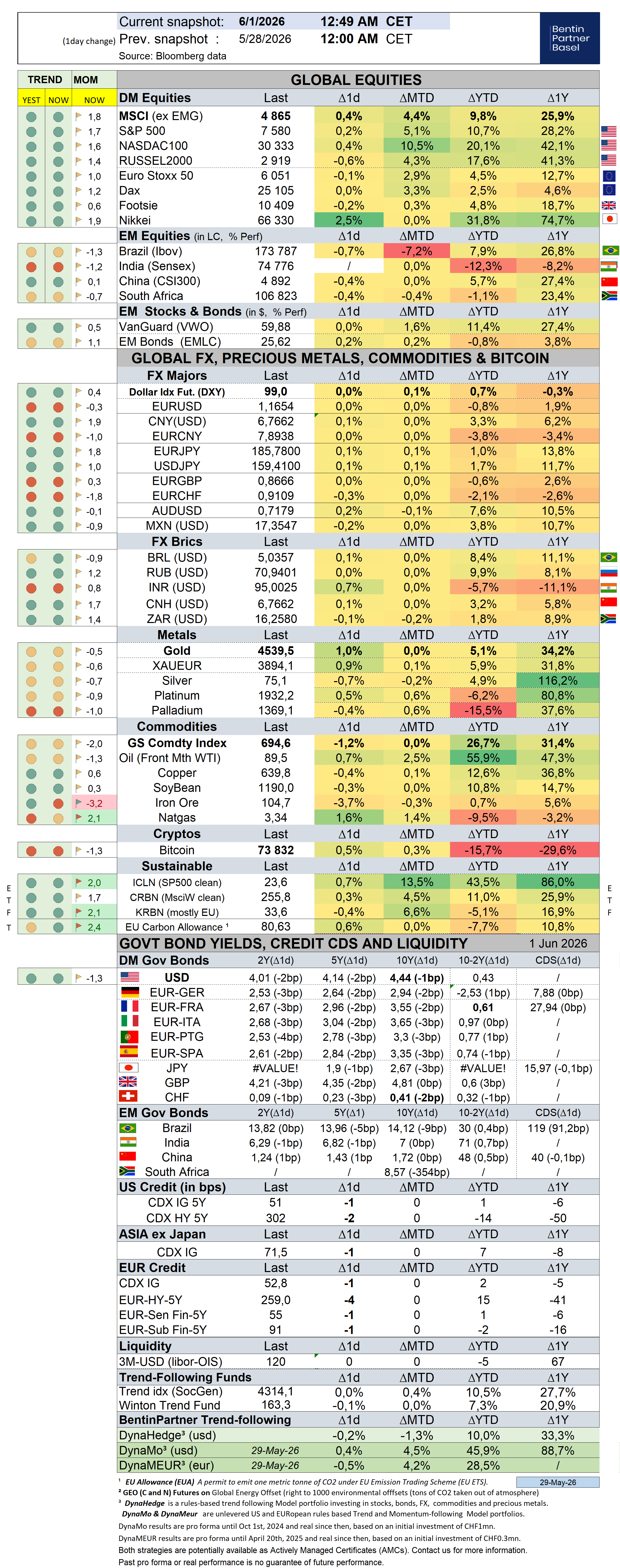

As US stocks completed their ninth consecutive weekly gains, closing at fresh all-time highs at the end of the week, BoA strategist M. Harnett lamented about the biggest bubble since the railroads but fighting the move took even more courage as the US gears for historic IPO’s and a Fed likely to signal top policy tightening.

One thing is clear, this rally continued to lack in breadth with a big sucking sound heard from the AI trade at the expense of almost everything else. Only 21 stocks of the SP500 traded at new highs (ominously in line with March 2000 stock market top) and 222 stocks traded 20% below their peak while another 20% traded some 40% below their peak.

Again, last week, the tape was driven by semiconductor stocks which gained 5.1%, now standing with an 81% ytd gain Micron added 27% on the week while another AI hardware provider, Dell closed the week with a 42% gain.

With the notable exception of Korea (+100% ytd) and its chip heavy index, most Asian equity markets traded lower last week as investors continued to make space for the AI trade and as local economies continued to suffer from the war in the Middle East. European equities barely moved last week as well.

Ed Yardini dismissed the overwhelming concerns that US stocks are in a bubble, talking about FEMO (“Fabulous earnings Momentum”) rather than FOMO (“Fear of Missing Out”) as being the main driver, noting that a forward PE of 20-22 looks reasonable to him without a recession which remains a hard call to make (for the US).

It seems, according to CNBC, that family offices are planning for some big changes in their portfolios in years, to move money outside of the US, according to a recent survey. For such a decision to turn out right, in my view, a US recession and a failed set of IPOs are needed and this is far from assured because as Europe falls in recession (that is a near certain outlook), it will keep regulating as the US will keep innovating…unless a drastic change occurs at the EU governance level. In contrast, Hedge Funds seem to be “all in” on the Ai trade…according to Goldman Sachs latest “Hedge Fund Trend Monitor” tracking 1000 hedge funds.

That said, another difference perhaps with 1999 is the explosion of global debt levels and the near parallel ballooning of the Fed’s balance sheet …but let’s not go there this week as bonds also behaved quite well last week (whatever the reason was) with global bond markets enjoying a respite, dropping between 10 and 15bps across geography. Perhaps also helping was an FT article noting that US regulatory easing has allowed top US and UK banks to expand their balance sheet by 15% or USD2.9trn in the past two quarters, essentially adding the size of another Citi into the mix while greater capital requirements for European banks will instead squeeze their balance sheet capacity by USD1.3trn.

But even if we go there (worrying about bond yields), after all, too much debt can only be resolved by lower rates, financial repression and essentially money printing which is where we are going in my view. And that would potentially be very bullish for stocks…

A key point for the bond market will be K. Warsh “real” attitude, now that he has been confirmed as the new Fed Chair (he worked 15 years for Stan Druckenmiller’ Hedge fund, making him the second highest ranking US Finance official of that breed). He is well versed in the hedge funds massive leverage in place in the Treasury market (and unlikely to rock the place), but also in the European bond markets, which led last week’s ECB Financial Stability Review to “warn about the growing presence of more price sensitive investors (at the expense of buy and hold investors such as central banks, which continue to reduce their holdings of US Treasuries), which could amplify any abrupt repricing of sovereign risk.

HY credit spreads narrowed last week as well, supported by higher stocks while the curve flattened (with short dated securities underperforming) as the market still seems inclined to believe that the Fed will deliver a token 25bps hike (before ultimately sending rates lower, in my view).

The US dollar traded slightly lower (by -0.3%) last week with some notable strength in NZD (+2.4%) and ZAR (+1.5%).

Gold and silver continued to trade sideways, looking for afresh impetus.

On the US economy side, the Fed preferred inflation gauge (PCE) rose to a three year’s high by 3.8%, the fastest pace in 3 years which could set the Fed en route for this “one and only” more rate hike.

Indicators of economic strength were mixed but fairly resilient so far. American Airlines reported strong demand for travel despite high jet fuel costs and higher priced tickets….at the same time as consumer confidence hedged down, providing more evidence of the K shaped nature of the US economy.

Anecdotally perhaps, San Francisco rents spiked by 22% in a year, evidence of a latest and local real estate boom that sent the median 2-bedroom flat rent to $5’500 supported by the booming AI stocks. In the meantime,

On the geopolitical side, nothing new materialized last week with President D. Trump continuing to suggest that a deal with Iran is close but apparently still out of reach with Iran’s ultra hardliners also hitting out at the country’s negotiators over a potential deal with the US.

Treasury Secretary S. Bessent opined that Iran had made “a big mistake by attacking its neighbors in the Persian Gulf”, referring to the decision that has made the US military offensive be held in check (and most likely the very reason why the cease fire is claimed to be still holding).

Last week, Israeli Prime Minister B. Netanyahu instructed its military to expand its maneuver in Lebanon with the Israeli army also claiming it took down 900 Hezbollah terrorists since the start of the cease fire on April 16th.

In the meantime, the Trump Administration is bracing waiting for a potential collapse of Cuba’s government with D. Trump preferring a “peaceful strangle transition to a “free Cuba” military mission.

Potential market moving events I the coming days and couple of weeks will be the US CPI print (at 4%) on June 10th, an (erroneous?) ECB rate hike on June 11th and Warsh first press conference on June 17th…

Over the past week, the S&P500 gained 1,9% (10,9% YTD) while the Nasdaq100 rallied 3,3% (20,2% YTD). The US small cap index rallied 2,8% (18,0% YTD). AAPL rallied 2,3% (14,8%).

The Equally Weighed SP500 rallied 2,0% (9,0% YTD, Z-score 2,0), outperforming the S&P500 by 0,2%. The median SP500 YTD return closed the week at 3,8%.

Cboe Volatility Index sold off by -8,6% (2,5% YTD, Z-score -2,3) to 15,32.

The Eurostoxx50 gained 0,7% (6,3%), underperforming the S&P500 by-1,1%.

Diversified EM equities (VWO) rallied 2,0% (11,4%), outperforming the S&P500 by 0,2%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies dropped -0,3% (2,3%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,3% (1,2%).

10Y US Treasuries rallied -12bps (27bps ) to 4,44%. 10Y Bunds dropped -10bps (8bps) to 2,94%. 10Y Italian BTPs rallied -12bps (10bps) to 3,65%, outperforming Bunds by -2bps.

10Y French OAT’s rallied -12bps (-2bps ) to 3,55%, outperforming Bunds by -2bps.

US High Yield (HY) Average Spread over Treasuries dropped -3bps (-9bps) to 2,57%. US Investment Grade Average OAS was unchanged (-6bps ) to 0,78%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -2bps (1bps) to 0,55%.

Gold dropped -0,7% (5,0%) while Silver sold off by -3,8% (4,8%). Major Gold Mines (GDX) rallied 4,1% (4,3%).

Goldman Sachs Commodity Index sold off by -4,0% (31,8%). WTI Crude sold off by -7,4% (55,8%).

Overnight in Asia…

Ø S&P future +21 points; Hong Kong +0.8%; Nikkei +1%; China -0.5%

Ø US futures and Asian shares gained, led by the KOSPI 3.5% gain as investors continued to pile on AI trades. At the same time, oil rose 2% as the perspective of a peace deal remained elusive, Bloomberg noted.

Ø SpaceX's IPO is expected to raise more than twice as much as any IPO before it, with a target valuation of at least $1.8 trillion, Bloomberg also noted, adding that the IPO success or failure could have significant implications for the market as whole. Contributing to fuel more speculation was last week’s “fire ball” event happening to Blue Origin’s flagship heavy‑lift rocket, the only U.S. system intended to compete directly with SpaceX’s Falcon Heavy and eventually Starship.

SpaceX guaranteeing 30% of the deal going to retail investors (and Musk’s fan base) will likely fuel further enthusiasm for the IPO.

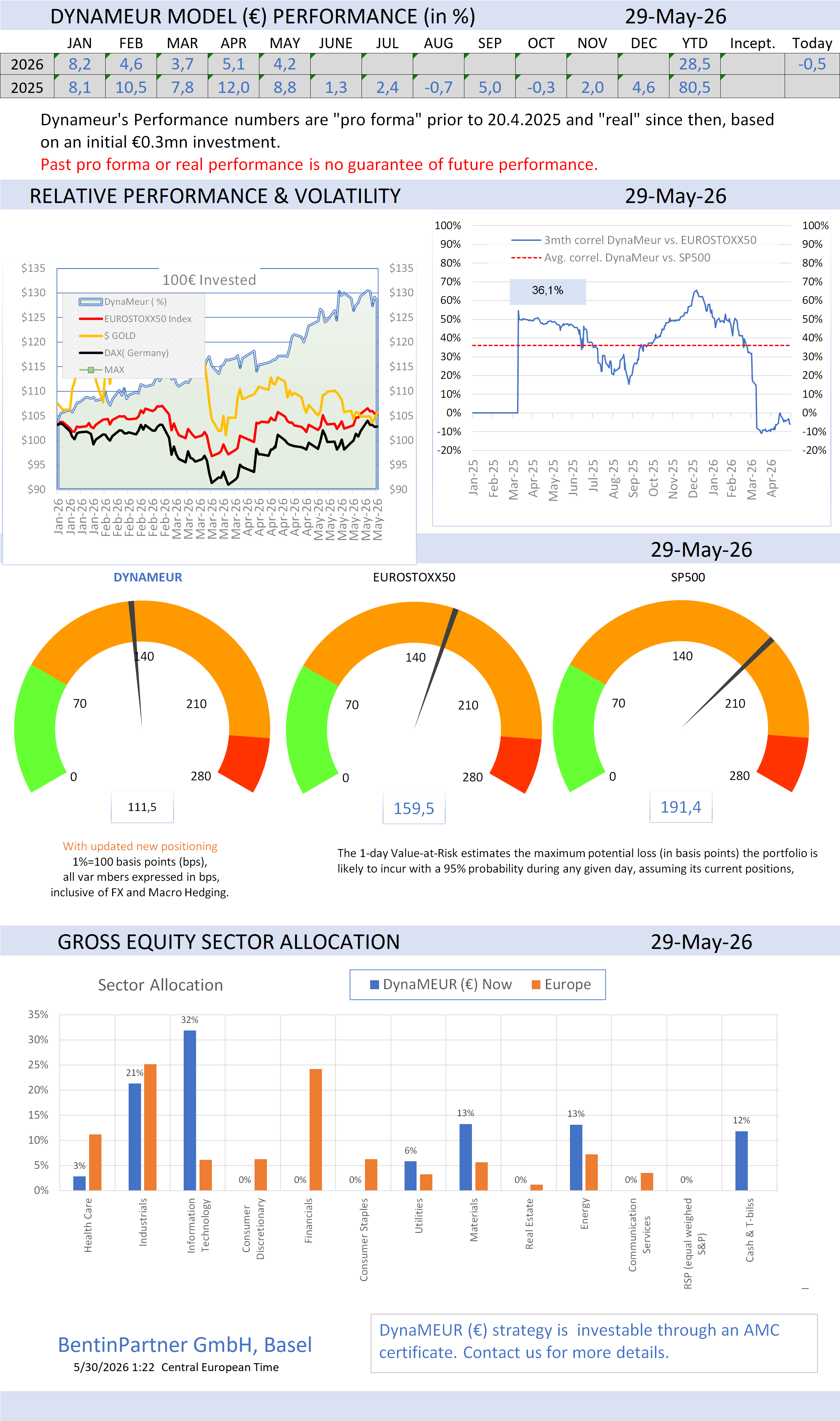

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments