The Great SpaceX/OpenAI Sucking Sound...

- Marc Bentin

- May 26

- 8 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

US stocks gained for an eight consecutive week last week, supported by expectations of a nearing resolution and optimism about the upcoming mega IPOs of SpaceX and OpenAI.

In that context, BoA CIO Hartnett jumped out of the fence over the week end saying that “AI is the biggest bubble since the railroads (when it comes to the concentration of stocks rallying in comparison with the US total market cap) but that two things are required before selling. First the SpaceX/OpenAI IPO as banks are unlikely to allow a meaningful correction before they get a chance to earn billions in fees and before policy tightens in the US once inflation reaches 4-5% “in the coming months”.

I very much share the same view now…Bonds and stocks have further diverged even as, over the past couple of days, bonds regained some composure.

To a large extent the AI bubble growing further and the bond troubles of the past few months are two facets of the same potential problem as corporations lined up for the biggest IPOs in history are among those large AI players crowding other actors of the US economy, including the government and retail borrowers.

The fact that the AI bubble keeps growing has all to do with retail greed and institutional investors scratching their head as to what lies ahead with the so called “passive bid” once trillions of dollars indexed to the S&P (and Nasdaq) will have to rebalance existing holdings to make room for the behemoths that SpaceX and OpeanAI constitute.

The concentration of tech stocks in the SP500 stand around 30% (+10% in the associated telecom sector) and what is already an historic concentration will become even more concentrated in weeks and months following these IPOs. Nasdaq already said it will introduce the newcomers within weeks of their IPOs while S&P said it considers fast-tracking the entry into the S&P500 from the typical 12 months to just 6 months as it also envisages to waive …the profitability requirements for inclusion in the index.

Historically, it has often been a better idea to wait for the dust to settle a little instead of buying at or near the IPO. However, adding to the madness of the crowd, the artificial support of Wall Street and the carefully orchestrated scarcity of papers (only 5% of the capital of SpaceX will go public), these IPOs could will likely lead to a stampede from both greedy retail investors and institutional indexers. What will people sell to make room for these stocks? Probably more defensive sectors rather than AI related tech stocks that should gain from the dynamics created by SpaceX and OpenAI, making the S&P an even more concentrated bet on large cap tech stocks…just a guess but a big red flag for those tempted to short the market or call the bubble to blow off…now.

Fundamentals in the US are fine for now as the increase in inflationary pressure remains contained and with the economy boosted by large capex spending and for now a still resilient job market. This is unfortunately not the case in Europe (at all) of which the economy is taking the hit from the energy shock, a collapsing confidence and a single mandated (inflation) Central Bank that speaks about tightening policy to fight an inflation that has nothing to do with a demand and all to do with a supply shock (an ideal reason for not raising rates, I would think).

Unfortunately, Europe is also paralyzed by stubborn and ideologically driven bureaucrats and politicians desperate to hang on to power, ready for all tricks to keep it, who are also for the most part covering up the extent of the economic hit impacting Europe…France is a case in point with composite PMI collapsing to ….43.5 recently from 47.6 (50 being the defining line between growth and recession), the largest contraction in 5 years, which most likely will coincide with a 1% decline in GDP (and 70% odds of a recession) while the budget deficit target of 5.3% by year end is expected to zoom instead over 6.5%. It cannot be emphasized enough that this was a sudden and broad‑based collapse in activity, resulting from an energy shock and demand destruction. Interestingly last week, the UK lifted sanctions against Russian oil (to be refined by third parties) as the UK PM faces a political storm of his own.

During that time, the Diplomat in Chief in Europe, originating from the smallest EU country and who neither US and Chinese counterparts seem to even want to talk to, is pushing for more sanctions against Russia, driven by a chronic Russophobia…

This is the context in which the likely imminent aggravation of the conflict in Ukraine (caused in large part by letting Ukraine cross red lines after red lines without EU pushback) will further scarify the European economy while the US emerges relatively and “artificially” unscathed.

Bonds recovered last week, supported by a decline in oil prices and encouraged by expectations that the newly appointed Fed Chair Kevin Warsh will be able to cling to some form of Federal Reserve independence and as he is viewed as the reformer candidate that argued against B. Bernanke’s radical monetary doctrine. Kevin Warsh will certainly be facing an incredibly challenging situation considering that the US debt has essentially doubled (to USD37trn) while the Fed balance sheet increased by 50% from when J. Powell took the helm of the Federal Reserve.

At the end of the day, the Fed may have to resort to similar policies when faced with an impossible equation to solve but he deserves the benefit of the doubt for saying that “to fulfill this mission, I will lead a reform-orientated Federal Reserve, learning from past successes and mistakes, both escaping static framework and models, and upholding clear standards of integrity and performance”.

The dollar closed mostly unchanged (still keeping its slow depreciation trend intact vs. CNY).

Gold and silver gained 1.7% and 5.3% respectively, supported by falling yields last week, while gold mines underperformed. The lasted “In Gold We Trust Report” was released last Wednesday (see press conference presentation ) and remains the “must read” reference for all gold investors, especially after the recent correction that has perhaps shaken investors’ confidence a little bit.

Despite facing the headwinds from a recent increase in bond yields and some liquidation from Turkey or India to defend their currency, the case for gold regaining its previous all-time highs and then some over the next months and years, remains as strong as ever, resting on five pillars;

-chronic fiscal deficits that will ultimately force debt monetization and artificially low interest rates (financial repression)

-the return of inflation linked to deglobalization, energy transition bottlenecks, defense spending and demographics

- a move towards a multipolar reserve system (de-dollarization is a slow-moving phenomenon but a fact nonetheless, with the USD representing only 50% of world reserves from 70% in 2015 while gold and CNY taking the bulk of the difference in a trend that we expect will continue.

-record central bank buying (and repatriation). Despite a recent slow down related to the war in Iran, CBs are still set to purchase 1000 tons of gold for a fourth year in a row.

-underinvestment in mining supply

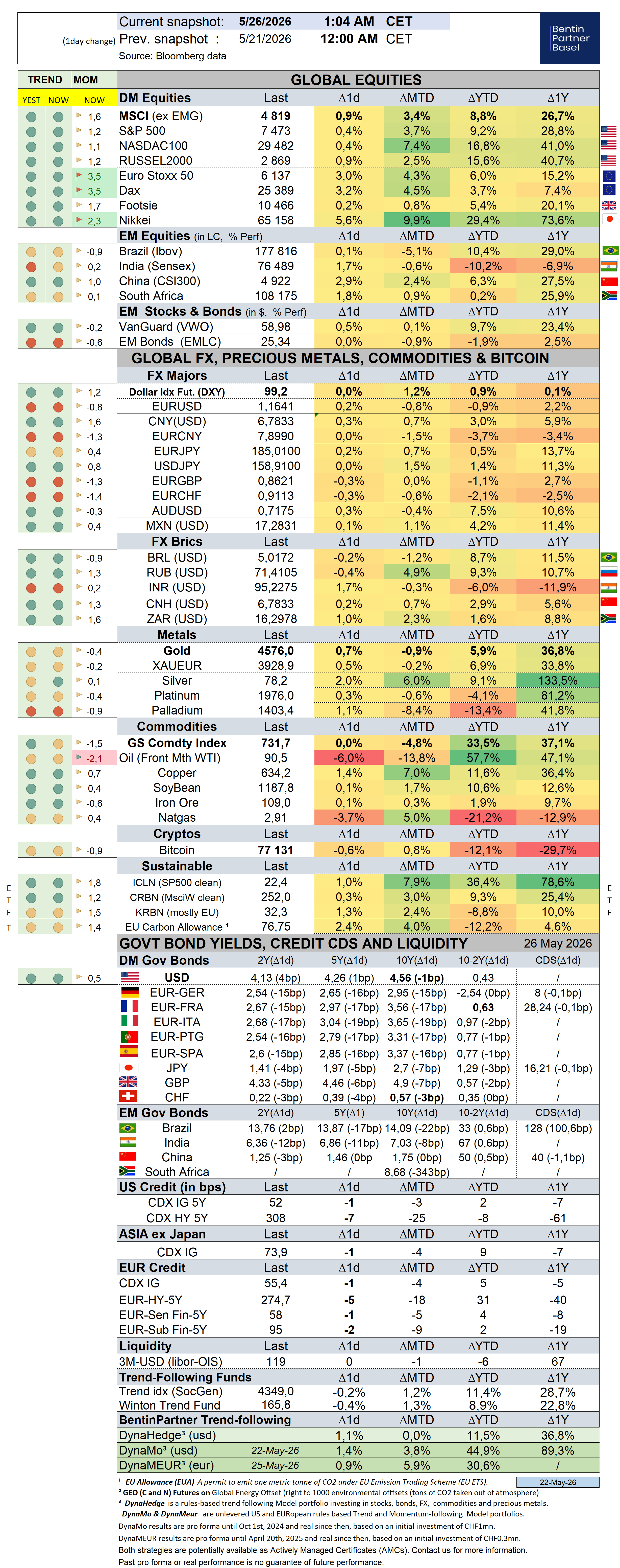

Over the past week, the S&P500 gained 0,9% (9,3% YTD) while the Nasdaq100 gained 1,2% (16,8% YTD). The US small cap index rallied 2,7% (15,8% YTD). AAPL rallied 2,9% (13,6%).

The Equally Weighed SP500 rallied 2,5% (7,8% YTD, Z-score 2,4), outperforming the S&P500 by 1,6%. The median SP500 YTD return closed the week at 2,9%.

Cboe Volatility Index sold off by -6,9% (11,0% YTD) to 16,59.

The Eurostoxx50 rallied 4,9% (7,6%, Z-score 2,6), outperforming the S&P500 by 4%.

Diversified EM equities (VWO) gained 0,9% (9,7%), matching the S&P500.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies was unchanged (2,7%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) gained 0,6% (0,9%).

10Y US Treasuries rallied -4bps (39bps) to 4,56%. 10Y Bunds dropped -20bps (9bps, Z-score -2,1) to 2,95%. 10Y Italian BTPs rallied -25bps (10bps , Z-score -2,2) to 3,65%, outperforming Bunds by -5bps.

10Y French OAT's rallied -22bps (-1bps, Z-score -2,2) to 3,56%, outperforming Bunds by -2bps.

US High Yield (HY) Average Spread over Treasuries dropped -12bps (-6bps) to 2,60%. US Investment Grade Average OAS dropped -2bps (-6bps) to 0,78%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps (4bps) to 0,58%.

Gold gained 1,7% (5,6%) while Silver rallied 5,3% (8,3%). Major Gold Mines (GDX) sold off by -2,7% (-0,9%).

Goldman Sachs Commodity Index sold off by -2,1% (36,6%). WTI Crude sold off by -16,3% (58,3%, Z-score -2,0).

Overnight in Asia…

Ø S&P future +49 points; Hong Kong +0.5%; Nikkei -0.2%; China -0.3%

Ø Asian stocks extended gains following Friday’s US stock market rally (US stocks were closed yesterday) and expectations that the US and Iran will be able to extend a cease fire which led to a 7% oil price decline (to 96 on Brent), the lowest in more than a month during a holiday thinned session.

Ø Russian Foreign Minister Sergei Lavrov called US State Secretary Marco Rubio to advise him to evacuate US citizens and diplomats from Kyiv due to planned heavy strikes on the Ukrainian capital and against relevant “decision-making centers” at the request of President Vladimir Putin. The Kremlin has urged all foreign nationals to leave Kyiv as soon as possible and advises residents to stay away from military and administrative infrastructure, citing plans to continue series of systematic retaliatory strikes, Bloomberg reported.

Ø Donald Trump said that negotiations with Iran over an interim deal to extend their ceasefire and reopen the strait were “proceeding nicely.”

Ø Still, US and Israeli jets struck Iranian vessels in the Strait of Hormuz and other targets, with several Iranian personnel killed, according to Iranian authorities. Sticking points remain unresolved, including the future of Iran’s nuclear program.

Ø Prime Minister Benjamin Netanyahu said Israel will intensify its strikes against Hezbollah while the draft of a potential deal between the US and Iran included language to end the war between Israel and the Iranian-backed Hezbollah in Lebanon, with Iran demanding the cessation of hostilities in Lebanon as part of any peace agreement.

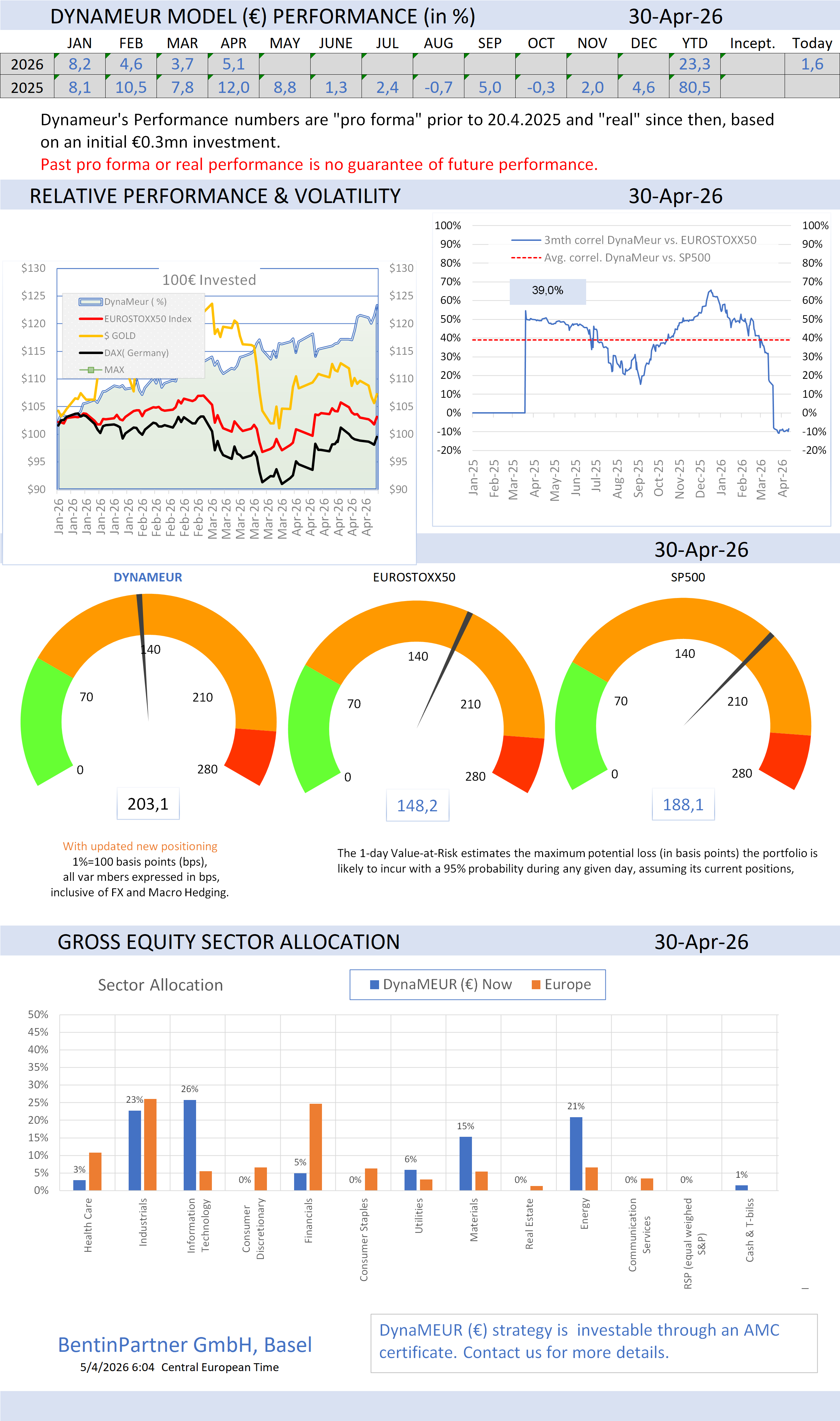

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments