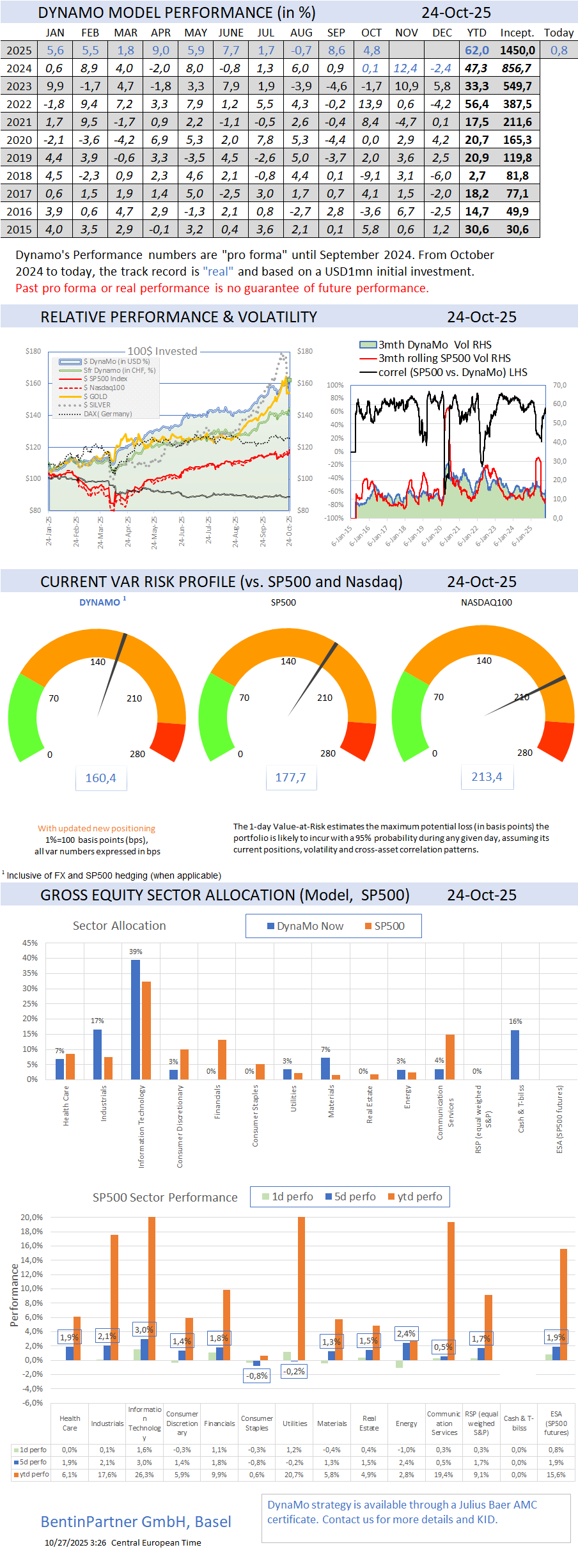

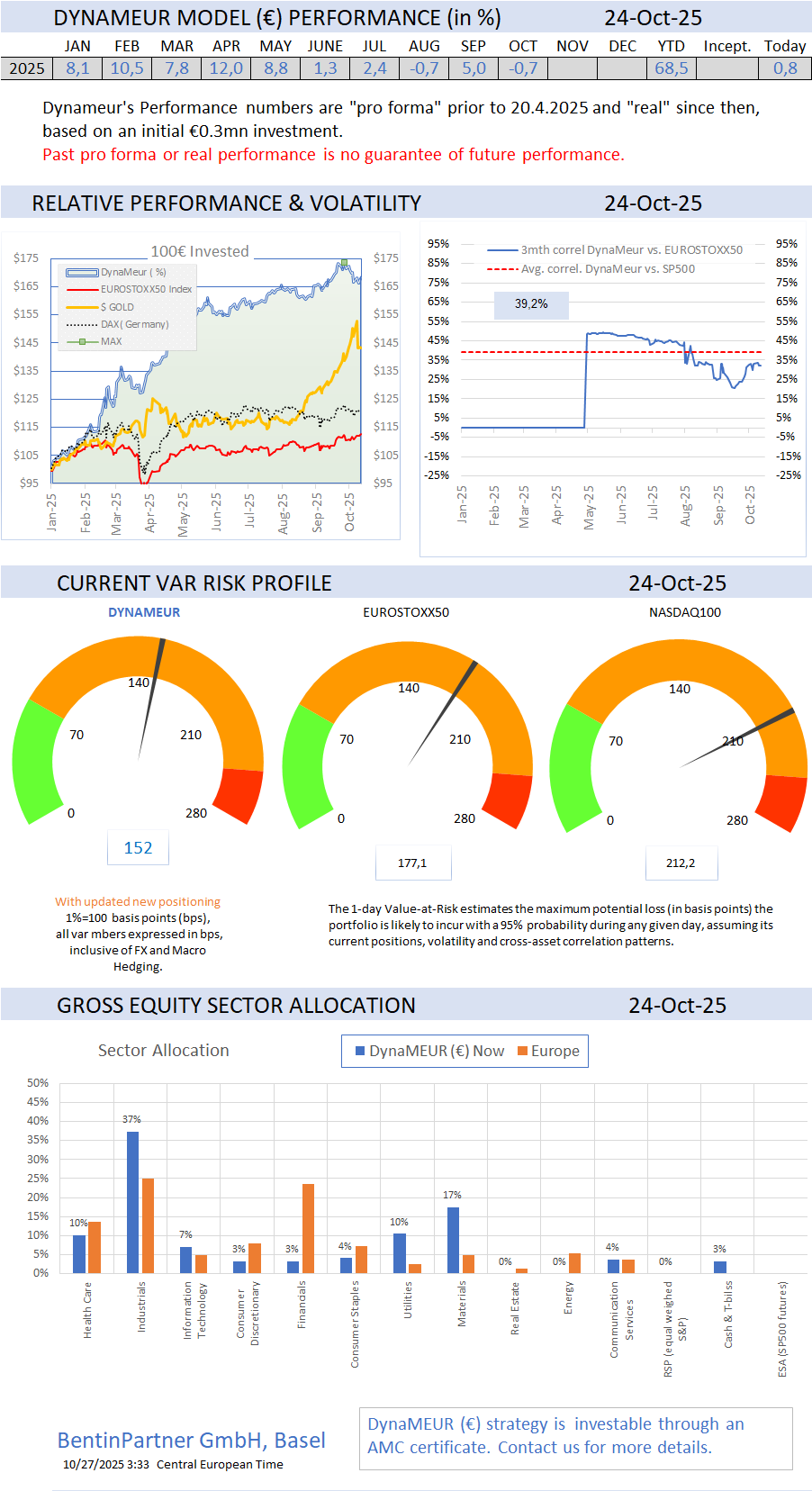

More AI Gains...

- Marc Bentin

- Oct 27, 2025

- 8 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

Major equity markets delivered additional gains last week, supported by more short squeezes, following the publication of a relatively tame US inflation report on Friday and the perspective of the Fed cutting rates this week while favorable prospects for a US-China truce ahead of the coming meeting between US President Trump and China’s President Xi also helped boost risk appetite.

On the US economic side, while the CPI came in slightly better than expected (3% yoy vs. 0.4% expected), the Atlanta Fed GDPnow forecast remained at 3.89% while the preliminary October manufacturing PMI was reported, slightly beating expectations at 52.2 (and the service PMI at a solid 55.2, the second highest reading in 10 months). Despite a tame CPI, many things are reporting higher prices including 2026 health insurance premium, beef and food in general, home and auto insurance, and even electricity with lower oil prices covering up for most of those increases, it seems (and perhaps also a few hedonistic adjustments). For what it is worth the University of Michigan consumer survey for the 1-year inflation expectation remained at solid 4.6% (3.9% for the 10-year expectation).

In currencies, the dollar index gained slightly last week while JPY dropped 1.5% on the week on prospects of a more dovish BoJ and the appointment of a fiscally loose Prime Minister.

US leveraged loan activity still felt the heat from the First Brands and Tricolor Holdings related selling but rebounded slightly last week. While US govt yields rose slightly, US HY also improved a couple of bps last week, despite investors pulling some USD970mn from US high yield Mutual Funds. There was also some indication of higher risk aversion and tighter underwriting for high risk lending. JPMorgan said early last week that credit related worries have been driving up banks’ funding costs and that a lack of transparency at private equity groups and hedge funds were to be blamed. The IMF earlier this month and more recently BoE Governor Bailey, also warned on the need for greater oversight of a sector where banks in the US and Europe have exposure estimated around USD4.5trn. Obviously, few dare to talk about the “B” word but most are thinking about it…

On a more positive note perhaps, it was reported on Thursday that Banks were preparing to launch a USD38bn debt offering as soon as today to help fund data centers from Oracle, which would be the largest such deal for AI infrastructure (with JPM among the lead managers of the deal). Obviously, as well the AI arms race is still raging…

As the Fed meets this week to decide to cut interest rate, it will face another question becoming increasingly urgent, how soon it should stop shrinking the Fed USD6.6trn balance sheet as money markets have been flashing for several weeks already that the process should have run its course.

A good way to replenish the depleted reserves could also be to revalue the Fed’s gold but although it would not require per se the purchase of additional gold, it would deliver a bad optic at a time after gold soared this year, supported by relentless Central Bank buying and mounting concerns about fiat currency debasement.

Last week’s most salient market development was a pronounced sell-off in precious metals which, in my view, was salutary. The selloff in Gold followed that of silver which was only of a technical and manipulative nature (the silver future contract was under threat with severe and exceptional backwardation going all the way to the fourth maturity). With this situation now normalized in the futures market, the structural deficit of silver remains and nearly guarantees, in our view, the existence of a nearby floor (especially with copper now soaring) with the only remaining negative being runaway equity markets gains (which are an integral part of the debasement trade) and the proximity of a Fed meeting (which has usually presented good entry levels for the metals) that is generally associated with lower gold and silver prices. I would be very surprised if the Fed was to act or even speak “hawkish” this time…

Due to supply concerns (and structural multi-year deficits), it was re-classified as a “critical mineral” in August 2025 by the US administration which has started stockpiling it as a result, recognizing its importance energy, defense and national security on a nearly equal foot as rare earth.

The EU Commission criticism got louder last week with 19 EU heads of state writing a letter to Ursula von der Leyen demanding the abolition of “superfluous and unbalanced regulations” and nothing less than a “regulatory reset” in Brussels. The letter came days after German Chancellor Mertz called at the SME day in Cologne for no less than “throw a stick into the spokes of the Brussels machine so as it finally stops”.

The Governor of the Belgian National Bank, Pierre Wunsch, warned against this risk back in 2024 at a conference where he required a change in EU governance, summarizing the situation by saying that so far, the “US innovates, China replicates and Europe regulates”. Some of the key take aways from his presentation were that climate change constitutes a supply shock, not a solution to Europe’s growth problems, that Europe, all things considered, is now facing energy costs that are 5 to 10 times more expensive than in the US which means that companies will flee to the US (that was before the tariffs discussion introduced by D. Trump which only made matters worse…) and that, talking about his own experience at the National Bank, the research department was getting hot under the collar because it needs to invest (lose) a lot of time in risks that have never materialized in 30 years….This led him to warn against the risks of “Eurosceloris 2.0” before most others (see from ‘8min of this presentation).

The EU Commission suffered another blow last Friday with Belgian Prime Minister B. De Wever standing against the proposed seizure of USD180bn Russian assets held at Euroclear, supported by a solid legal argumentation, which mentioned, en passant, the fact that Japan and other countries controlling about half the frozen sovereign Russian assets, have refused to follow the path of confiscation.

Over the past week, the S&P500 gained 1,9% (15,6% YTD) while the Nasdaq100 rallied 2,2% (20,7% YTD, Z-score 2,0). The US small cap index rallied 2,5% (12,9% YTD). AAPL rallied 4,2% (5,0%).

The Equally Weighed SP500 gained 1,7% (9,1% YTD), underperforming the S&P500 by-0,2%. The median SP500 YTD return closed the week at 7,4%.

Cboe Volatility Index sold off by -21,2% (-5,6% YTD) to 16,37.

The Eurostoxx50 gained 1,2% (18,7%), underperforming the S&P500 by-0,8%.

Diversified EM equities (VWO) gained 1,5% (25,3%), outperforming the S&P500 by -0,5%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 0,6% (-5,1%) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,2% (6,5%).

10Y US Treasuries dropped 4bps (-55bps) to 4,02%. 10Y Bunds climbed 5bps (26bps) to 2,63%. 10Y Italian BTPs climbed 4bps (-11bps) to 3,42%, outperforming Bunds by -1bps.

10Y French OAT's underperformed rising 7bps (24bps) to 3,43%, underperforming Bunds by 2bps.

US High Yield (HY) Average Spread over Treasuries dropped -12bps (-6bps) to 2,81%. US Investment Grade Average OAS dropped -3bps (-6bps) to 0,81%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -1bps (-4bps) to 0,59%.

Gold sold off by -6,0% (56,0%) while Silver sold off by -7,5% (67,8%). Major Gold Mines (GDX) sold off by -7,5% (114,7%).

Goldman Sachs Commodity Index rallied 3,3% (6,9%). WTI Crude rallied 7,3% (-14,0%).

Overnight in Asia…

S&P future +55 points; Hong Kong +0.8%; Nikkei+2.2%; China +0.9%

Asian stocks and US futures are trading higher on US and China closing in on a trade deal. Top US and Chinese negotiators said they came to terms on a range of contentious points, setting the table for leaders Donald Trump and Xi Jinping to finalize a deal and ease trade tensions. Preliminary consensus on topics including export controls, fentanyl and shipping levies was reached while US Treasury Secretary Scott Bessent said Trump’s threat of 100% tariffs on Chinese goods “is effectively off the table”. Striking a conciliatory tone, the People’s Daily said this morning the progress showed Beijing and Washington were capable of handling their differences.

Copper surged (reaching record highs), as did oil, with the potential US-China deal bolstering the demand outlook.

Despite plenty of earlier predictions to the contrary, Argentina President J. Milei is on track to win the mid term elections with 90% of the votes counted. Markets will likely rally Monday in response to the news of Milei’s resurgence. His relentless pursuit of deregulatory policies and ambitious budget cuts had won cheers from investors before the election last month, Bloomberg reported. Milei’s win will also vindicate the extraordinary support US Treasury Secretary Scott Bessent offered Argentina. Just before the election, the US signed a $20 billion currency swap line agreement with Argentina to shore up the beleaguered peso, which is down more than 30% so far this year.

France Socialist party introduced a scaled down version of its wealth tax proposal in exchange for supporting the 2026 budget (to be voted on late next week).

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments