The 1 Trillion $ Question...

- Marc Bentin

- 6 days ago

- 6 min read

BentinPartner Weekly

Dear Reader,

Please find below our latest Weekly Trend Report.

Have a nice start of the week.

Marc Bentin,

Bentinpartner GmbH

During his inaugurating first press conference as Fed Chair K. Warsh pinpointed persistent US inflationary pressures and reminded the Fed’s responsibility to deliver on its price stability objective of 2%.

This was good news but also took some market participants by surprise, leading to a rerating of expectations for a Fed rate hike or two (already pricing with 93% probability a 25bps rate hike by September) before the end of the year.

By not giving his own “dot plot”, K. Warsh also left his options open, leaving everybody guess where he stands on those expectations, also signaling that he plans to deliver on his reform agenda for the Fed appointing a handful of new “task forces”.

This was not enough to dent buoyant risk appetite and optimism on US equity markets added roughly 1% on the week with the Nasdaq gaining nearly three times as much as retail investors poured money into US stocks at a record pace on the day of SpaceX’s blockbuster IPO.

Trading activity reported by Citadel from the retail group spiked to unprecedented levels across both equities and options, Bloomberg reported. To the $75bn IPO of SpaceX, $35bn of debt financing for Anthropic awas also added, pointing to continued investors’ appetite to fund the AI craze. That is good news as well both consumption and investments remain highly dependent on the Ai bubble not popping.

At the same time, Goldman wrote a note over the week end asking the “one trillion-dollar question” of whether China’s AI Models are better value than their US counterparts. If they are, it could challenge the US AI bubble circle financing (and US GDP Growth which is now 50% coming from AI). This is likely the reason for the most recent US crackdown on Anthropic, trying to ban the foreign usage of Claude Fable 5.

As a word of caution as well, Goldman noted that the divergence in stock price performance between “cheque writers” (the hyperscalers such as Nvda) and “cheques receivers” (the SOXX to a large extent) was another widening crocodile jaw.

Japan’s stocks stormed nearly 8% higher (and the KOSPI +11%) on a further JPY devaluation and as speculation remained intently focused on the SOXX index (chips).

European markets followed US equity markets higher as well, adding a bit more than 1%.

US bonds were hit in the immediate aftermath of the Fed meeting and 10Y yields ended the week higher by 4 bps.

At the same time, the default rate among private-credit borrowers reached the highest in roughly three-years, adding signs of stress in the USD1.8trn market, Bloomberg noted.

In FX, the dollar reacted fairly positively to K. Warsh’s words, gaining 1% on the week.

At the same time, in a mirror like fashion following higher yields and a recovering dollar, precious metals dropped with gold shedding nearly -4% and silver twice as much while commodities also dropped, led by lower oil prices. Soft commodities like Corn and wheat rallied however, as the lack of fertilizer during the sowing season still guarantees lower crop yields and higher (food) prices at least for a while.

While most of the recent enthusiasm to justify lower oil prices and a further decline in the risk premium rested on progress towards in the Middle East peace (with most US previous red lines essentially crossed or scratched), talks between the US and Iran were called off Friday after intense fighting between Israel and Hezbollah in southern Lebanon, raising questions about an initial agreement to end the war in Iran. Israel and the militant group later agreed to renew their ceasefire, three officials said, according to the Associated press.

President D. Trump also said last Wednesday at the G7 conference that the U.S. will ‘go right back to dropping bombs’ if he doesn’t like the Iran deal. Trump said that the proposed agreement to bring the Middle East conflict to an end… is ‘not final.’ ‘It’s a memorandum of understanding, and if I don’t like it, we’ll go back to shooting at them, dropping bombs on their heads. I don’t like it if they don’t behave. We’ll go right back to dropping bombs right smack in the middle of their head,’ the president said…”

In the meantime, on the other front (of the Ukraine war), Russia and Ukraine exchanged hundreds of drones with Russia also sending dozens of missiles at the Ukrainian capital of Kyiv. Not an inch of conversation effort towards peace was noticeable with some European governments seeking no other ways of communication than poking the bear ever closer.

President E. Macron is now late by two months to determine the date of the next Presidential election (with rumors now abounding that he is seeking a parliamentary dissolution …yet again, less than one year before the Presidential elections.

Those closely following French politics and the efforts to curtail the freedom of (dissenting) expression going into the still putative Presidential French election, also followed with a keen interest, the French Ministry of Truth efforts to actively pursue the silencing of Cnews.

European politics remained in a race to the bottom with UK Prime Minister K. Starmer expected to announce his resignation today (out of courtesy, President D. Trump announced it in advance over the week end). In the meantime, Spanish Prime Minister Sanchez’ wife was also taken her passport away on allegation of bribery, the FT reported.

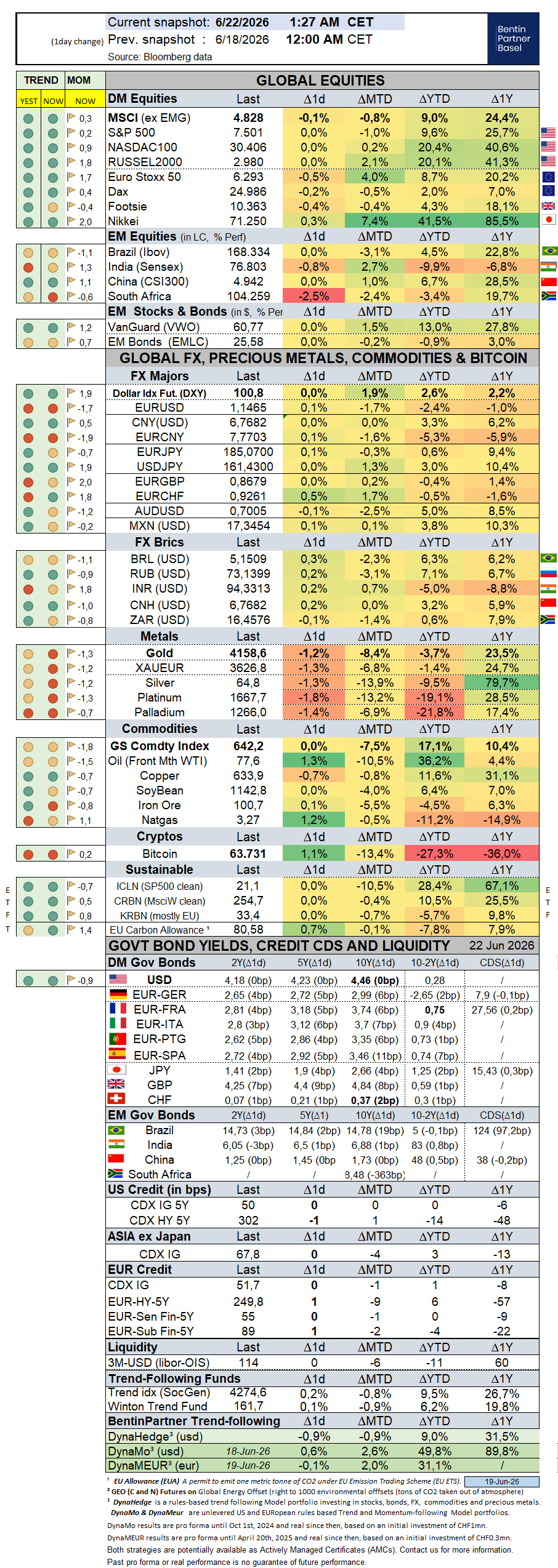

Over the past week, the S&P500 gained 1,2% (9,5% YTD) while the Nasdaq100 rallied 3,3% (20,6% YTD). The US small cap index gained 1,8% (20,1% YTD). AAPL gained 0,8% (9,6%).

The Equally Weighed SP500 gained 0,1% (9,6% YTD), underperforming the S&P500 by-1,1%. The median SP500 YTD return closed the week at 4,9%.

CBOE Volatility Index sold off by -5,1% (12,2% YTD) to 16,78.

The Eurostoxx50 gained 1,8% (10,6%), outperforming the S&P500 by 0,6%.

Diversified EM equities (VWO) rallied 2,8% (13,0%), outperforming the S&P500 by 1,6%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies gained 1,3% (4,7%, Z-score 2,4) while the MSCI EM currency index (measuring the performance of EM currencies vs. the USD) dropped -0,4% (0,8%).

10Y US Treasuries rallied -3bps (29bps) to 4,45%. 10Y Bunds dropped -1bps (13bps) to 2,99%. 10Y Italian BTPs dropped -3bps (15bps) to 3,70%, outperforming Bunds by -2bps.

10Y French OAT's was unchanged (18bps) to 3,74%, underperforming Bunds by 1bps.

US High Yield (HY) Average Spread over Treasuries dropped -1bps (-1bps) to 2,65%. US Investment Grade Average OAS climbed 1bps (-4bps) to 0,80%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 1bps (0bps) to 0,55%.

Gold sold off by -3,6% (-3,8%) while Silver sold off by -7,4% (-9,6%). Major Gold Mines (GDX) rallied 6,2% (-3,8%).

Goldman Sachs Commodity Index sold off by -4,2% (23,6%). WTI Crude sold off by -7,9% (36,2%).

Overnight in Asia…

S&P future -40 points; Hong Kong -1.3%; Nikkei+2%; China +0.0%

Asian shares and US stocks are lower to start the week on doubts about the US-Iran Peace Process (Japanese stocks rose however as JPY keeps devaluing).

Italian Prime Minister Giorgia Meloni has escalated her response to Donald Trump's provocations, saying he lies and panders to enemies while turning on his friends. She also poked him by telling him to look at his own polling as the November midterms approach, no doubt aware that his popularity has hit new lows.

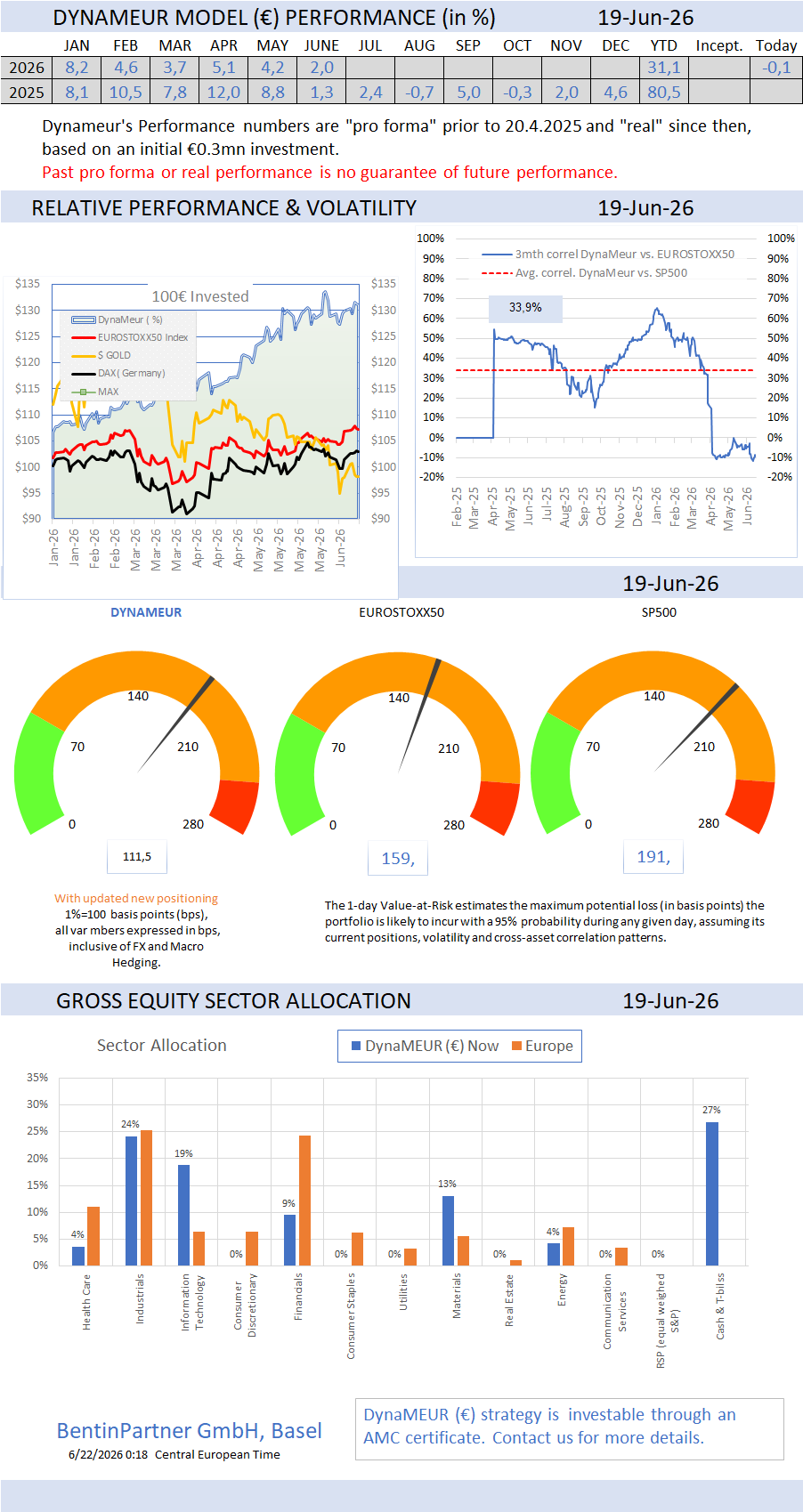

To learn more about our AMC offering and how to invest in the trend-following, visit our Advisory web page.

If you like our Weekly, you will love our Daily!

Consider a subscription today. Discounts may apply!

To learn more about us and how we can assist you, check our website

Important Disclaimer

© Copyright by BentinPartner LLC. This communication is provided for information purposes only and for the recipient's sole use. Please do not forward it without prior authorization. It is not intended as a recommendation, an offer, or solicitation for the purchase or sale of any security or underlying asset referenced herein or investment advice. Investors should seek financial advice regarding the suitability of any investment strategy based on their objectives, financial situation, investment horizon, and particular needs. This report does not include information tailored to any particular investor. It has been prepared without any regard to the specific investment objectives, financial situation, or particular needs of any person who receives this report. Accordingly, the opinions discussed in this report may not be suitable for all investors. You should not consider any of the content in this report as legal, tax, or financial advice. The data and analysis contained herein are provided "as is" and without warranty of any kind. BentinPartner LLC, its employees, or any third party shall not have any liability for any loss sustained by anyone who has relied on the information contained in any publication published by BentinPartner LLC. The content and views expressed in this report represent the opinions of Marc Bentin and should not be construed as a guarantee of performance with respect to any referenced sector. We remind you that past performance is not necessarily indicative of future results. Although BentinPartner LLC believes the information and content included in this report have been obtained from sources considered reliable, no representation or warranty, express or implied, is provided in relation to the accuracy, completeness, or reliability of such information. This Report is also not intended to be a complete statement or summary of the industries, markets, or developments referred to in the Report.

Comments